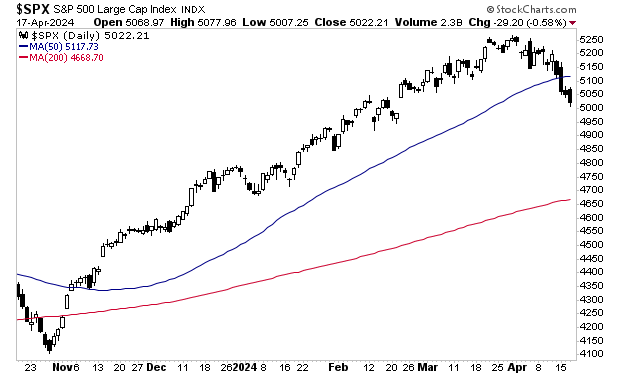

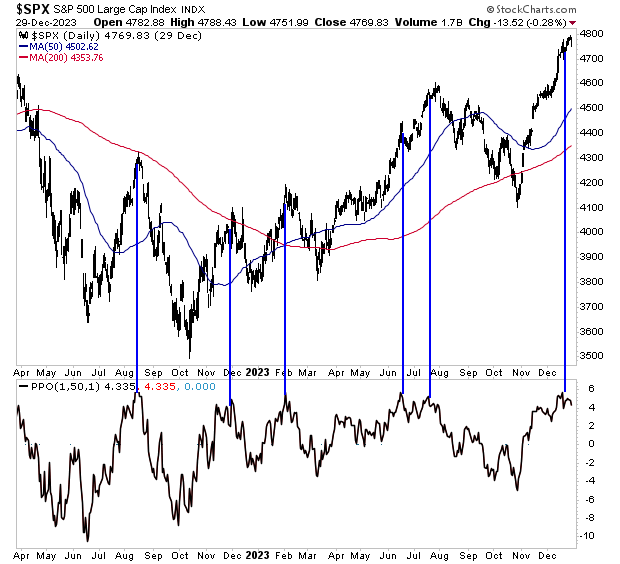

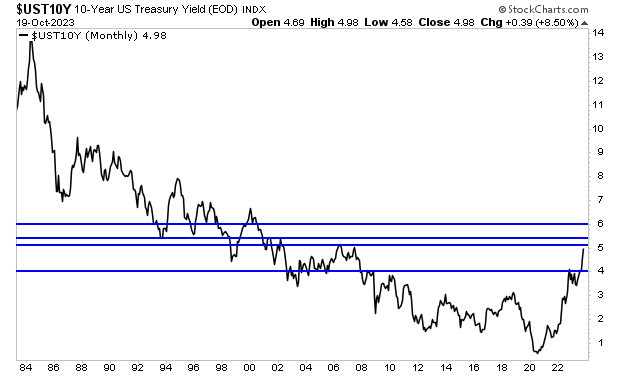

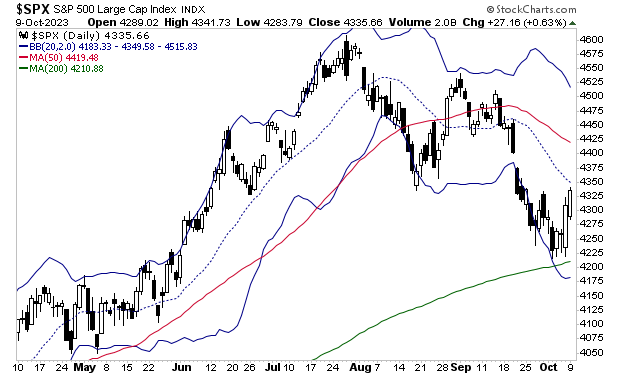

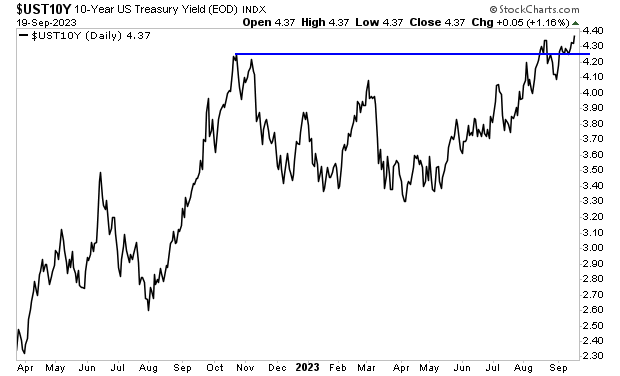

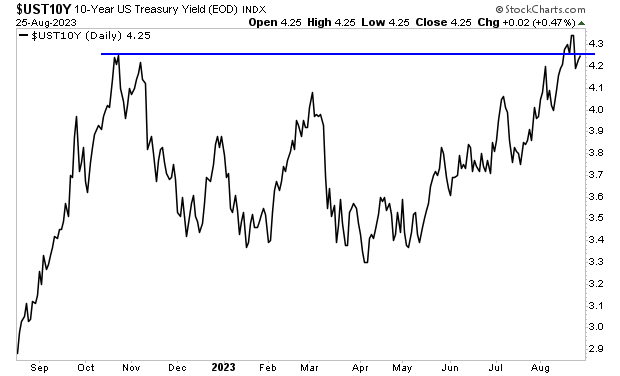

The stock market has finally woken up to what I’ve been warning about for weeks… namely that inflation is rebounding.

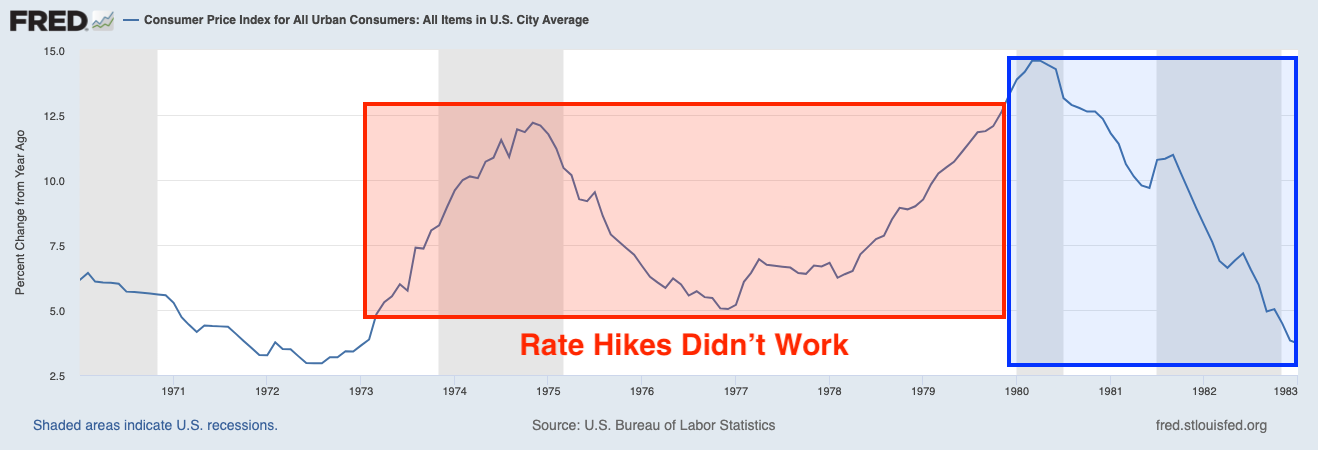

By quick way of review, the Fed stopped raising interest rates in July 2023. It then started talking about cutting interest rates in November. And it did this despite the clear evidence that Energy prices were the only part of the inflation data that had turned negative. Put another way, every other segment of the inflation data was still rising… albeit at a slower pace.

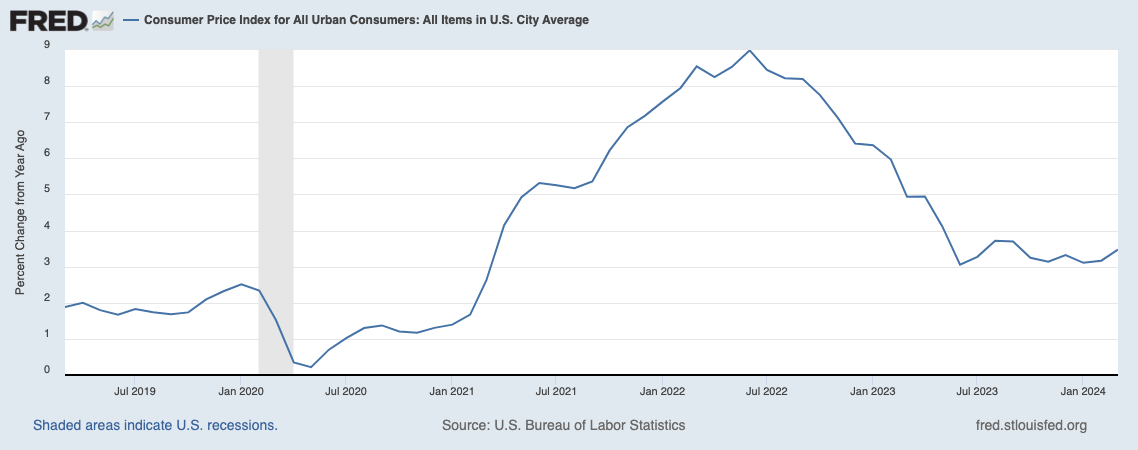

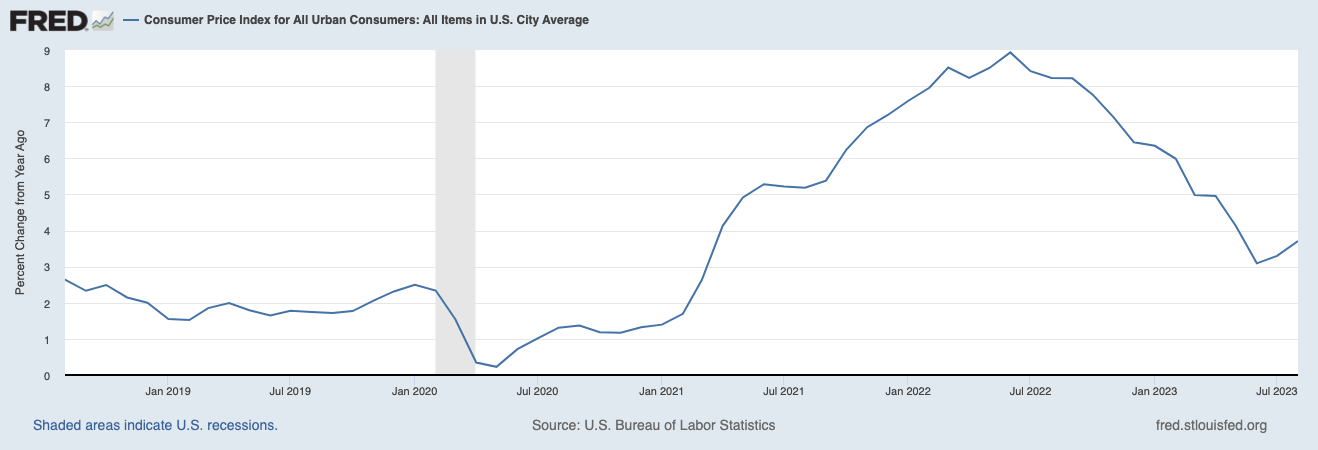

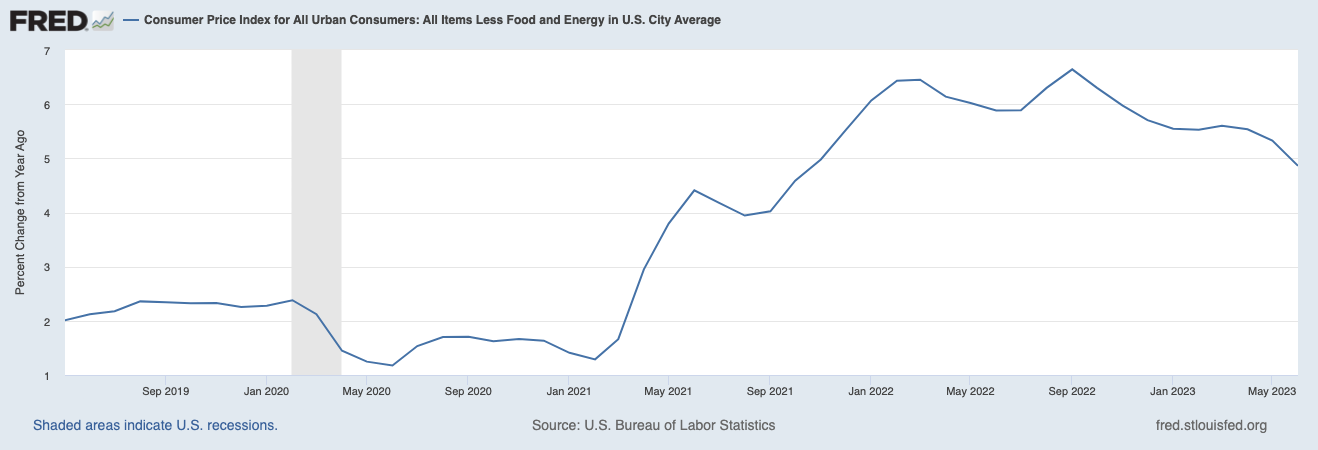

Fast forward to today, and the official inflation measure, the Consumer Price Index or CPI for short has bottomed and is beginning to rebound.

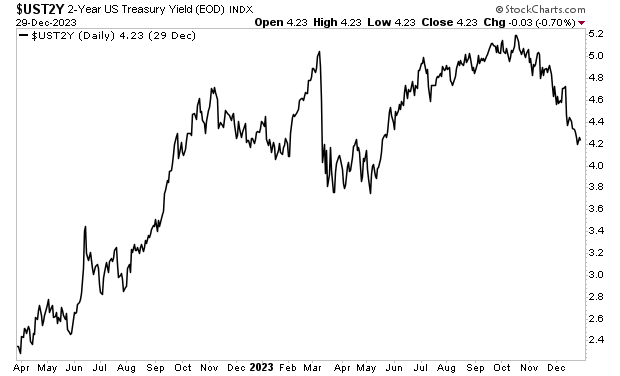

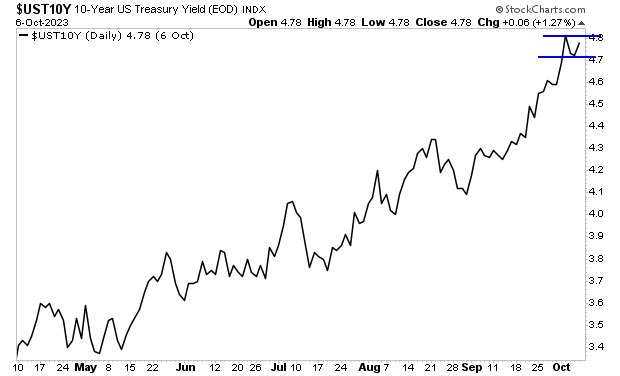

With inflation doing this, there is NO WAY the Fed can cut rates three times this year. The bond market has realized this and is now discounting maybe one rate cut of 0.25% this year.

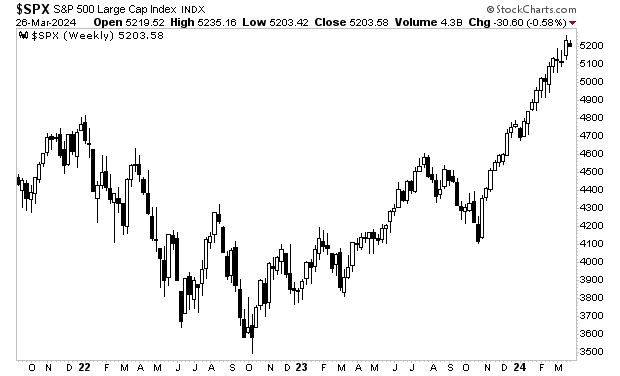

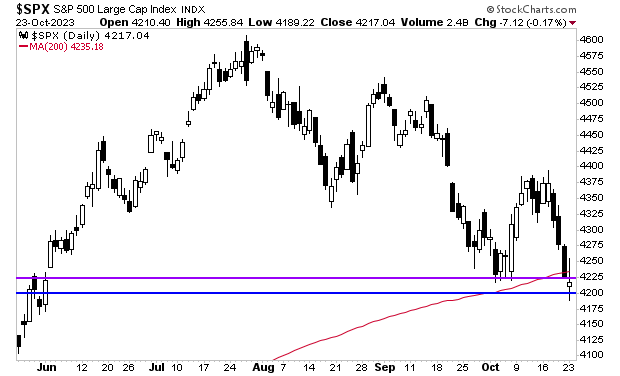

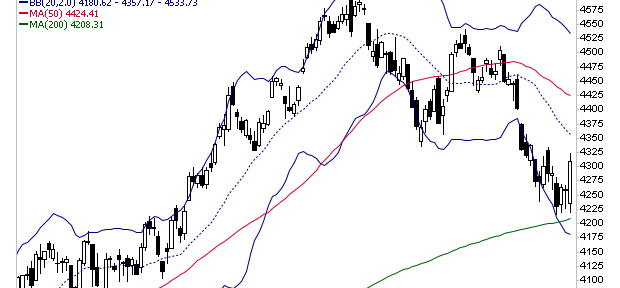

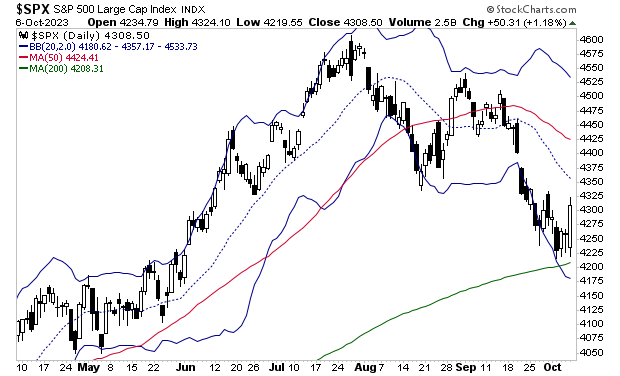

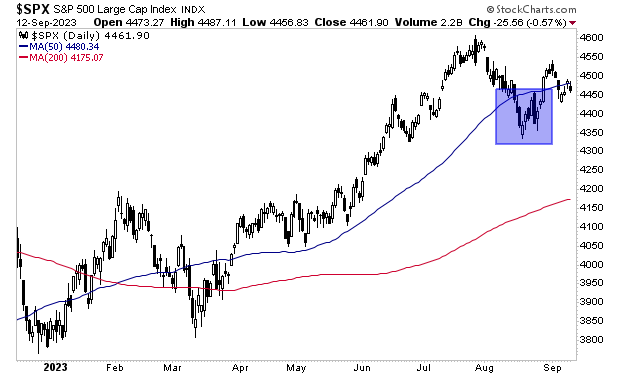

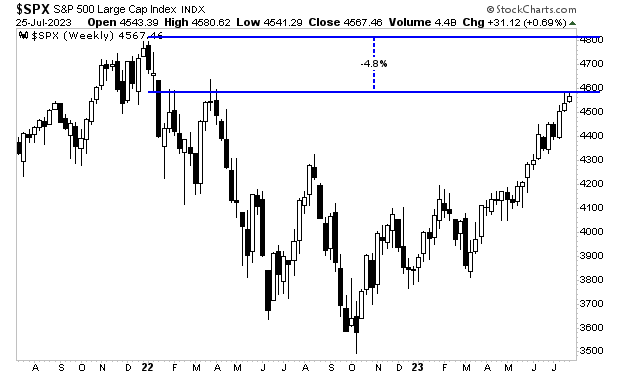

Stocks didn’t like that. The S&P 500 has now dropped 4% and is below its 50-day moving average (DMA) for the first time since November 2023.

Bottomline: this move was entirely predictable, and those investors who were prepared for it are seeing EXTRAORDINARY returns in their portfolios.

On that note, we recently published a Special Investment Report detailing three investments that will profit from this rampant government spending. Normally this report would cost $499, but we are giving copies FREE to anyone who joins our daily market commentary.

I warned time and again that the Fed was making a massive policy mistake that would unleash another round of inflation.

By quick way of review, the Fed stopped raising interest rates in July 2023. It then started talking about cutting interest rates in November. This was a MASSIVE mistake as inflation has NOT been defeated.

Indeed, ever since the Fed started talking about cutting rates, the official inflation measure, the Consumer Price Index (CPI) has bottomed and is now turning back up.

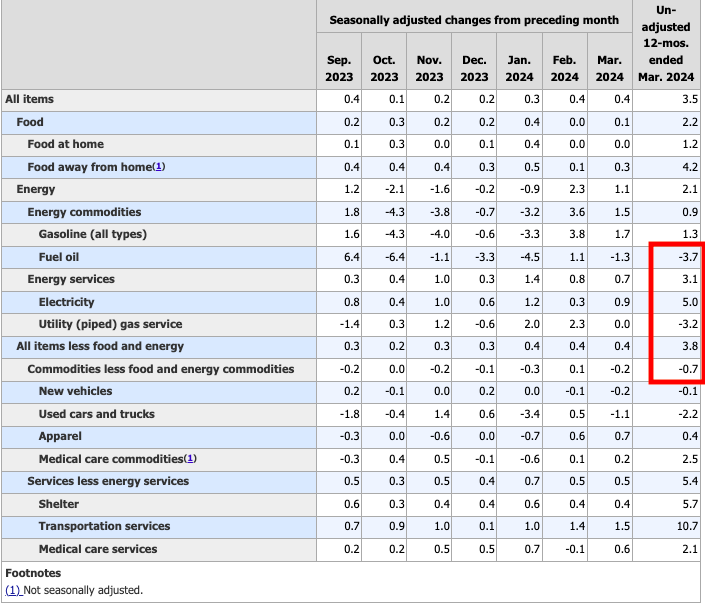

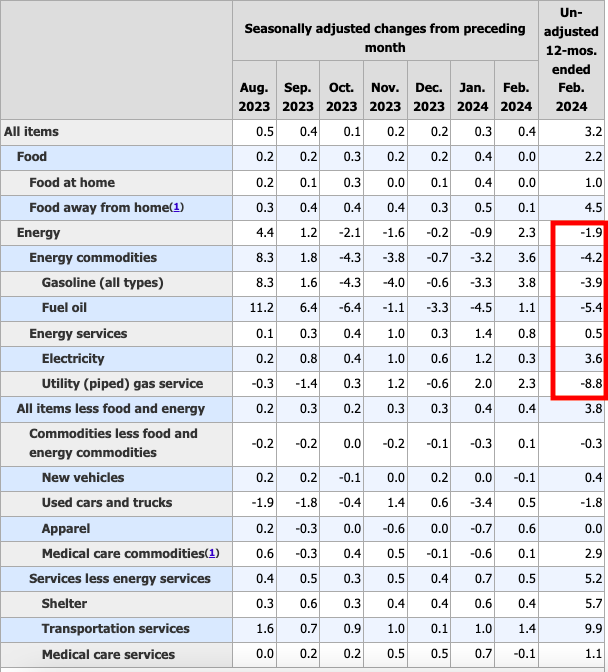

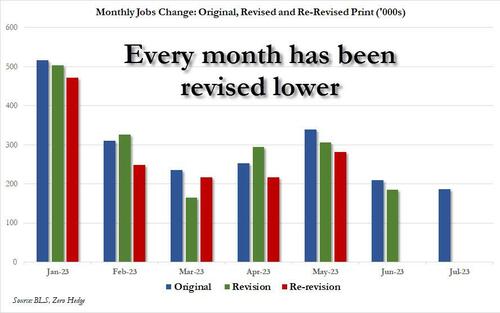

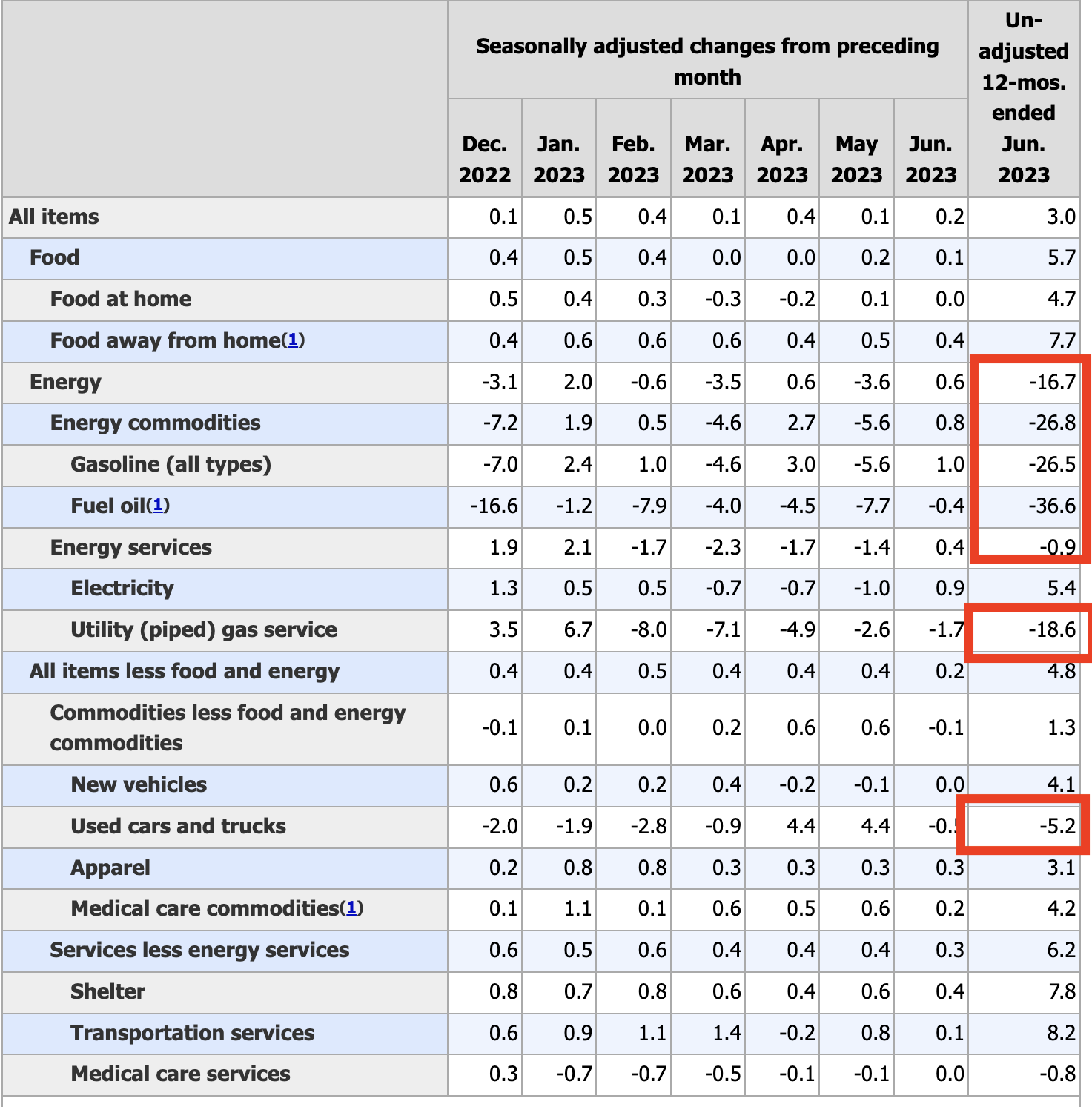

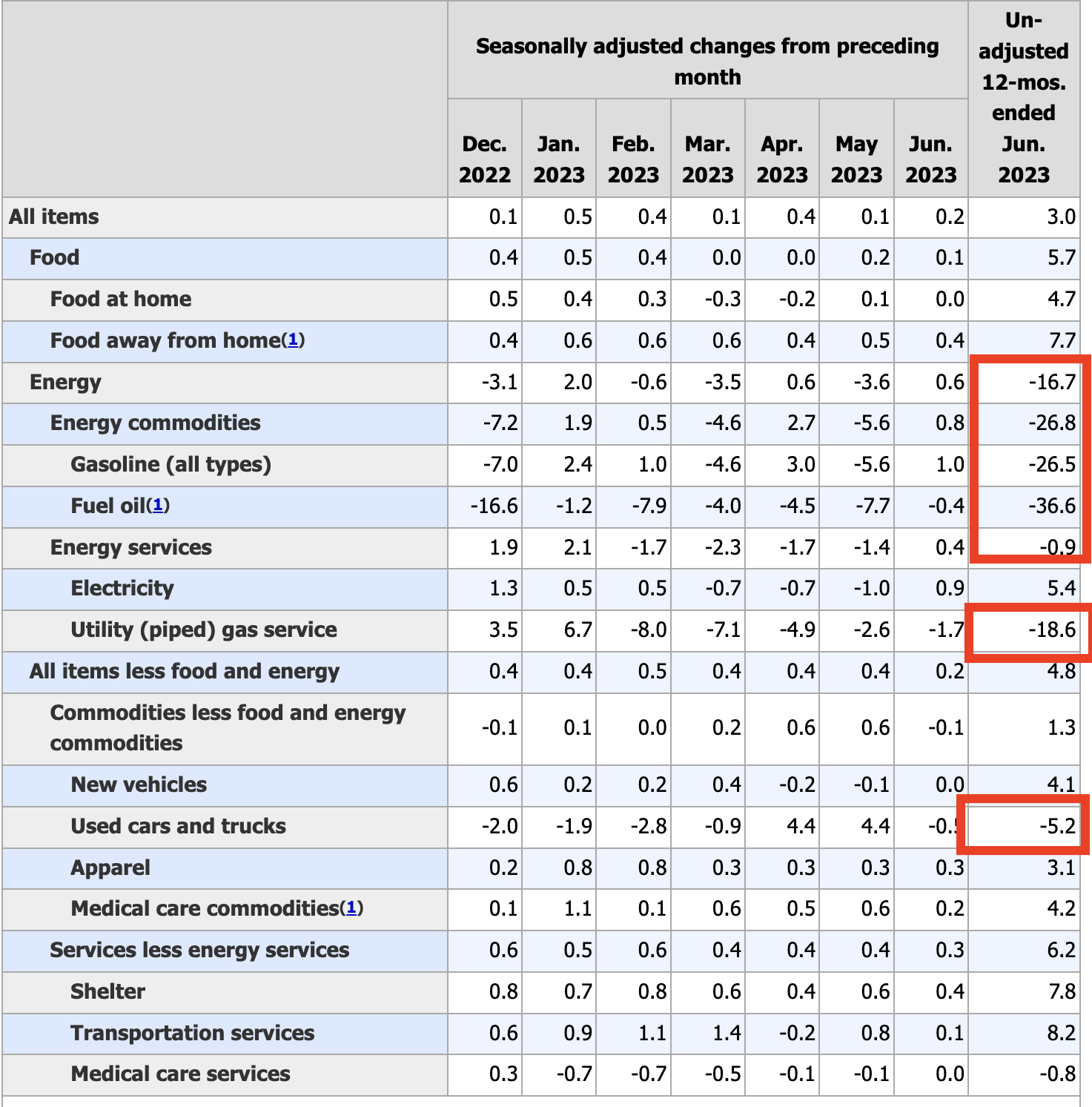

This trend continues. Yesterday, the Bureau of Labor Statistics (BLS) revealed that CPI rose 0.4% Month-over-Month (MoM) and 3.5% Year-over-Year (YoY) in March 2024.

This represents the FOURTH straight month of CPI coming in hotter than expected. The fact it surprised Wall Street and most investment strategists confirms that NONE of these people are paying attention to the data.

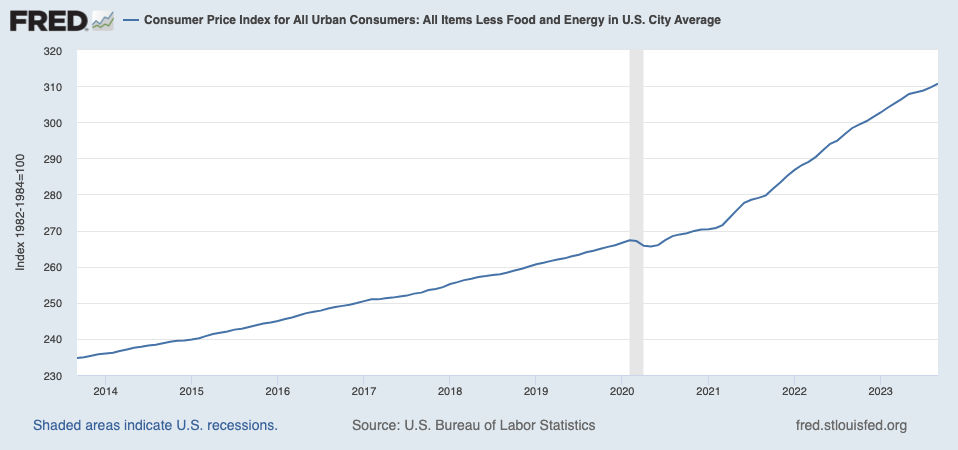

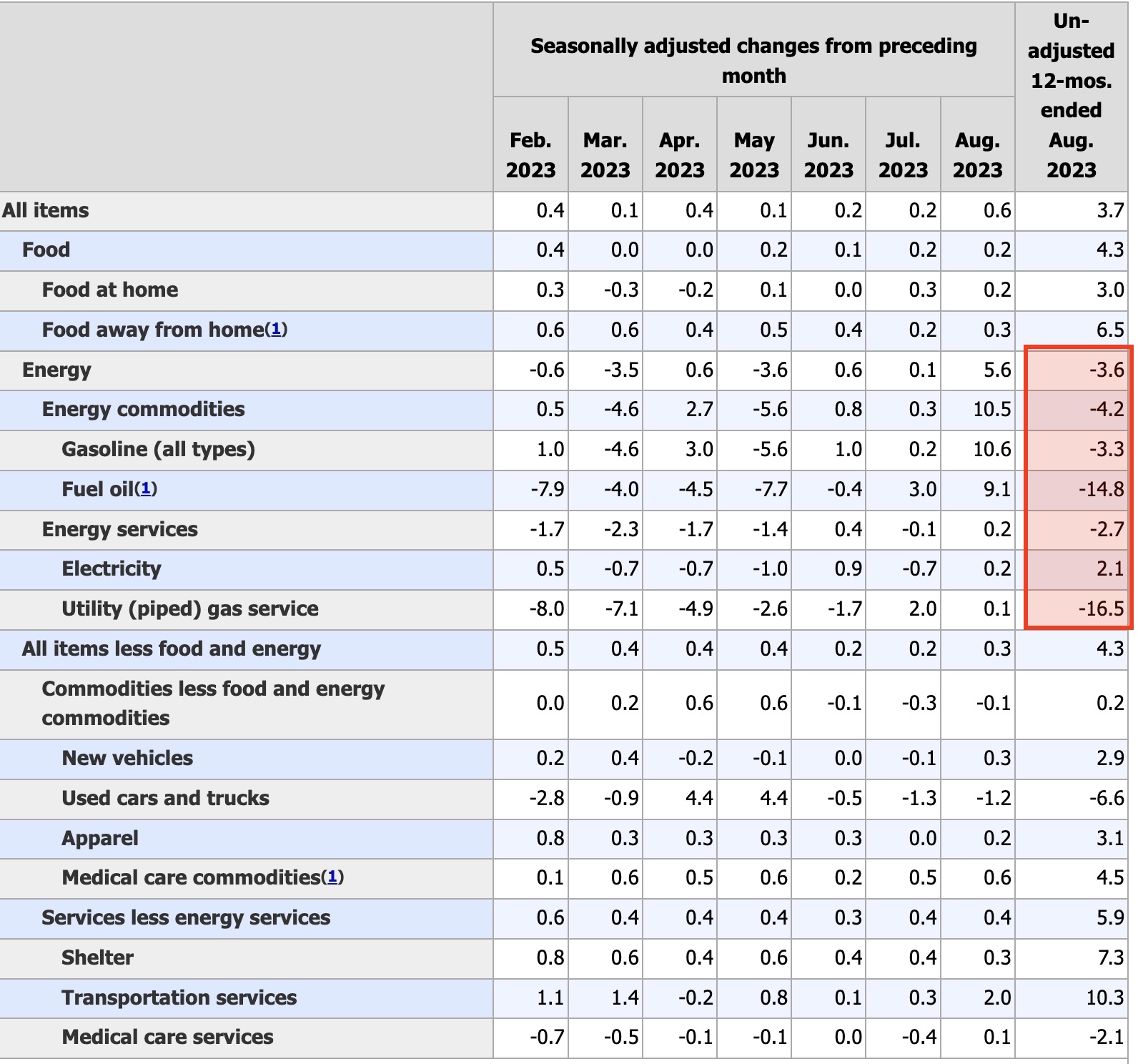

The only part of the inflation data that is down is energy prices (and used cars which receives almost no weight). Every other segment of the CPI continues to rise.

See for yourself:

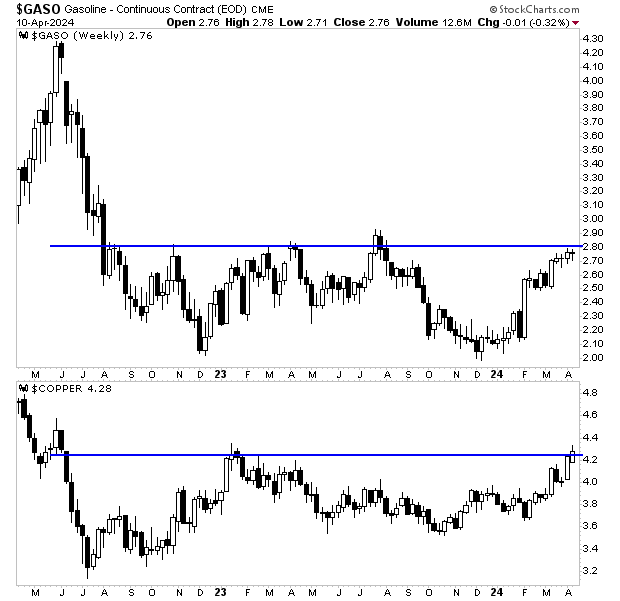

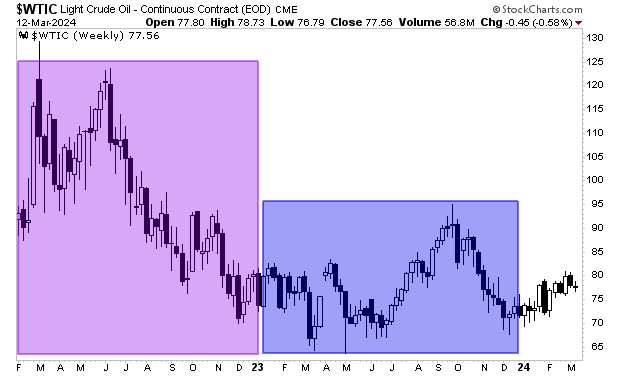

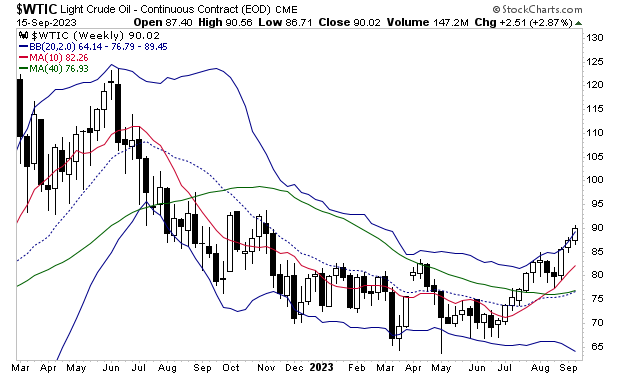

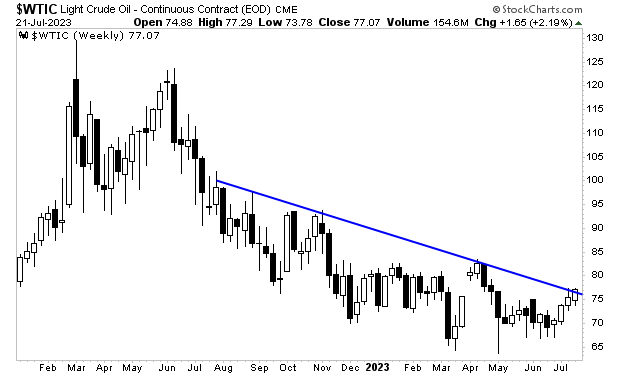

However, even Energy prices will begin turning up again… as are commodities in general. Both gasoline prices and copper prices are on the rise and about to break out of multi-year consolidation periods.

This is going to catch most investors offsides… but the good news is that with the right investments, you could see EXTRAORDINARY returns from what’s coming.

On that note, we recently published a Special Investment Report detailing three investments that will profit from this rampant government spending. Normally this report would cost $499, but we are giving copies FREE to anyone who joins our daily market commentary.

Over the last week, we’ve warned investors that the Fed’s actions are unleashing another round of inflation in the U.S. financial system.

By quick way of review.

The only part of the inflation data that is declining year over year is Energy prices. Every other segment of the Consumer Price Index (CPI) continues to rise.

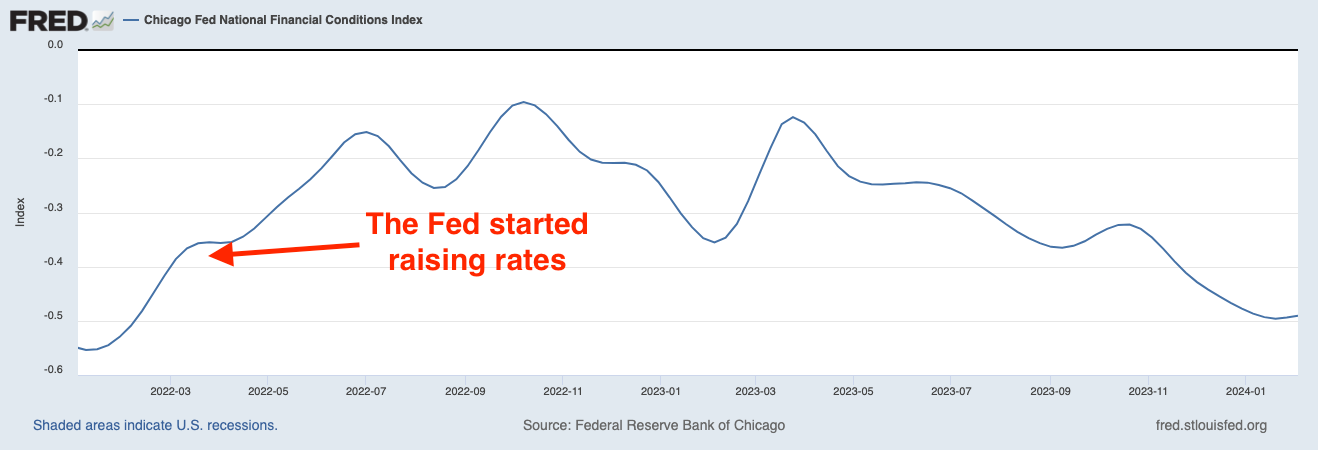

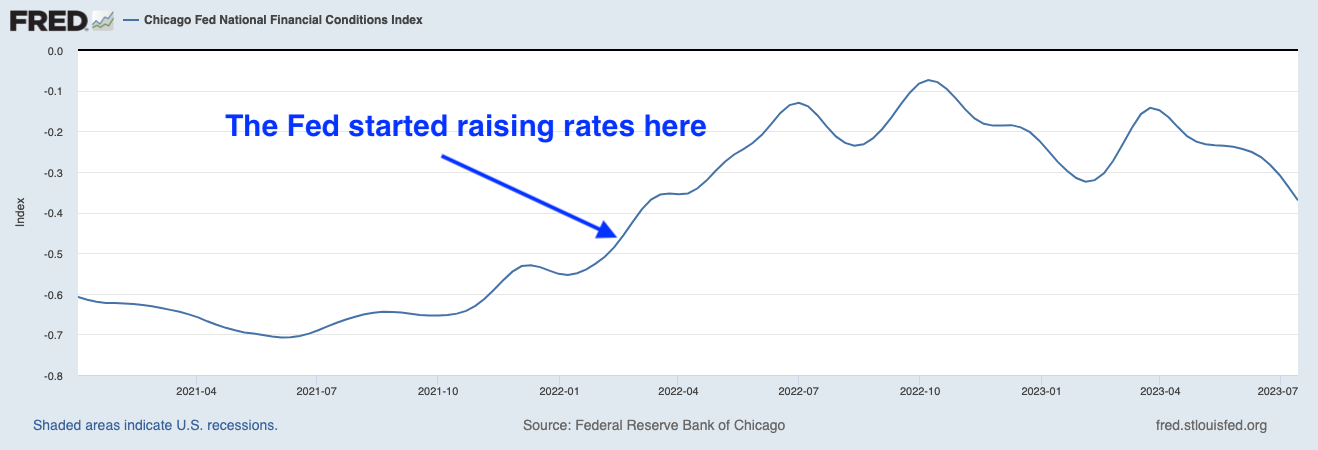

Financial conditions are as loose today as they were when the Fed first started raising interest rates in March 2022. And yet, the Fed is preparing to cut rates instead of raising them.

The Fed is still providing hundreds of billions of dollars in liquidity to the financial system via credit facilities.

The Fed’s own research indicates that food inflation is the best predictor of future inflation. And agricultural commodities are skyrocketing to new highs.

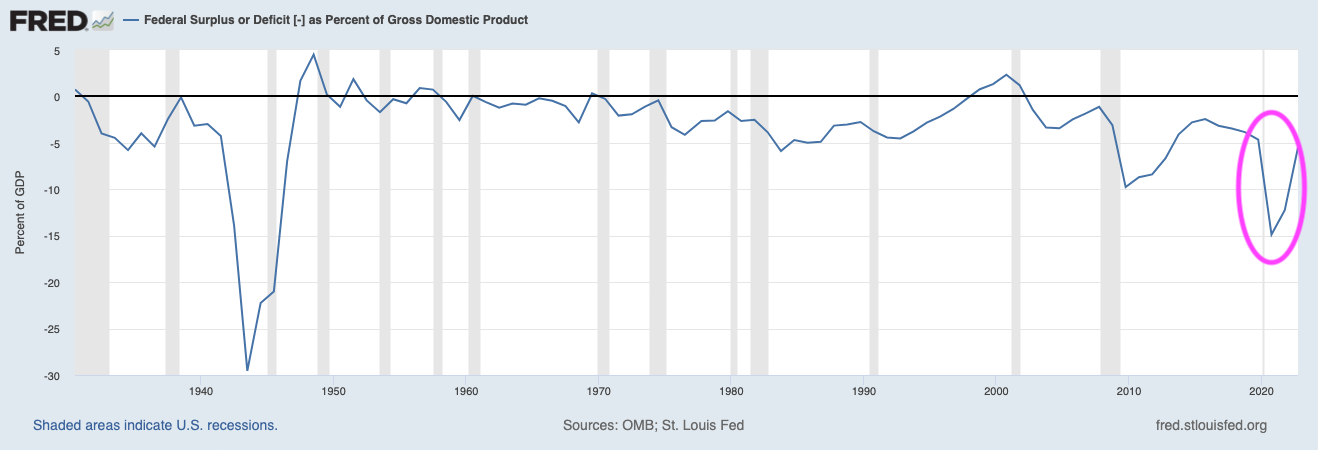

Unfortunately for Americans, the Fed isn’t the only entity that is engaged in inflationary policies. The Biden administration is currently engaged in truly extraordinary levels of money printing.

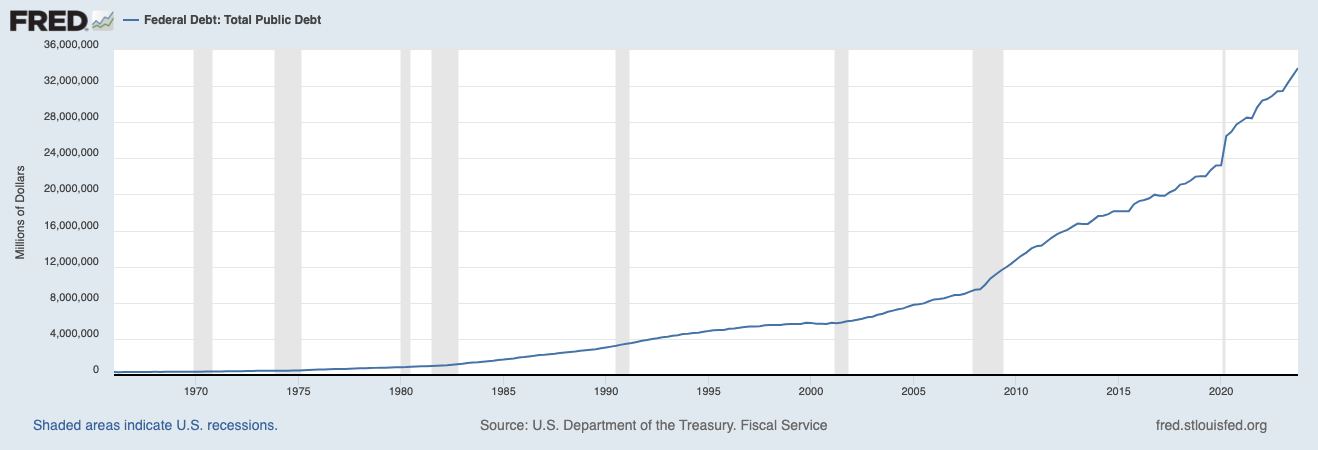

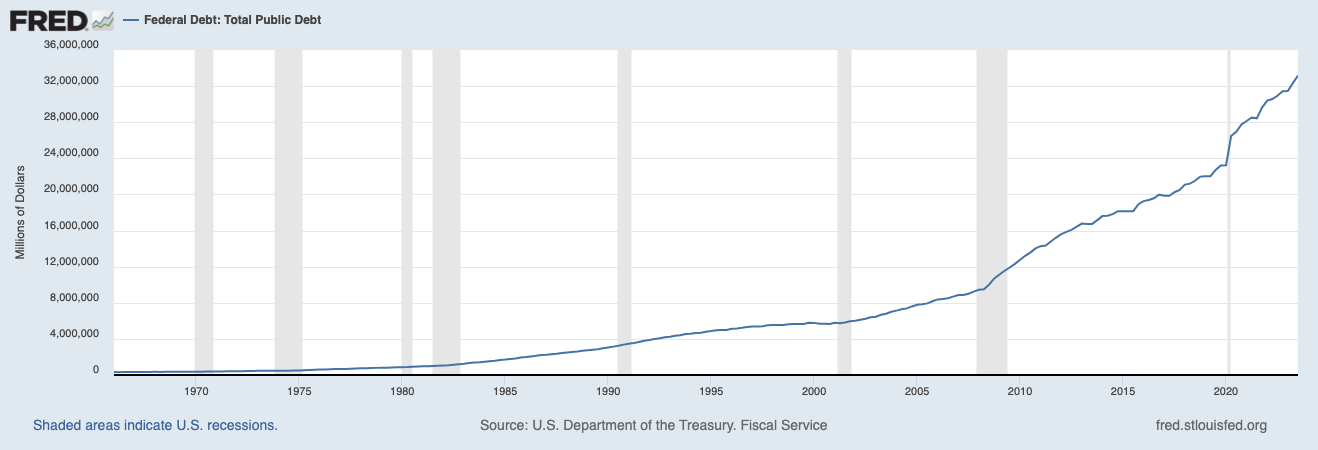

The Biden administration has added $6 trillion to the national debt since taking office. Bear in mind, this is happening at a time when the U.S. is collecting a record amount in taxes. So, the Biden administration is not only spending all of the tax dollars collected, it’s spending so much money that the U.S. is having to issue record amounts of debt!

The below chart needs no explanation. This is simply not sustainable.

Indeed, the pace of debt issuance is speeding up not slowing. The Biden admin issued $3 trillion in new debt in between 2021 and 2023. It added another $4 trillion in new debt in 2023 alone. At this pace. the U.S. will hit $40 trillion in debt some time in mid-2025.

Indeed, the pace of debt issuance is speeding up not slowing. The Biden admin issued $3 trillion in new debt in between 2021 and 2023. It added another $4 trillion in new debt in 2023 alone. At this pace. the U.S. will hit $40 trillion in debt some time in mid-2025.

The good news is that those investors who are properly positioned for this stand to generate truly EXTRAORDINARY returns in the coming months.

On that note, we recently published a Special Investment Report detailing three investments that will profit from this rampant government spending. Normally this report would cost $499, but we are giving copies FREE to anyone who joins our daily market commentary.

As I keep emphasizing, another round of inflation is coming.

And the worst part?

The Fed knows it, but is playing political games to boost the economy/ stock market for the Biden Administration.

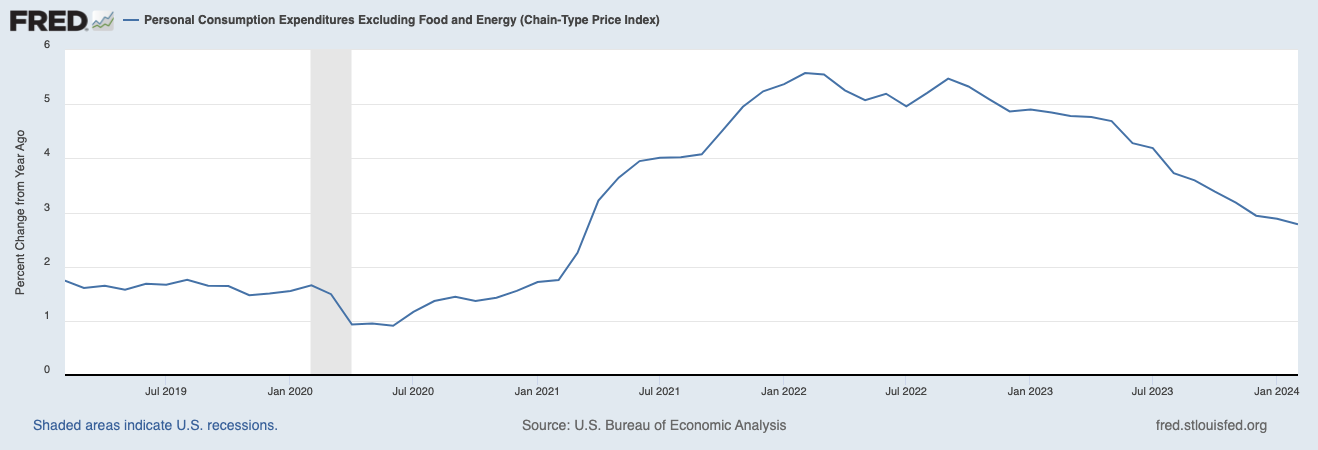

“But wait a minute, Graham,” you’re no doubt thinking, “the Fed’s preferred inflation measure is core-Personal Consumption Expenditures and that is trending down to the Fed’s 2% target.”

Let me let you in on a little secret… PCE is a terrible predictor of future inflation… and the Fed knows it.

The Fed is the largest employer of economics PhDs in the world. All told, the Fed has over 400 economics PhDs and 150 research assistants on payroll. As a result of this, the Fed is constantly doing research on various issues.

Back in 2001, the Fed had several researchers dive into the subject of inflation. Their goal was the analyze whether the Fed’s preferred measures of inflation (the CPI and the Personal Consumption Expenditures or PCE) are decent predictors of future inflation. The Fed also investigated a whole slew of other inflation measures for comparison purposes.

The results?

The Fed found that food inflation, NOT CPI or PCE, is the best predictor of future inflation. Fed researchers wrote the following:

We see that past inflation in food prices has been a better forecaster of future inflation than has the popular core measure [CPI and PCE]…Comparing the past year’s inflation in food prices to the prices of other components that comprise the PCEPI (as in Table 1), we find that the food component still ranks the best among them all…

Source: St Louis Fed (emphasis added).

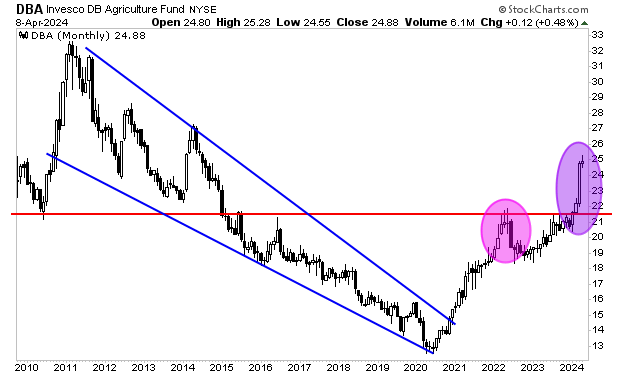

Now, food is derived from agricultural commodities. And what have agricultural commodities been doing in the last few months?

The first round of inflation is highlighted with a pink oval. The current price move is significantly larger. According to the Fed’s own research, this indicates a second wave of inflation is about to hit the US.

The good news is that those investors who are properly positioned for this stand to generate truly EXTRAORDINARY returns in the coming months.

On that note, the FREE copies of our Special Investment Report detailing three investments that will profit from the next round of inflation are rapidly being reserved. So if you want reserve one, you better move fast!

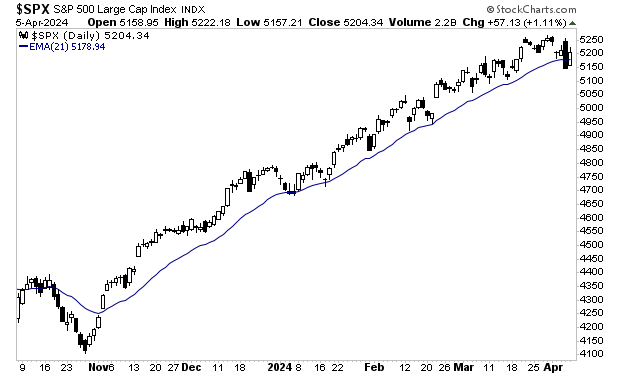

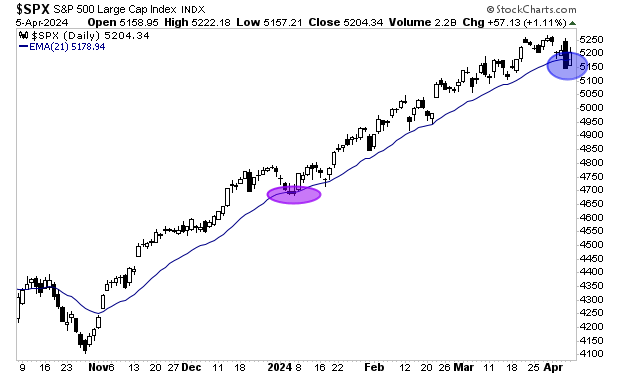

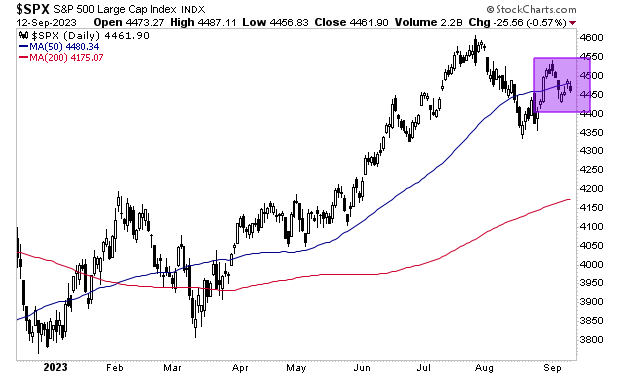

Ever since the S&P 500 bottomed in late October/ early November 2023, the 21-day exponential moving average (EMA) has served a major “trend line.” Put simply, whenever stocks fell to test this line, they “bounced” soon after and the rally continued.

Last week’s price action featured a different dynamic. Stocks fell to test the 21-EMA and struggled to reclaim it for two sessions (blue oval in the chart below). The only other time this happened was during the brief market pullback in early January 2024. At that time, the market rebounded sharply on the third trading session (purple oval in the chart below).

In this context, today’s price action is key. If the S&P 500 rallies hard and reclaims the 21-EMA, then it’s likely stocks will rally to new highs. However, if stocks cannot reclaim the 21-EMA with conviction today, then we’re likely to see more downside for stocks.

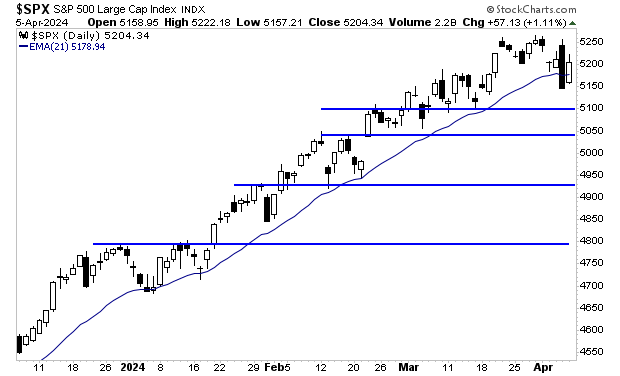

I’ve illustrated the S&P 500’s support lines in the chart below.

If you’re interested in taking advantage of a unique situation in the stock market today, the FREE copies of our Special Investment Report detailing three investments that can profit from inflation are rapidly being reserved. So if you want reserve one, you better move fast!

Our latest theme is that the U.S. Central Bank, called the Federal Reserve, or the Fed for short, is NOT politically independent, but is in fact a highly partisan organization that leans left.

The above items are not some conspiracy theory. The Fed’s own actions support this view.

By quick way of review…

1) The Bernanke-led Fed launched QE 3 just three months before the 2012 Presidential election. At the time, the economy was growing, unemployment was falling, and there were no signs of systemic duress in the financial system. So this was a clear intervention to aid the Obama Administration’s 2012 re-election bid.

2) The Fed kept rates at zero for seven of the eight years President Obama was in office. Once it finally got around to raising rates, it engaged in one of the feeblest hiking schedules in history, raising them only once in 2015

and once in 2016.

3) Donald Trump won the 2016 Presidential election in a major upset to the political establishment. At that point the Fed suddenly began raising rates three to four times per year while simultaneously draining $500 billion in liquidity from the financial system.

4) Today, the Fed is actively juicing the stock market via multiple credit facilities designed to provide liquidity to help the Biden administration with its re-election bid. The Fed is also promising to cut rates despite the fact it’s an election year and inflation has not fallen to its 2% target.

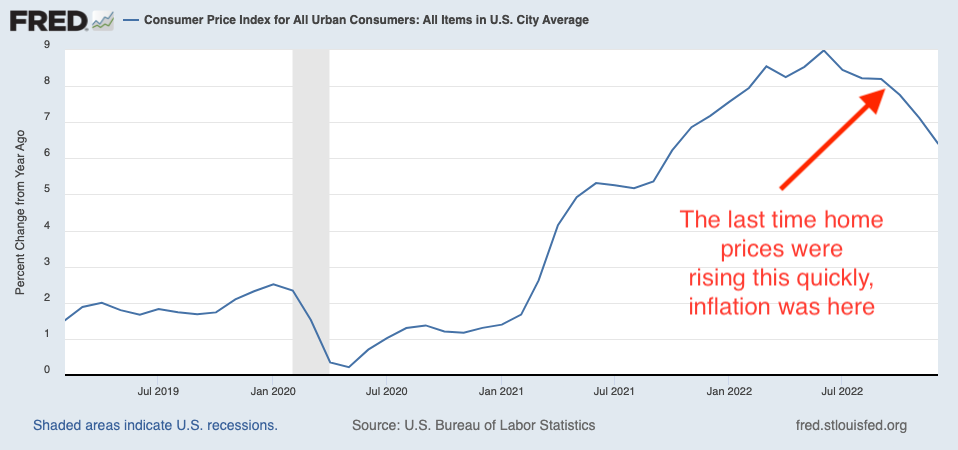

I wish this was the end of this disturbing exercise, but it’s not: the Fed is also letting housing bubble up again. The reason? You guessed it, real estate is the single most owned asset class in the U.S. And boosting home prices during an election year is likely to sway voters.

TheS&P CoreLogic Case-Shiller U.S. National Home Price Index rose 6% in January. This is up from 5.6% in December 2023. As HousingWire notes, this represents the seventh consecutive month of annual price growth. It’s also the biggest increase since November 2022.

By the way, inflation was around 6% at that time!

So we’ve got both real estate and stocks bubbling up again, courtesy of the Fed playing political games. In the near-term this is fantastic for Americans, who will see their net worth rise as a result of this.

The bad news is that there’s no such thing as a free lunch. And the Fed’s political shenanigans are unleashing a second wave of inflation.

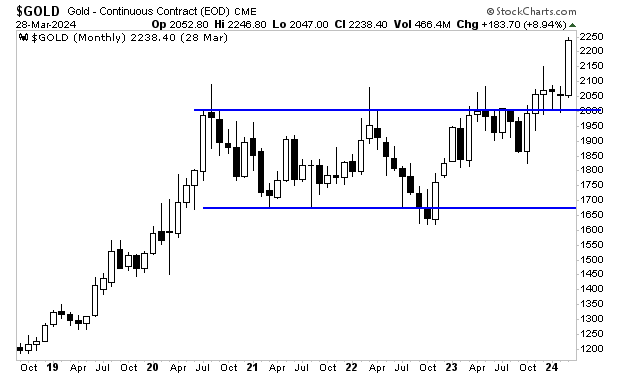

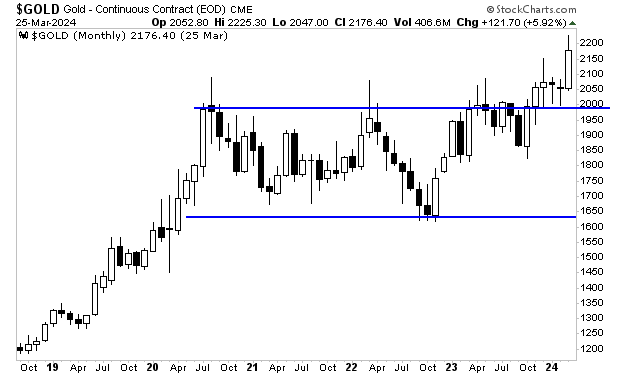

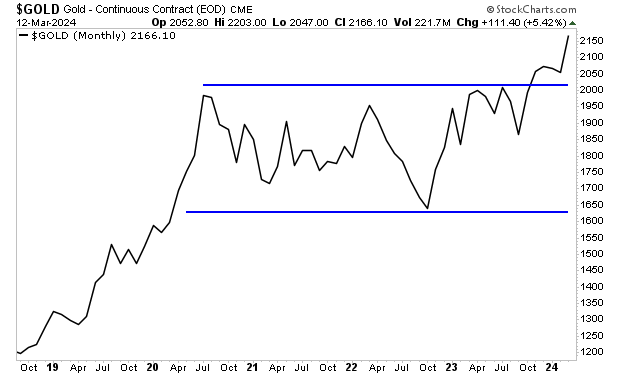

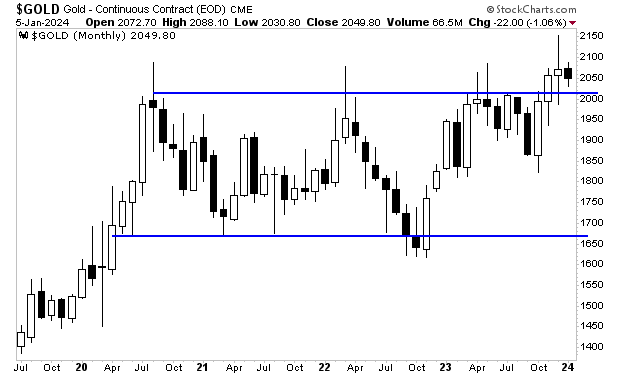

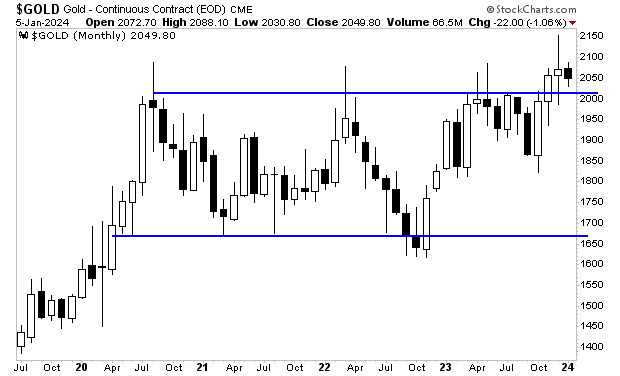

Gold has figured it out. It recently exploded to new all-time highs.

The good news is that those investors who are properly positioned for this stand to generate truly EXTRAORDINARY returns in the coming months.

On that note, the FREE copies of our Special Investment Report detailing three investments that will profit from the next round of inflation are rapidly being reserved. So if you want reserve one, you better move fast!

Yesterday, I detailed how the Fed is a political entity… and it leans left.

By quick way of review…

1) The Bernanke-led Fed launched QE 3 just three months before the 2012 Presidential election. At the time, the economy was growing, unemployment was falling, and there were no signs of systemic duress in the financial system. So this was a clear intervention to aid the Obama Administration’s 2012 re-election bid.

2) The Fed kept rates at zero for seven of the eight years President Obama was in office. Once it finally got around to raising rates, it engaged in one of the feeblest hiking schedules in history, raising them only once in 2015

and once in 2016.

3) Donald Trump won the 2016 Presidential election in a major upset to the political establishment. At that point the Fed suddenly began raising rates three to four times per year while simultaneously draining $500 billion in liquidity from the financial system.

It is possible that the above items are all coincidence. It’s also possible that Bigfoot could actually be Elvis living in disguise in the woods.

So what is the Fed up to now?

It’s trying to help President Biden win the 2024 Presidential election by juicing the two asset classes that have the largest impact on Americans’ net worth (stocks and housing ).

Today we’ll be assessing the stock market.

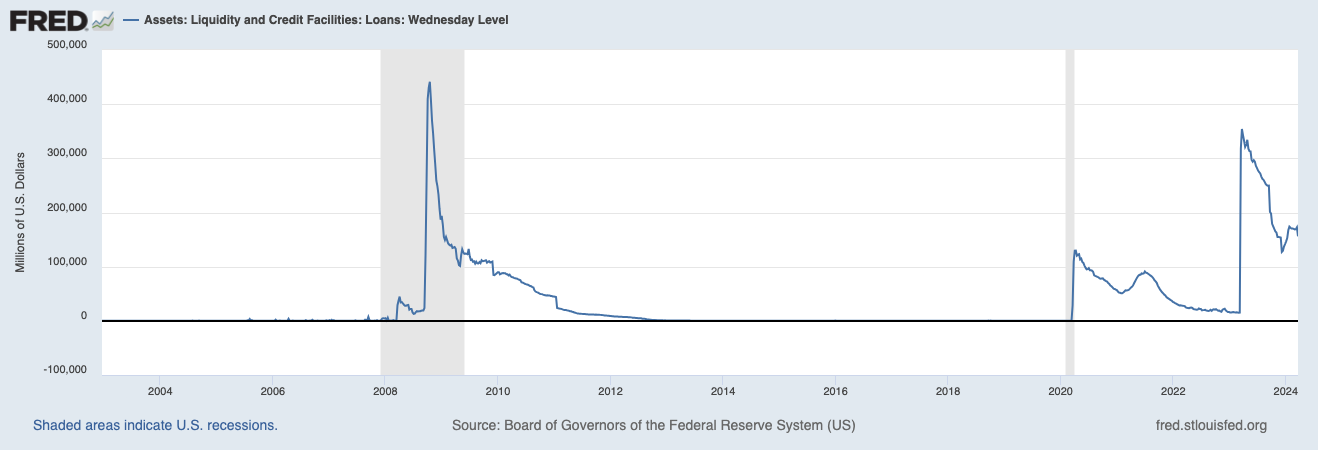

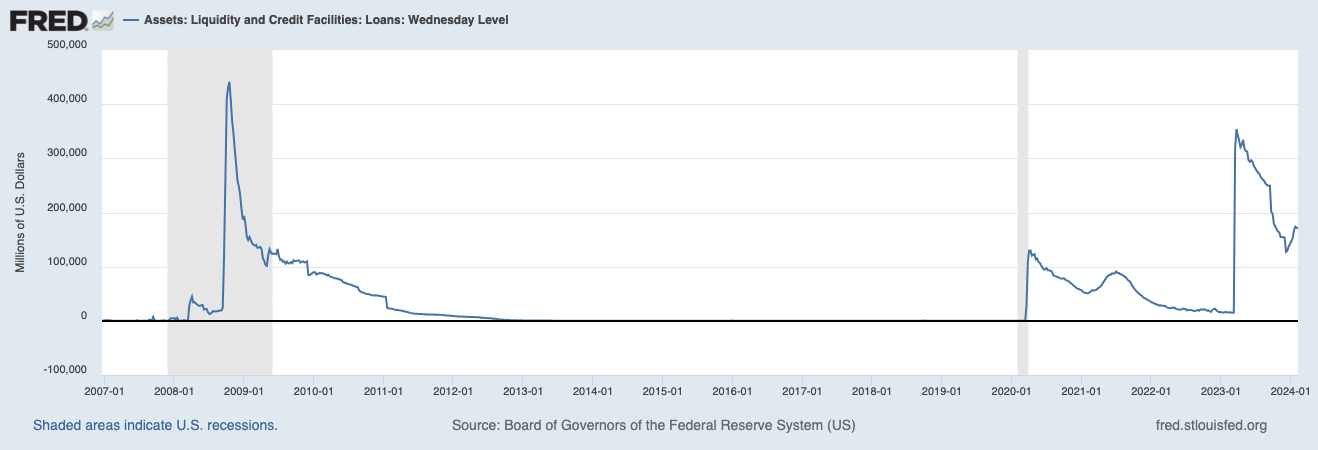

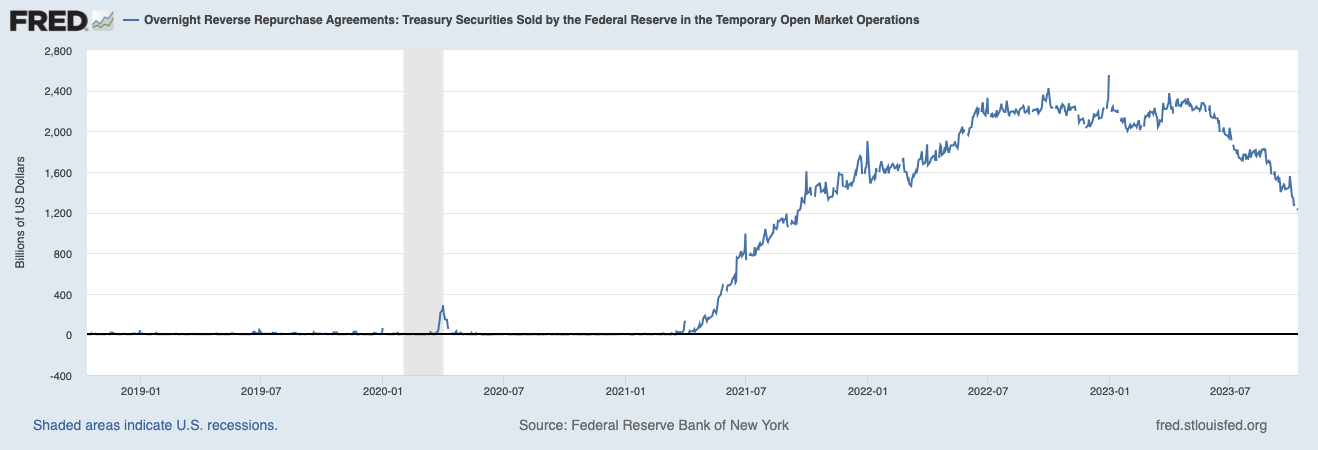

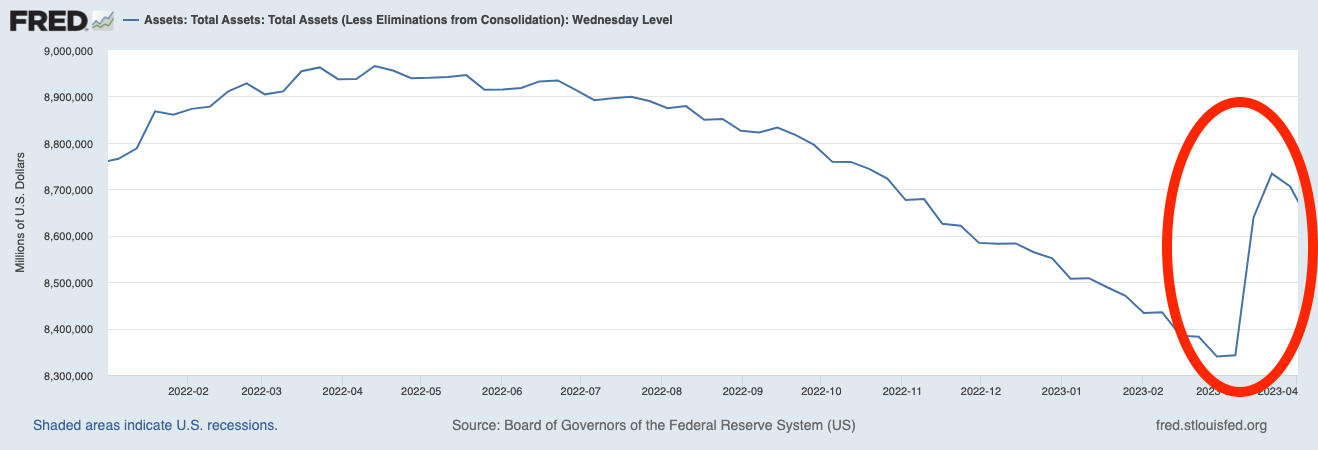

The Fed is supposed to be draining liquidity from the financial system via its Quantitive Tightening (QT) program. However, the Fed is ALSO providing $155 BILLION in liquidity via its overnight credit facilities. To put that into perspective, it’s more liquidity than the Fed was providing via this facility in MARCH 2009 right after the worst financial crisis in 80 years!

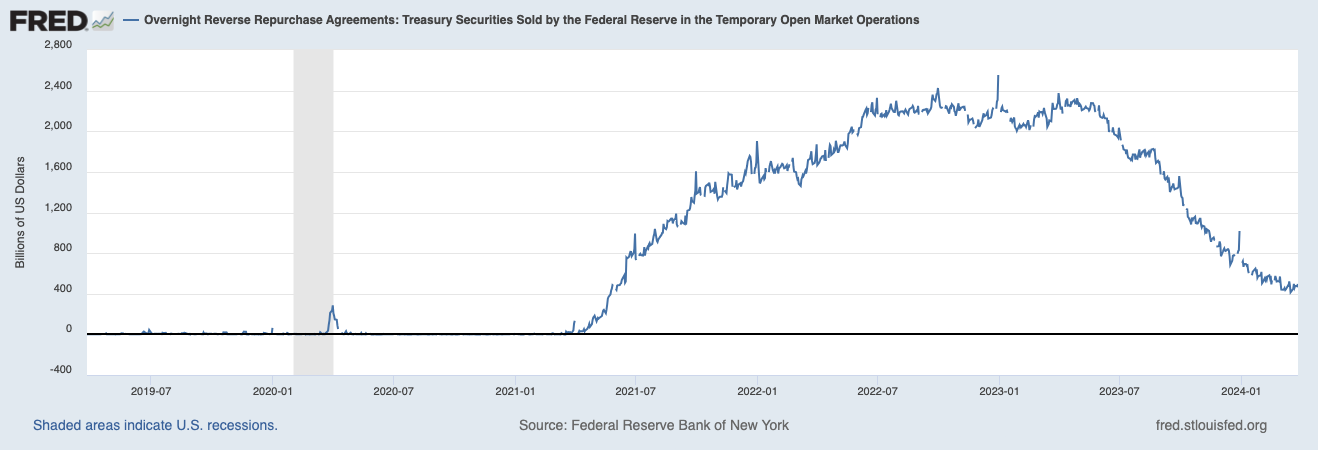

As if that’s not egregious enough, the Fed is ALSO providing nearly $500 billion in liquidity via a process called Reverse Repurchase Agreements.

Small wonder then that the stock market has been roaring higher. The Fed is providing EMERGENCY levels of liquidity to the financial system at a time when the economy is growing! So much for QT!

In the very simplest of terms, the Fed is juicing stocks higher to boost the Biden Administration’s 2024 re-election bid. And rest assured, I’ll detail how the Fed is doing the same thing with housing in tomorrow’s article.

The good news is that those investors who are properly positioned for this stand to see extraordinary gains.

On that note, the FREE copies of our Special Investment Report detailing three investments that will profit from the next round of inflation are rapidly being reserved. So if you want reserve one, you better move fast!

It’s time to tell the truth when it comes to Fed political interventions.

One of the biggest myths concerning the Fed is that it is politically independent. This is laughably false to anyone who has paid attention during the last 25 years.

Consider that in 2012, the Bernanke-led Fed announced QE 3, its largest QE program in history at the time (an $80 billion per month, open-ended program), a mere THREE MONTHS before the U.S. Presidential election.

Bear in mind, the U.S. economy was growing and the U.S. financial system wasn’t under significant duress at the time. So this was blatant political interference to aid the Obama Administration’s re-election bid by boosting the stock market and economy.

A second major example of Fed political bias concerns its major shift in monetary policy once Donald Trump became President. To fully grasp this, we need to provide a little historical context.

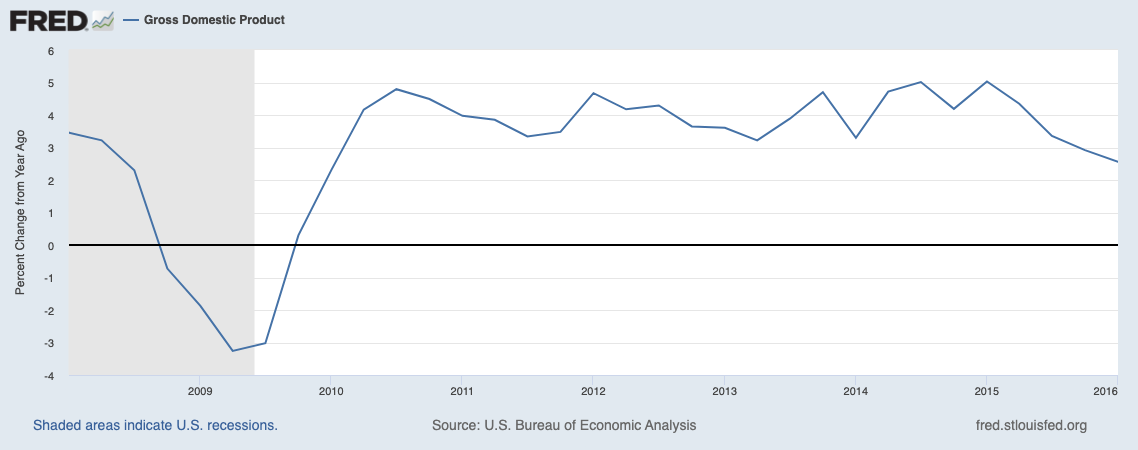

Between 2008 and 2016, the Fed engaged in eight years of extraordinary monetary easing, maintaining interest rates of 0.25% (zero), and engaging in over $3 trillion worth of QE from 2008 to 2015. Bear in mind that throughout this time, the U.S. economy was technically NOT in recession. Economic growth was steady:

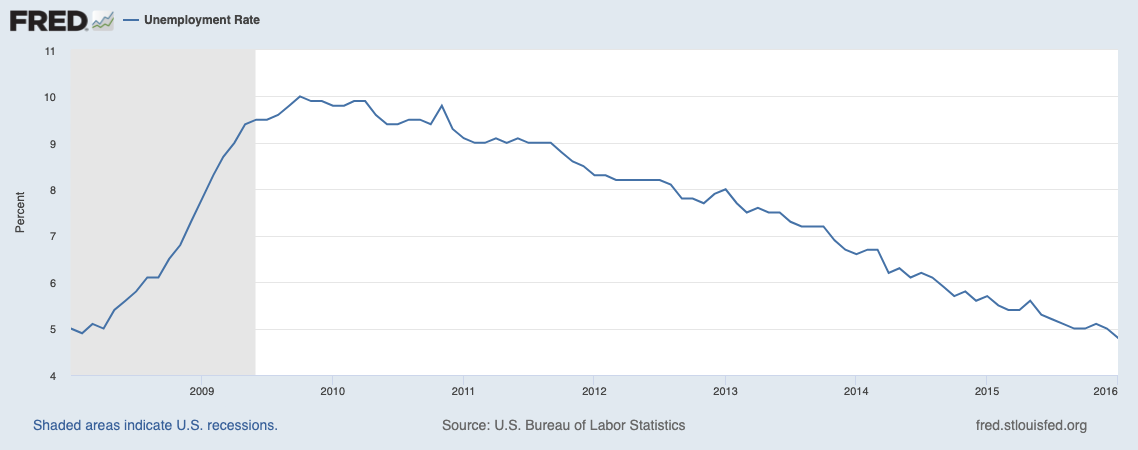

And the unemployment rate was in a clear downtrend:

Once the Fed actually ended easing, it embarked on one of the feeblest campaigns of tightening monetary policy in history, raising rates only one time in 2015 and 2016. I would note that all of this took place under the Obama administration.

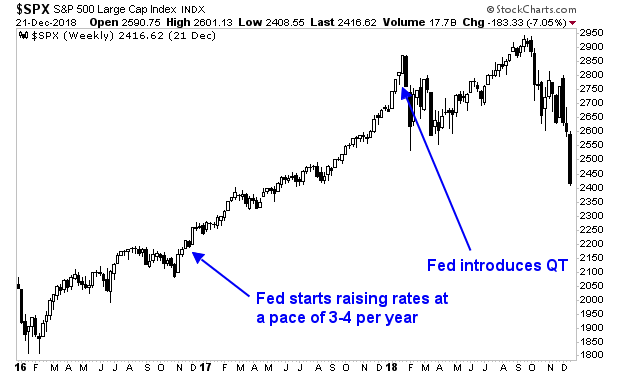

Then Donald Trump won the 2016 Presidential election, and suddenly the Fed “got religion” about normalizing monetary policy. It raised rates three times in 2017 and another four times in 2018. In 2018 it also began shrinking its balance sheet via a process called Quantitative Tightening or QT. It would ultimately drain $500 billion in liquidity from the financial system via QT in 12 months. That is quite a shift considering the Fed had maintained rates at or close to ZERO for eight years prior to this.

Throughout 2016-2018, the Fed ignored numerous signals that this pace of tightening was placing the financial system under duress, right up until the junk bond market froze and the U.S. stock market crashed 20% during the holidays in December 2018.

For those who would argue that the Fed’s sudden shift from maintaining easy monetary policy for the better part of a decade to aggressively normalizing policy in the span of 20 months had nothing to do with Donald Trump being President, consider that former Fed Vice Chair Stanley Fisher admitted in an interview that the Fed’s raising rates in December 2018 was done specifically to hurt the economy because the Fed was annoyed with President Trump’s constant tweeting about them.

So again… the Fed IS a political entity… and it leans LEFT.

I’ll detail what this means investors as we head into the 2024 President election in tomorrow’s article. But for now, gold is giving us a clue.

The good news is that those investors who are properly positioned for this stand to see extraordinary gains.

On that note, the FREE copies of our Special Investment Report detailing three investments that will profit from the next round of inflation are rapidly being reserved. So if you want reserve one, you better move fast!

Last week, the Fed confirmed that it intends to cut rates three times this year, despite the fact inflation is NOT near its target of 2% and is in fact turning back up.

If you’re scratching your head on this, there’s a very simple answer:

It’s an election year. And the Powell Fed is stacked with political hacks.

It is clear that the Powell Fed is full committed to aiding the Biden administration in its re-election bid. After all, why else would the Fed talk about triggering an easing cycle when:

1) The stock market is at all-time highs.

2) Financial conditions are looser now than they were BEFORE the Fed starting raising rates in 2022.

3) The economy is growing, NOT slowing down.

4) Inflation is turning back up.

These are the sorts of conditions in which the Fed usually RAISES rates. Instead, the Fed is going to start cutting rates AND reducing the pace of its Quantitative Tightening (QT) program.

Both of those are HIGHLY inflationary.

In this context, it is clear the Fed has become a political entity. There is no credible economic/ financial reason for the Fed to commit to these policies. At the very least, the Fed should remove one rate cut from its forecast for 2024.

Instead, it is clear that the Fed is committed to pushing stocks and housing as high as possible going into the 2024 Presidential election. This will be a boon for Americans in the short-term, but the consequences will be devastating in the coming months as inflation eviscerates incomes and investment portfolios.

The good news is that those investors who are properly positioned for this stand to see extraordinary gains.

On that note, the FREE copies of our Special Investment Report detailing three investments that will profit from the next round of inflation are rapidly being reserved. So if you want reserve one, you better move fast!

I’ve previously explained in great detail that the official inflation measure, the Consumer Price Index or CPI, is massaged to the point of being a work of fiction.

Among the more egregious gimmicks employed by the BLS:

Data collection consists of surveys with low response rates.

Those being surveyed are asked to remember what they paid for goods and services (as if anyone keeps an excel spreadsheet of that stuff).

The CPI doesn’t consider food or energy prices.

The CPI doesn’t use real world measures for shelter, instead relying on carefully crafted artificial metrics that have no connection to reality.

And so on.

However, if you’re looking for one simple explanation that the CPI is fiction, you need look no further than the Biden administration’s poll numbers.

President Biden is an historically unpopular President. This is truly astonishing when you consider that his opponent for the 2024 election (former President Trump) is one of the most polarizing and unappealing candidates in history.

Why are Biden’s polls so bad?

Inflation.

Americans vote based on many factors, but ultimately, they tend to vote with their pocket books. And inflation is a MAJOR problem for the bottom four quintiles (lower 80%) of Americans based on net worth/ income.

The media shills and hacks like to argue that Biden is unpopular because Americans are “wrong” or “misguided” due to “disinformation.” But we have to remember that these are the same people who told us inflation was “transitory” for most of 2021 and 2022. Their track record is truly abysmal when it comes to accurately assessing reality.

Bottomline: inflation has NOT come down, no matter what the BLS and media tell you. And those investors who don’t prepare for what’s coming are in for a world of hurt.

I’ll detail what this means for the markets in tomorrow’s article.

If you’ve yet to position your portfolio to profit a resurgence in inflation, we just published a Special Investment Report outlining the clear signals that inflation is back as well as THREE unique investments that could EXPLODE higher as inflation takes hold of the financial system later in 2024.

This report went live just four days ago. And already two of these investments are up.

The Fed is screwing up… again. And investors who don’t prepare for what’s coming are in for a NASTY surprise in the coming months.

To understand what I mean by this, let me provide some context.

Starting in November of 2023, Fed officials began proclaiming that inflation had been tamed. The argument, at the time, was that inflation data was clearly trending down, while rates were much higher, so the Fed would need to start cutting rates soon to avoid crushing the economy.

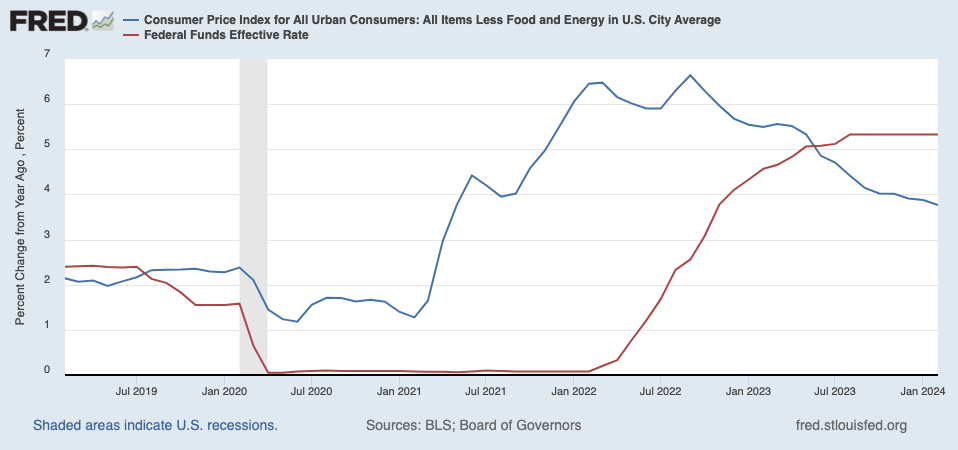

I realize this is difficult to picture, so I’ve included the below image for you. The Fed Funds Rate is the red line. The official inflation measure, the Consumer Price Index, or CPI for short, is the blue line. As you can see, starting in mid-2023, the red line was much higher than the blue line.

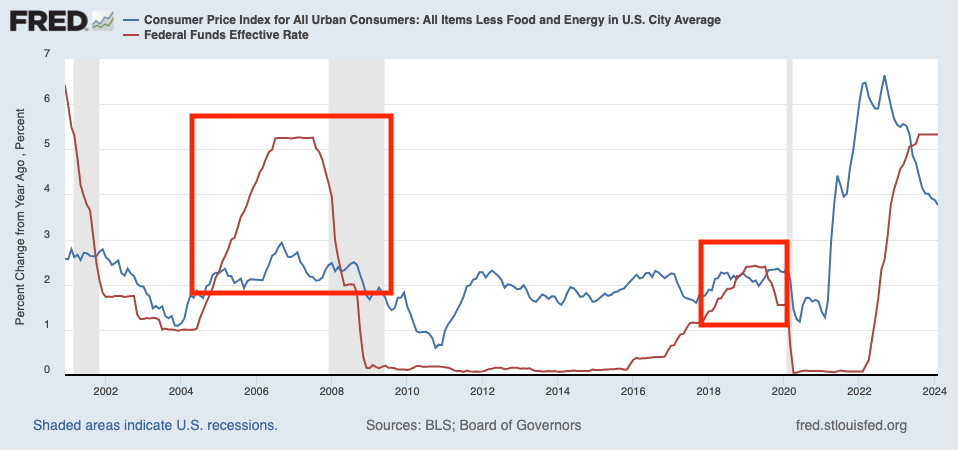

During the last 25 years, any time the Fed Funds Rate has been much higher than inflation for long, something BAD has happened (a recession or crisis). I’ve illustrated this on the below chart with red rectangles.

This is why the Fed started talking about cutting interest rates in November 2023, despite the fact inflation was still well above 3%, while the Fed’s target for inflation was 2%. In the very simplest of terms, the Fed was “betting” that inflation would continue to trend down, therefore giving the Fed the excuse to cut rates.

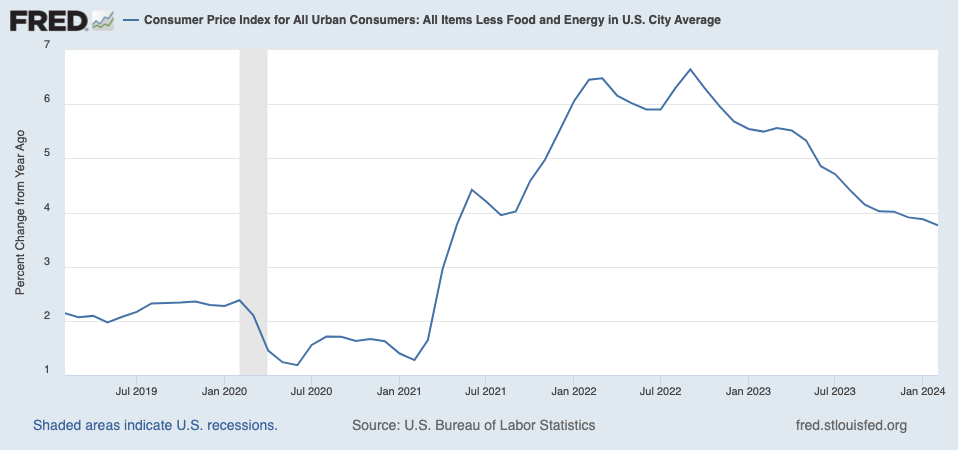

However, since that time, the CPI has stopped declining as rapidly. The trend, while still down, isn’t nearly as strong.

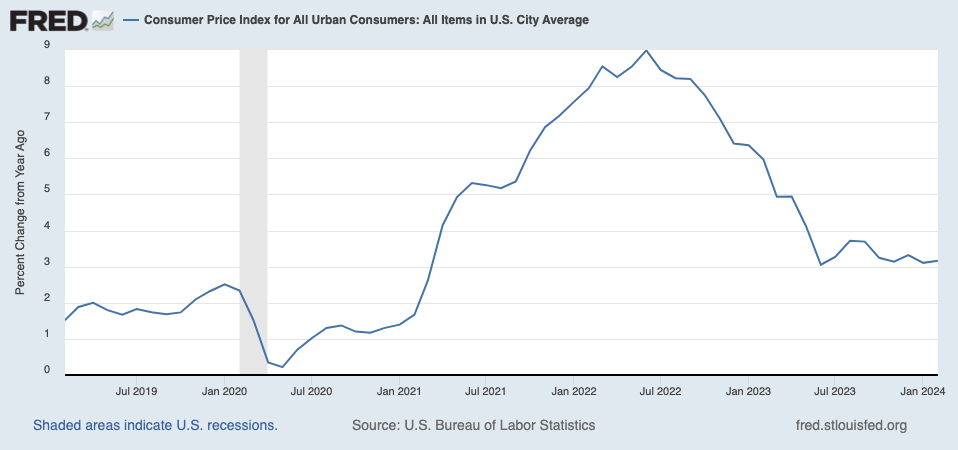

Indeed, the situation looks much uglier when we include food and energy prices to inflation. As I noted in yesterday’s article, the ONLY reason inflation appears to have declined as much as it has is because energy prices have collapsed year over year. Once you include energy data in the inflation measure, things look like this:

Put simply, the Fed has screwed up… again. The Fed promised it would cut rates base on an assumption that has proven false. This opens the door to a serious upset for the markets in the coming weeks.

If you’ve yet to take action to profit a resurgence in inflation, we just published a Special Investment Report outlining the clear signals that inflation is back as well as THREE unique investments that could EXPLODE higher as inflation takes hold of the financial system later in 2024.

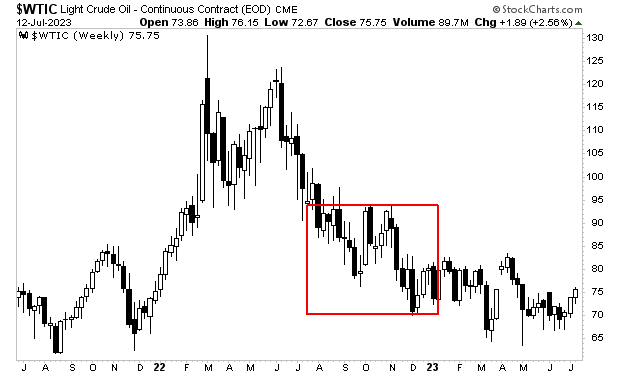

Throughout 2023, I warned that inflation was not really disappearing from the financial system. Time and again I noted that the ONLY data in the inflation measure that had declined was energy prices.

This trend continues to this day, by the way. See for yourself.

Take out energy prices (and used cars) and the inflationary data is still RISING in every category.

And things are going to get worse soon.

Why?

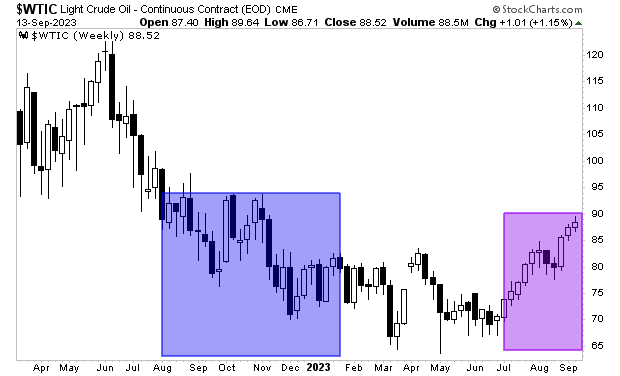

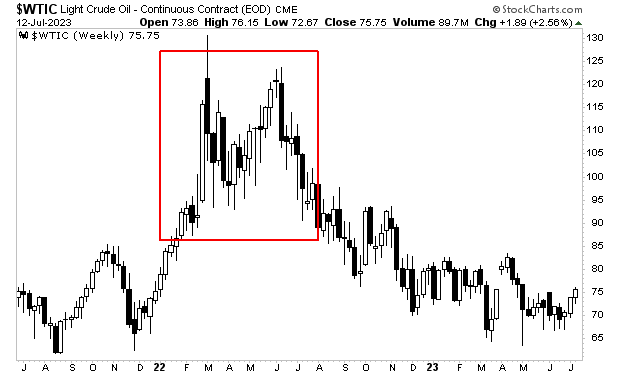

Energy prices will soon no longer be DOWN year over year. For 12 months, the CPI has been calculated by comparing the prices in the blue rectangle to prices in the purple rectangle. However, in 2024, prices will be compared to the blue rectangle for inflation calculations.

We’ve now had two months of the CPI surprising to the upside. And this is while Energy prices are HELPING the inflation data. What happens when Energy is no longer down on a year over year basis?

Hint: gold has already figured it out. Other asset classes will soon.

If you’ve yet to take action to profit a resurgence in inflation, we just published a Special Investment Report concerning THREE investments you can use to make inflation pay you as it rips through the financial system in the months ahead.

The report is titled How to Profit from Inflation: Three Investments to Make Money”. And it explains in very simply terms how to make inflation PAY YOU.

We’re picking up where we left off our A Deep Dive Into What AI Means For Corporate America investment series. If you missed the first two parts from this series, you can access them hereandhere.

By brief way of review:

Artificial Intelligence (AI) is the dominant theme in the investing world today.

Currently AI is capable of accessing vast swathes of available information and integrating it in such a way that AI appears to be creating something from scratch.

Current AI models are being deployed in practically every sector of the economy from entertainment to marketing, operations and more.

While the areas of the economy that AI is impacting are different, the implications are all the same:

Improving productivity (getting more results for less effort).

This is why AI is so exciting for the economy and investors. In a best-case scenario, AI will lead to a massive increase in profitability as revenues grow and costs decrease. And that is what has triggered a kind of mania for AI-related stocks.

The flipside of this is that AI is currently a kind of Wild West in which “anything goes.” There are no legal, legislative, or societal frameworks for this technology. As a result, advances are being made with few if any ethical considerations.

In this sense, AI is following a pattern we’ve seen with other technological revolutions in the past. That pattern consists of two phases is:

The initial breakthrough phase, which occurs before social/legal frameworks are in place.

The “normalization” phase during which social/legal frameworks are implemented, giving the technology a societal and financial legitimacy.

If you need a real-world example of this, think of the electronic music file or MP3 revolution.

The first phase was Napster in 1999, which featured the sharing of music in what was later deemed as illegal activity (the legal framework was not yet ready for the technology). During this initial phase Napster exploded in popularity particularly among young people. At its peak Napster had tens of millions of users. Then came the lawsuits, Napster went bankrupt, and social/ legal frameworks were introduced for this new technology. During this time Apple introduced iTunes: a version of MP3 technology in which MP3s could be bought and sold in a legally acceptable form.

Napster is still around. Its marketing promotes the fact it is “100% legal.” And it has about five million users. By way of contrast, at its peak, iTunes had 500+ million users and accounted for 63% of all digital music sales. It is now in the process of being converted over to Apple Music, a new service that also offers music streaming and other services in order to compete with Spotify which is the new market leader. So once again, the technology has changed and requires adaption.

AI as it stands today, is in its “Napster” phase. As investors we can profit from this by riding key players in the space, but we need to do so with our eyes open to risks, in particular the risk that at some point, the threat of a regulatory framework for AI will appear. And when it does, much of the “froth” in AI stocks will disappear as hot money/ momentum investors leave the space out of fear.

This doesn’t mean that AI will be “dead” at that time. Indeed, the BIG money will be made as market leaders emerge from the ashes of that collapse.

We’ll delve deeper into this in tomorrow’s article…

In the meantime, if you’re interested in profiting from this technological revolution, we are currently putting the finishing touches on a special investment reporting that outlines some of the larger implications for AI as well as several of the most likely market leaders.

To receive this special report when it’s published later this week, all you need to do is sign up for our FREE daily investment commentary Gains Pains & Capital.

We’re picking up where we left off our A Deep Dive Into What AI Means For Corporate America investment series. If you missed the first part from this series last week, you can access it here.

By brief way of review:

Artificial Intelligence (AI) is the dominant theme in the investing world today.

Currently AI is capable of accessing vast swathes of available information and integrating it in such a way that AI appears to be creating something from scratch.

We’ve already detailed the impact this technology will have on the entertainment industry: creating videos/ movies/ commercials used to require dozens of people (directors, actors, lighting technicians, sound technicians, editors, etc.) Courtesy of AI, ONE person can serve all of those functions.

Today, we’re going to assess the impact AI can have on other industries.

In the corporate world, AI can perform many tasks that previously required several people if not entire departments. AI can write an entire marketing piece and even create a visual advertisement for a product using a few words/ phrases entered by one user.

Interactive Investor recently used to AI to develop an entire online marketing campaign including thousands of ads and keywords. The results saw an increase in account creation and decrease in acquisition costs.

AI can do legal work as well, performing document review, analyzing contracts, and even preparing a deposition. There are now several examples of AI “legal assistants” located online.

AI can even alter business operations. Whole Foods has begun introducing “Just Walk Out” stores in which you simply walk in, take whatever you want from the shelves, and walk out. Sensors and cameras take care of the payment side of things.

The above examples of AI technology pertain to very different areas of the economy: making movies, performing legal diligence, shopping for groceries, etc. However, for investors, the implications of AI all boil down to just two items:

Improving productivity (getting more results for less effort).

This is why AI is so exciting for the economy and investors. In a best-case scenario, AI will lead to a massive increase in profitability as revenues grow and costs decrease. And that is what has triggered a kind of mania for AI-related stocks: Nvidia, Super Micro Computers, etc.

The flipside of this is that AI is currently a kind of Wild West in which “anything goes.” There are no legal, legislative, or societal frameworks for this technology. As a result, advances are being made with few if any ethical considerations.

We’ll be assessing those in tomorrow’s article.

In the meantime, if you’re interested in profiting from this technological revolution, we are currently putting the finishing touches on a special investment reporting that outlines some of the larger implications for AI as well as several of the most likely market leaders.

To receive this special report when it’s published later this week, all you need to do is sign up for our FREE daily investment commentary Gains Pains & Capital.

Artificial Intelligence (AI) is the dominant theme in the investing world today.

If you’re unfamiliar with AI, the concept is as follows: AI represents technology that can “think for itself.”

That sounds pretty advanced, but the reality is that AI in its current form is something of a misnomer. What I mean by this is that the technology doesn’t actually “think,” rather it accesses vast swathes of available information and integrates it in such a way that AI appears to be creating something from scratch.

The results can be incredible or ridiculous, depending on your perception.

For example, below is a screenshot from a video that was generated by an AI technology called “Sora.” The image on the left is a photo of a real person. The image on the right is a still shot from a video that was generated by AI to show the woman singing the lyrics to a pop song. AI took the fixed image from the left and generated a full 90 seconds of facial movements to make it appear as if the woman was singing a song. It’s astonishing.

H/T Min Choi

The obvious implication here is that AI will be highly disruptive for the entertainment industry. Previously, creating movies required dozens of people (directors, actors, lighting technicians, sound technicians, editors, etc.) Courtesy of AI, ONE person can serve all of those functions. This is why the Writers Guild of America (screenwriters) writers went on strike last year: many if not ALL of these people are in danger of losing their jobs as AI progresses.

The entertainment industry isn’t the only part of the economy at risk of disruption by AI.

I’ll detail what AI means for other industries tomorrow. But in the meantime, if you’re interested in profiting from this technological revolution, we are currently putting the finishing touches on a special investment reporting that outlines some of the larger implications for AI as well as several of the most likely market leaders.

To receive this special report when it’s published, all you need to do is sign up for our FREE daily investment commentary Gains Pains & Capital.

I’m about to share the single most important thing about investing in Artificial Intelligence (AI) today…

If you keep this in mind, you’ll avoid the basic mistake that 99% of investors are making when they put capital to work in AI.

Are you ready? Here it comes…

Over 99% of commentators have no idea what they’re talking about.

I’m not trying to be rude, nor facetious. There are plenty of brilliant, insightful people commenting about AI today. But investors often act as if strategists and analysts are psychic.

They’re not.

Human innovation is too messy, chaotic, and ever-changing for lots of people to accurately predict. This is especially true when it comes to technological revolutions with far-reaching implications.

If you don’t believe me, let’s consider what happened with search engines, one of the recent technological revolutions that produced incredible profits for investors who played it correctly.

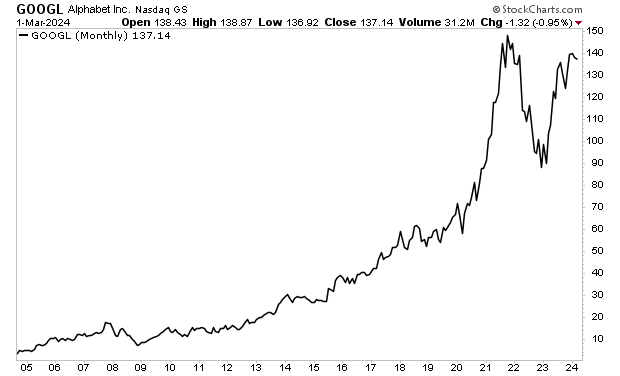

Today, Alphabet (GOOGL) is THE search engine of the world, accounting for over 90% of global searches. At a market cap of $1.7 TRILLION company, it is one of the 10 largest companies in the world. It routinely produces tens of billions of dollars in profits. In fact, its 2023 profits were greater than the market capitalizations of Ford (F) and U.S. Steel (X) combined.

However, back in the 1990s when search engine technology first came to market, Alphabet (then Google) wasn’t a market leader. Rather, the company was competing for market share with numerous other firms including Yahoo!, Hot Bot, Excite, Ask Jeeves, AltaVista, AOL Search, MSN Search and others.

Indeed, at that time, Yahoo! was the largest search engine company with a market capitalization of $125 billion. In fact, Yahoo! had a chance to buy the Alphabet for just $1 billion in 2002! Fast forward to 2017, and Yahoo! was sold to Verizon for less than $5 billion… by which point Alphabet was a $730 billion company.

Who saw that coming?

My point here is that, the internet, specifically search engines, represented an incredible revolution that changed the world. However, few if any people were able to accurately predict how it would play out.

And this didn’t just concern picking winners vs. losers… it also concerned the technology as a whole: many investors thought that the Tech Crash of the early ’00s meant that the opportunity for profiting from search engines was over. They couldn’t have been more wrong as the below chart illustrates.

The great news is that those who were able to navigate the markets to profit from search engines made truly STAGGERING amounts of money. And if you could pick the future market leaders in advance… while riding the booms and busts with proper risk management… well, the above chart of Alphabet shows you the kind of returns you could generate.

Thus, the key for investing in AI today is determining who the future leaders will be. That’s where the REAL money will be made.

We are currently putting the finishing touches on a special investment reporting that outlines some of the larger implications for AI as well as several of the most likely market leaders.

To receive this special report when it’s published, all you need to do is sign up for our FREE daily investment commentary Gains Pains & Capital.

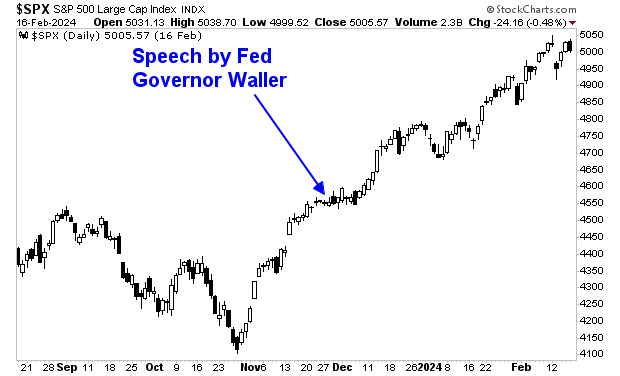

Inflation is going in the wrong direction again… and that is BAD news for stocks.

If you’ll recall, the primary driver of the recent rally in stocks was the Fed suggesting that it would soon begin cutting rates. Indeed, it was a speech by Fed Governor Waller concerning that exact topic in late November 2023 that ignited the move from 4,550 to new all time highs for the S&P 500.

However, with the economy still growing at an annualized rate of 3%, stocks at new all-time highs, and financial conditions looser today than they were before the Fed starting raising rates in March 2022, the ONLY way the Fed could cut rates without looking like a group of political activists is if inflation is at or close to target.

It’s not. In fact, the latest inflation data is going the WRONG way for the Fed.

The Consumer Price Index (CPI) for January was supposed to show a month over month (MoM) increase of just 0.2% and a year over year (YoY) increase of 2.9%. Instead it showed a MoM of 0.3% and a YoY of 2.9%).

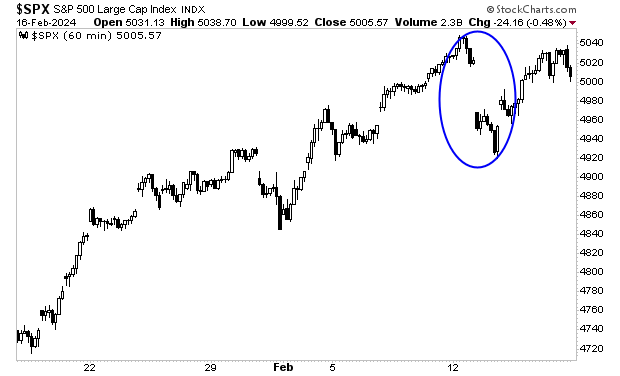

That 0.1% difference in MoM and 0.2% difference in YoY don’t sound like a big deal, but this was the reason the market dropped like a brick last week on Tuesday.

Then, on Friday, January’s Core Producer Price Index (PPI) came in at 0.5% MoM vs. expectations of 0.1%. Now that is a legitimately big deal as Core PPI is the Fed’s PREFERRED inflation measure.

This means there will be NO rate cuts in March. And investors will be lucky if they get a rate cut in April/ May.

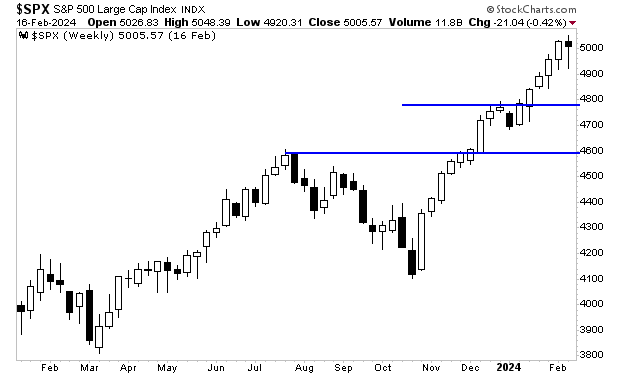

This sets the stage for a significant stock market correction. I’ve warned repeatedly that stocks are quite stretched above their primary trend. I believe the S&P 500 will be working its way down to 4,800 and then eventually 4,600 in the coming weeks. I’ve illustrated those levels on the chart below.

If you’re looking to take your trading to the next level, we’ve identified a simple strategy for riding rallies, avoiding corrections, and potentially beating the market by a wide margin. And best of all, it only takes about five minutes a day to use it! And despite this simplicity, it is INCREDIBLY profitable.

To find out what it is and how it works, and what it is saying about the markets today, all you need to do is join our FREE daily investment commentary GAINS PAINS & CAPITAL. You’ll immediately be given access to an investment report detailing this trading strategy so you can start using it today!

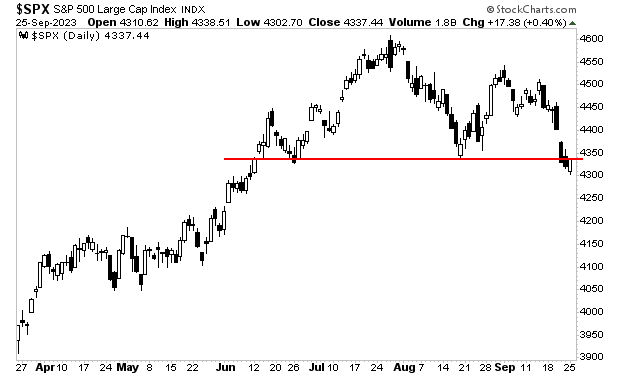

The S&P 500 looks primed for a correction of sorts.

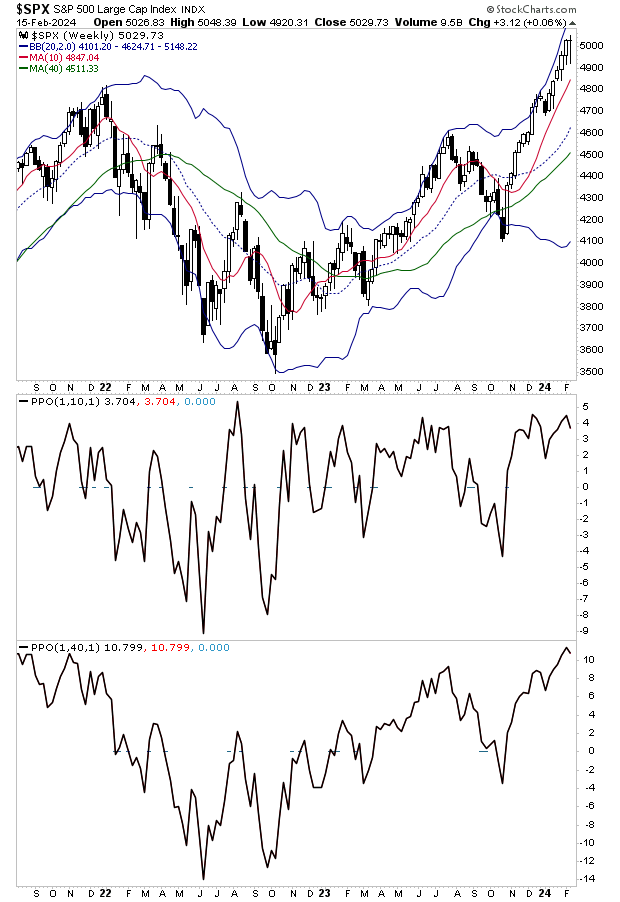

As I’ve noted previously, the S&P 500 is quite extended above both its 10-week moving average (same as the 50-DMA) as well as the 40-week moving average (same as the 200-DMA). Historically, this degree of extension above both trendlines has marked a temporary top as the below chart illustrates.

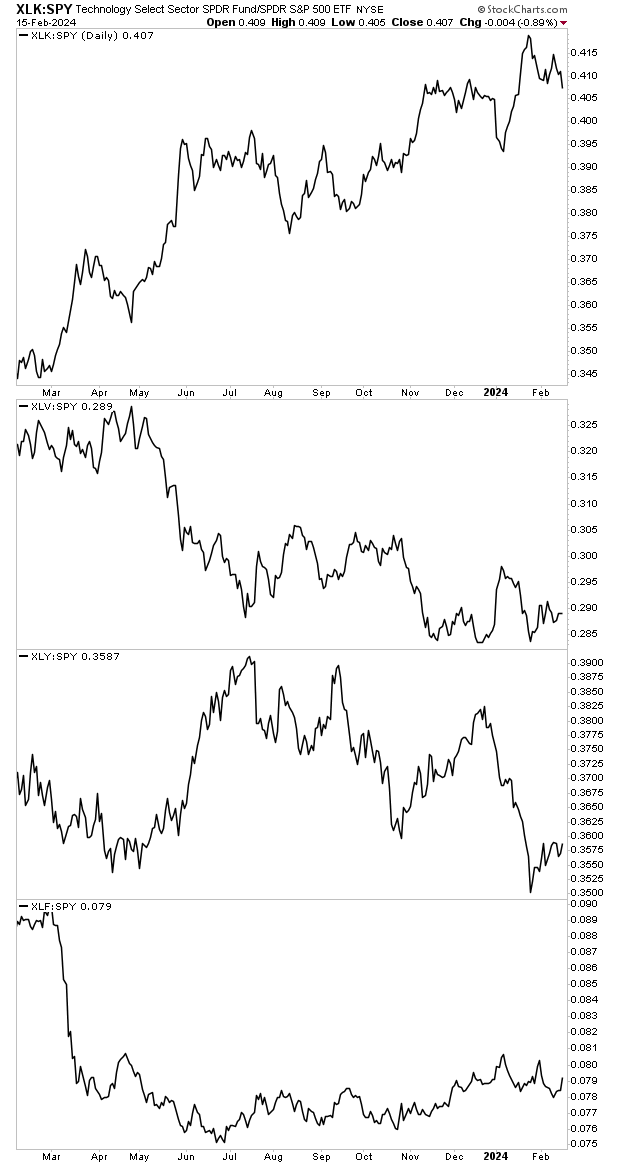

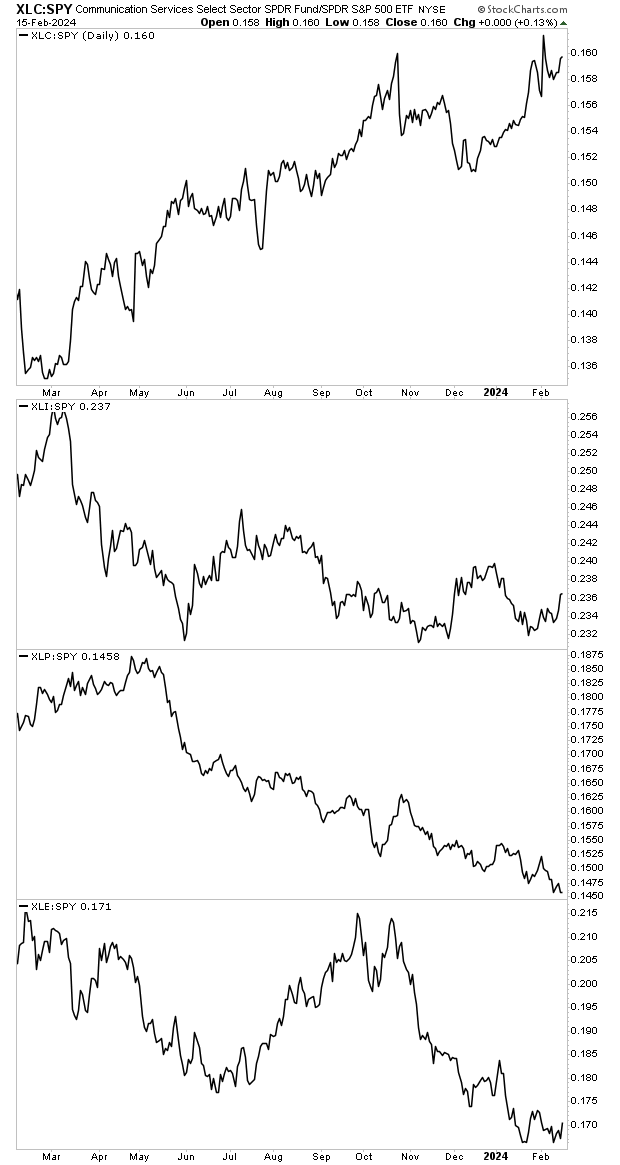

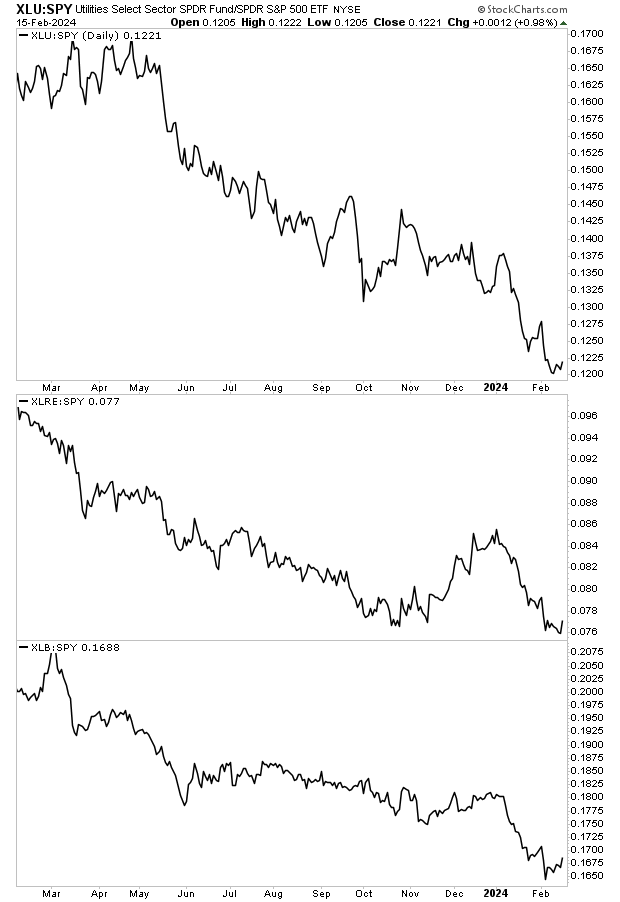

Beyond this, NO sector is outperforming the S&P 500 at this time (maybe with the exception of Communication Services).

Below are three charts showing the ratio performance between each sector in the S&P 500 and the broader index. When the individual sector outperforms, the line rises. When the individual sector underperforms, the line falls. As you’ll note, NO SECTOR is leading the market higher right now.

Tech, Healthcare, Consumer Discretionary and Financials:

Communication Services, Industrials, Consumer Staples, and Energy.

Utilities, Real Estate and Materials:

Looking at the above ratios, we note that Tech, Consumer Discretionary, Financials and Real Estate lead the market higher during the rally from early November until the end of 2023. However, today, not one single sector is leading the overall market higher (maybe with the exception of Communication Services). Even the Tech sector, which usually is a market leader has been underperforming the broader index since January.

So how has the market held up despite every sector underperforming?

A handful of stocks have pulled the overall market higher. Specifically, Nvidia (NVDA), Amazon (AMZN), Meta (META), and Eli Lilly & CO (LLY). Remove those companies from the S&P 500 and stocks are effectively flat.

Add it all up, and the above analysis suggests that “under the surface” the S&P 500 could see a decent correction of 5% or more in the coming weeks. Only a small handful of stocks are holding everything up. This combined with our overbought and overextended the market is suggests the momentum for the next market move will be DOWN.

If you’re looking to take your trading to the next level, we’ve identified a simple strategy for profiting from the market that is on par with anything before.

If you’re looking to take your trading to the next level, we’ve identified a simple strategy for catching rallies, avoiding corrections, and potentially beating the market by a wide margin. And best of all, it only takes about five minutes a day to use it! And yet, despite this simplicity, it is INCREDIBLY profitable.

To find out what it is and how it works, all you need to do is join our FREE daily investment commentary GAINS PAINS & CAPITAL. You’ll immediately be given access to an investment report detailing this trading strategy so you can start using it today!

Yesterday, I outlined how the Fed and the Treasury are actively working to juice the financial system to aid the Biden administration’s re-election bid.

By quick way of review:

1) The Fed will soon begin cutting interest rates while stocks are at all time highs, the economy is still growing, and financial conditions are in fact looser than they were before the Fed raised rates for the first time in March 2022.

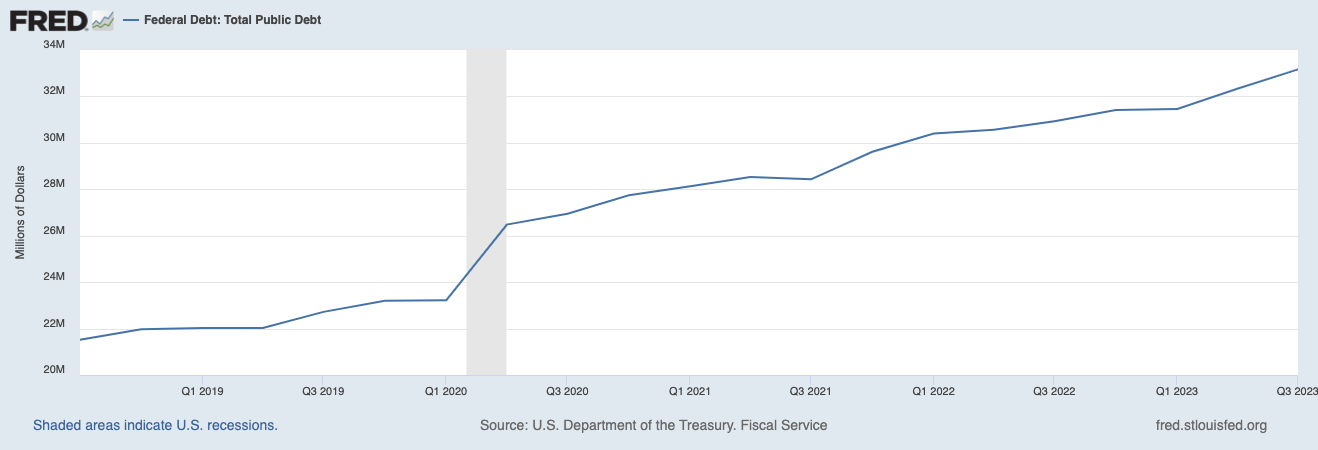

2) The U.S. is running emergency levels of social spending at a time when the economy is still growing. It’s added $5 trillion in debt since President Biden took office. And the pace of debt issuance is speeding up, not slowing down: the U.S. has added $2 trillion in debt in the last 12 months alone. You can thank Treasury Secretary Janet Yellen for signing off on this insanity.

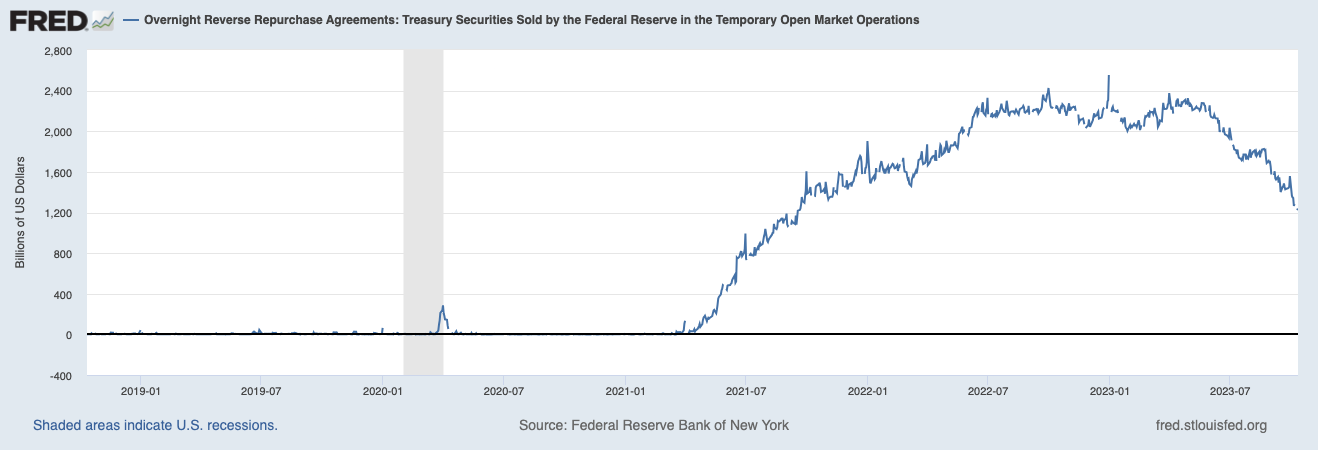

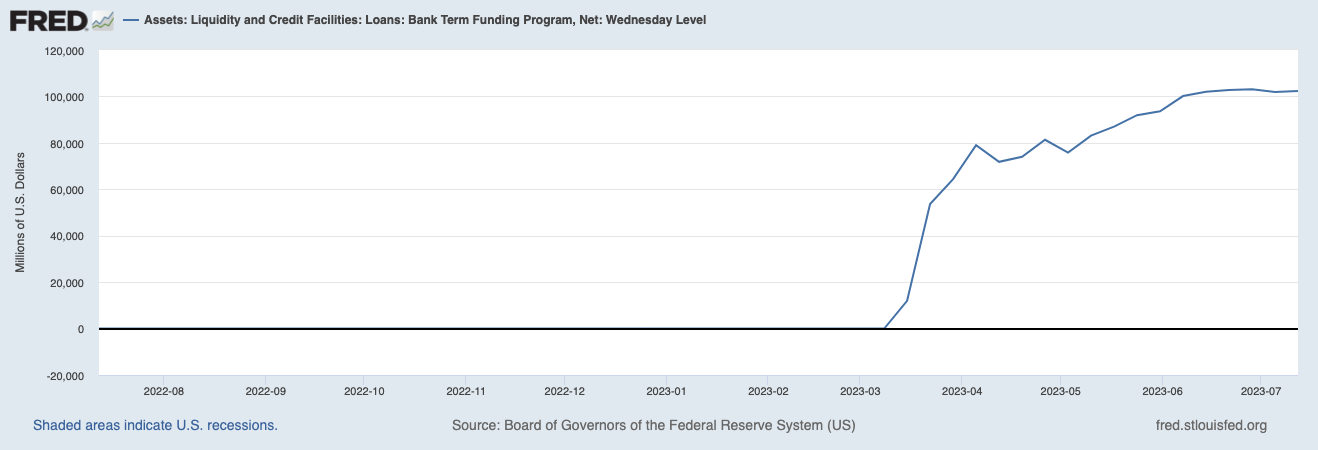

Today, I’d like to delve a bit more into one of the more nefarious schemes the Fed is using to juice stocks higher. To fully grasp this, we need to wind the clock back to March 2023, when the U.S. regional banking system was on the verge of collapse.

At that time, a number of large regional banks collapsed due to:

1) Bad risk management: their leadership teams failed to appropriately hedge their interest rate risk while the Fed was raising rates.

2) Banks were only paying 0.1% on deposits, while money market funds and short-term Treasuries were yielding 4% or more. As a result of this, depositors were pulling funds out of the banks, resulting in the banks having to sell large portions of their loan portfolios at a loss (banks must maintain certain capital requirements based on deposits).

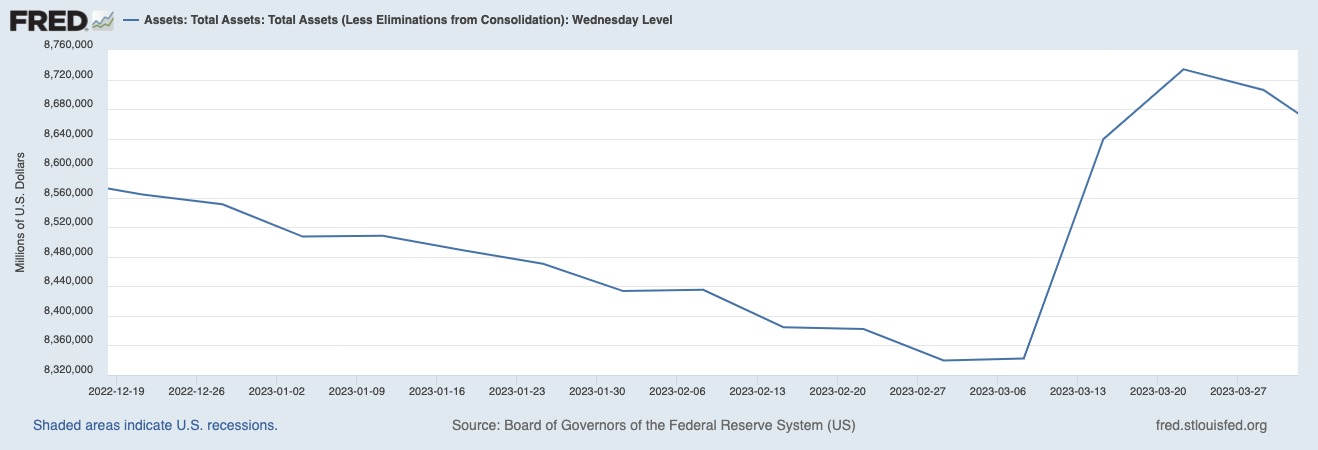

The Fed took action to stop a crisis from unfolding, pumping $400 billion in liquidity into the financial system in just three weeks. Prior to that, the Fed’s balance sheet was falling due to its Quantitative Tightening (QT) program. The Fed reversed NINE months worth of that program in just three weeks!

That staved off a crisis from hitting. But the Fed then began a back-door bailout of the banks through which it gave them additional access to credit and liquidity. And not just a little… but a LOT.

The below chart shows this facility’s use running back to 2005. And no, you’re not imagining things: the Fed’s use of this facility to juice the financial system in 2023 was greater than what it did during the pandemic, and almost as great as that used during the Great Financial Crisis of 2008! In fact, today it’s higher than it was during the absolute depth of the pandemic in March 2020!

We’re now almost a year out from the regional banking issues and the Fed continues using this facility to the tune of over $200 BILLION. So again, the Fed is juicing the financial system for political purposes. It’s abhorrent and corrupt, but it’s reality. And well prepared investors can take steps to insure they profit from what’s happening with the right investments.

I’ll address how to profit from this in tomorrow’s article. If you’d like it delivered to your inbox, all you have to do is join our FREE daily investment commentary GAINS PAINS & CAPITAL.

The Fed and the Treasury are juicing the markets to help the Biden administration with its 2024 re-election bid. And their actions are going to result in a massive crisis hitting some time in 2025.

The Fed is supposed to be politically independent, but everyone knows that is a fairytale. The Bernanke-led Fed introduced QE 3 a mere two months before the 2012 election to help the Obama administration. Moreover, former Fed Vice-Chair Stanley Fisher admitted that the Powell-led Fed intentionally raised rates in December 2018 (triggering a stock market crash) to hurt the economy under former President Trump.

Put simply, anyone who tells you that the Fed doesn’t play politics hasn’t been paying attention. And it is clear that today’s Fed led by Jerome Powell and today’s Treasury led by Janet Yellen are actively juicing the markets and economy to help the Biden administration with its claims that the economy is booming and everything is great.

Case in point, the Fed is talking about easing monetary conditions at a time when the stock market is at all-time highs and financial conditions are LOOSER than they were when the Fed first started raising rates! Why do this? To keep stocks higher for the election.

The Fed is not the only one in on this scheme.

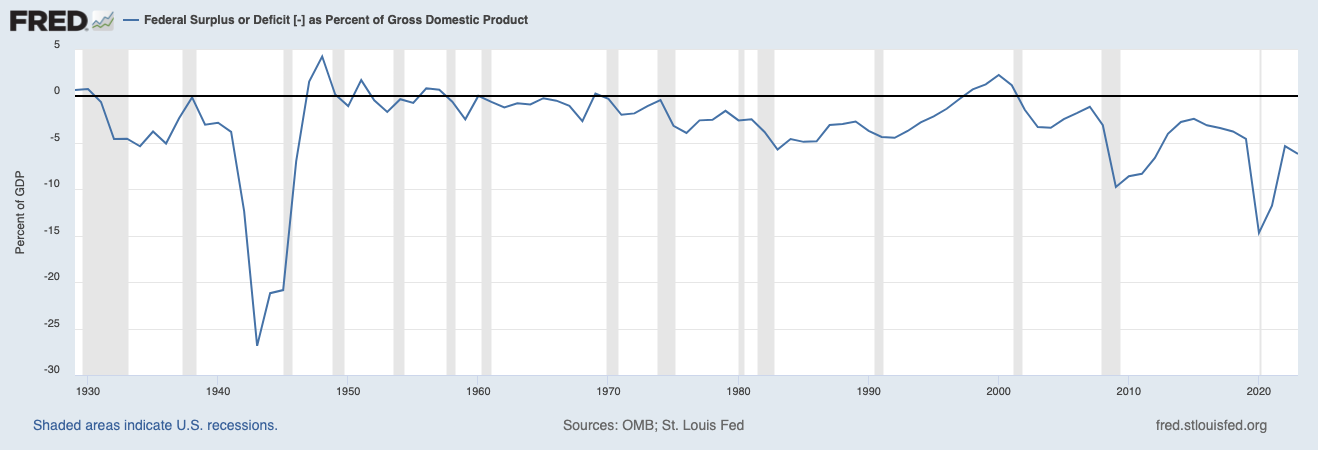

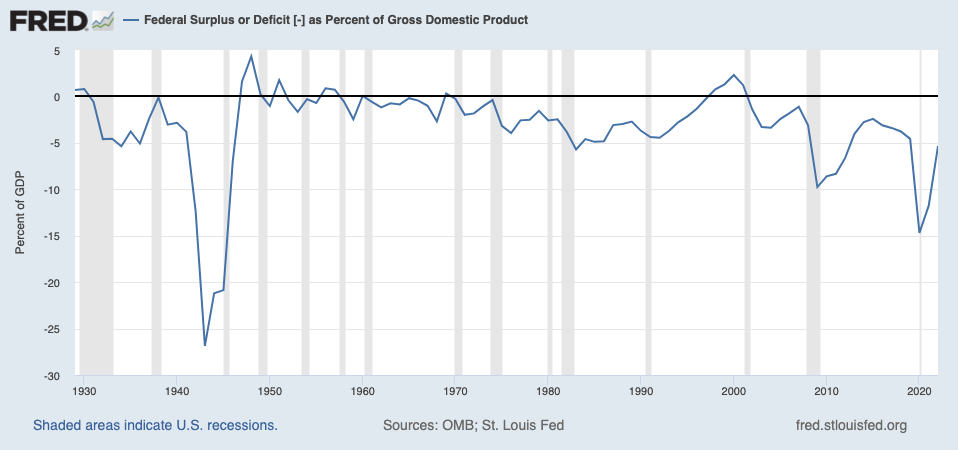

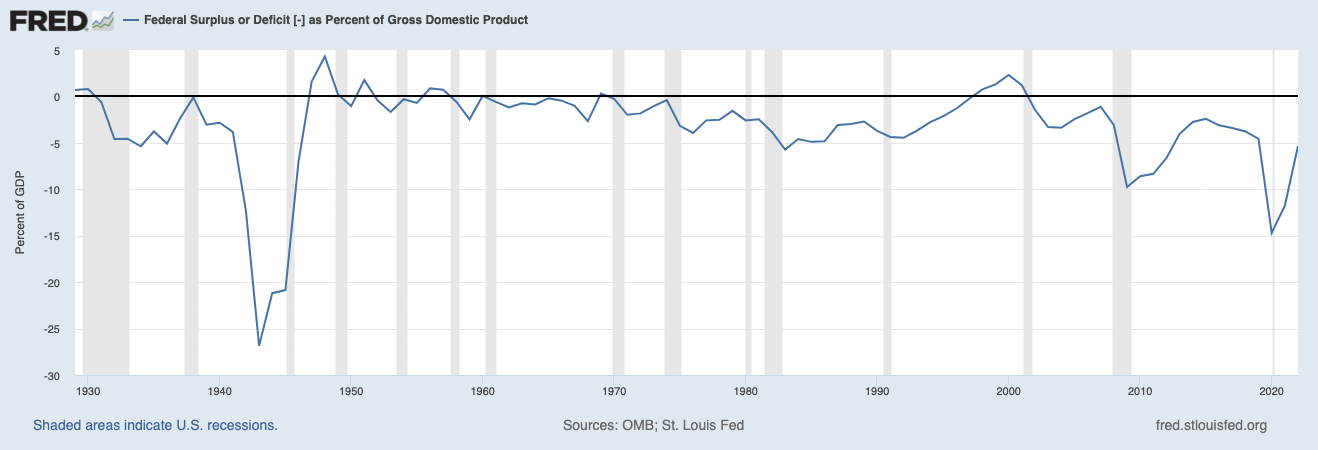

The Treasury is pulling out all the stops to help the Biden administration. Typically, the U.S. runs a massive deficit during recessions in order to cushion the economic contraction. Today the U.S. economy is technically still growing… and the Biden administration is running the U.S.’s largest deficit as as percentage of GDP in history (outside of World War II).

Put another way, the U.S. is running emergency levels of social spending at a time when the economy is still growing. And this is adding trillions of dollars in new debt to the U.S.’s liabilities every year.

The U.S. owed $28 trillion in debt when Joe Biden was sworn into office in 2021. It owes $33 trillion today. And the pace of debt issuance is speeding up, not slowing down: the U.S. has added $2 trillion in debt in the last 12 months alone. You can thank Treasury Secretary Janet Yellen for signing off on this insanity.

Worst of all, the above items are happening for political purposes. There are ZERO fundamental reasons for the Fed and the Treasury to be implementing the above policies. But in today’s world of political corruption and systemic abuse of power, it’s simply how things are.

I’ll address how to profit from this in tomorrow’s article. If you’d like it delivered to your inbox, all you have to do is join our FREE daily investment commentary GAINS PAINS & CAPITAL.

Who are you going to believe… the mainstream shills, or your own eyes and wallets?

The economic data in the US is telling us that the economy is booming. GDP growth is roaring at annualized rate of over 4%. Unemployment is collapsing, with over 300,000 new jobs being created last month. And inflation has been tackled, falling from a peak of nearly 9% to 3% where is sits today.

The mainstream media parrots these data points as if they were facts. There’s only one problem… if any of this were true, the Biden administration’s approval rating would not have just hit a new low of 37%. You can’t argue that the economy is doing great, but the President is doing an awful job at the same time. So one of these items (the economic data or the President’s approval ratings) is false.

It’s not the approval ratings.

The economic data in the U.S., particularly any economic data that is politically important (GDP growth, inflation, employment) is now largely fiction. And I don’t mean “fiction” as in there are honest mistakes being made because things are complicated; I mean fiction as in the bulk of the data is invented in a spreadsheet by a government beancounter.

Case in point, we are told that in January the economy added 353,000 jobs. As ZeroHedge notes this happened in a month in which the economy actually LOST 63,000 full time jobs and gained 96,000 part-time jobs. Yes, somehow the economy “created” 353,000 jobs while losing 96,000 full time jobs.

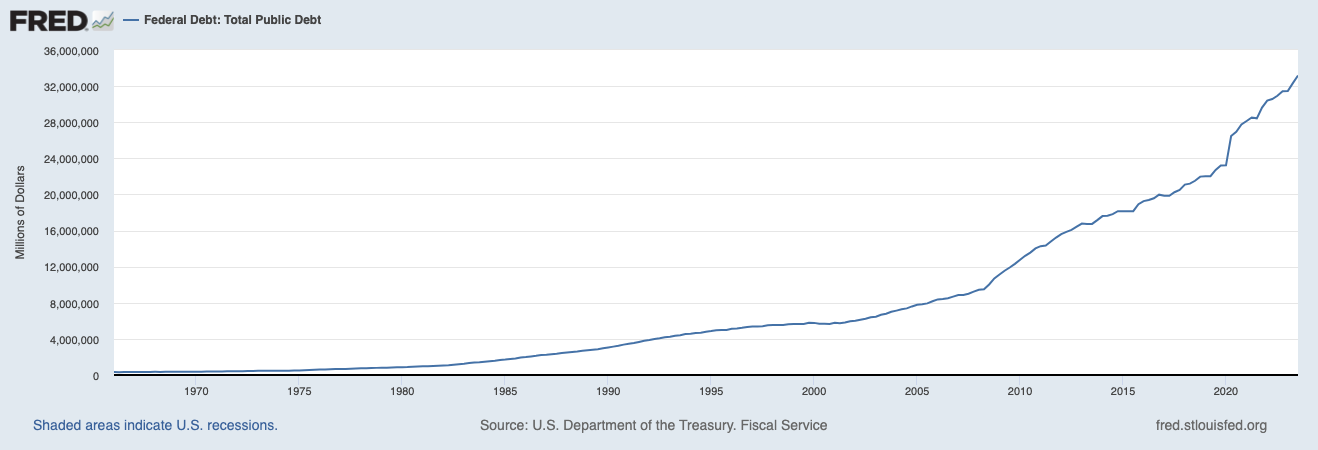

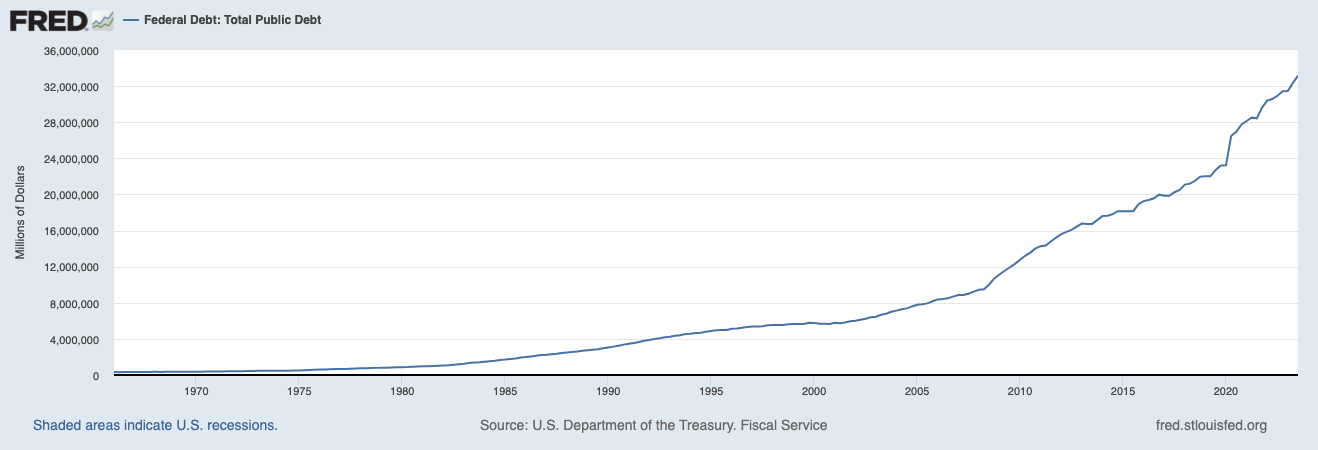

Some added food for thought about the true state of the economy. As I write this, the U.S. is adding over $2 trillion in debt every year. The below chart needs no explanation. This is obviously NOT going to end well.

Why is the U.S. adding so much debt?

Because the Biden administration is running the largest deficit as a percentage of GDP outside of WWII. Yes, the deficit is larger today than it’s been during any recession in the last 100 years. Surely this must be because the economy is roaring!

If all of the above items make your head hurt, consider the added insanity that financial institutions and fund managers actually invest trillions of dollars based on this stuff. And people wonder why no one ever sees a crisis coming in advance!?!?

Don’t fall for this stuff. There’s a lot of money to be made in the markets based on these lies, but it takes a lot of work and insight!

To start receiving our daily market insights every weekday before the market’s open (9:30AM EST), use the link below. There is no fee or cost to GAINS PAINS & CAPITAL. Access is free to the public.

Having juiced the markets higher with the promises of rates cuts, the Fed now finds itself in the absurd position of walking back these promises as A) stocks are at all time highs, B) the BLS continues to release manipulated jobs data to aid the Biden administration and C) the economy is allegedly growing at annualized rate of 4%+.

Regarding the jobs data…

It has become a running joke that the beancounters in Washington DC release absurdly positive economic data to aid the Biden administration, only to revise the data downward multiple times after the fact. Perhaps the single most ridiculous example of this occurred in 2022 when the Philadelphia Fed revealed that the BLS had overstated job growth in first half of the year by one million jobs.

I bring this up because the BLS was up to its usual shenanigans with the January jobs report released on Friday. In it the BLS claimed that the economy added 353,000 jobs in January 2024 instead of the expected 185,000. Let’s be blunt here, if the economy was even close to as strong as the gimmicked data the BLS issues, the Biden administration’s approval ratings wouldn’t be in the toilet.

Politics aside, the issue with this jobs report is that it makes it impossible for the Fed to cut rates any time soon. After all, how can the Fed start easing monetary conditions when the economy is supposedly adding over 300,000 jobs per month and GDP is supposedly growing at 4.2%?!

And so the markets are in a kind of limbo. Everyone is bullish based on hopes of Fed rate cuts… but the Fed can’t cut rates with the data this strong. This opens the door to a market correction to take some of the “froth” out of stocks.

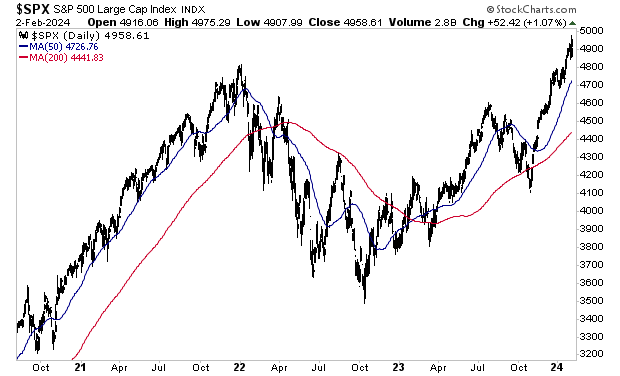

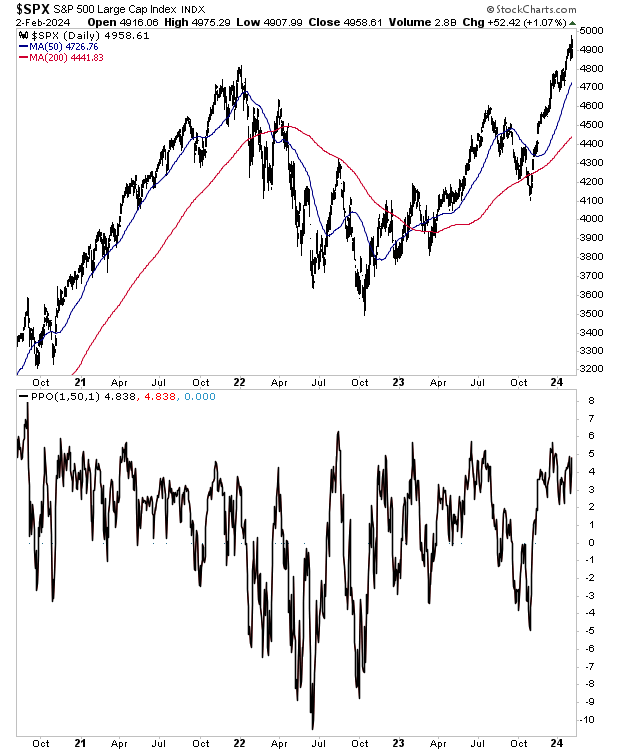

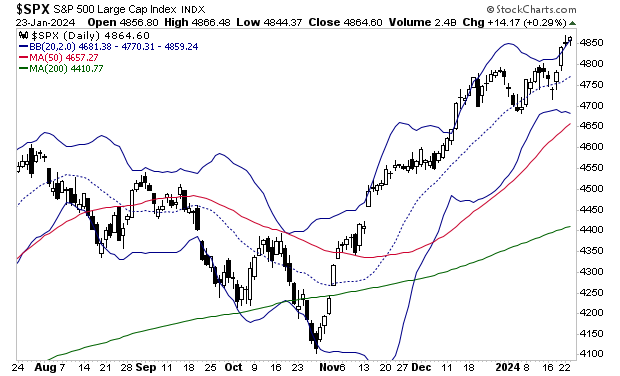

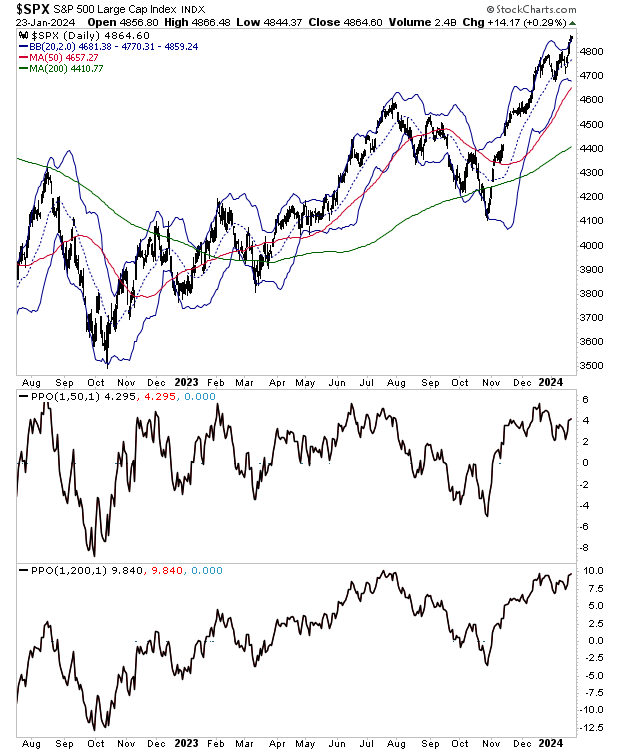

The S&P 500 hasn’t touched its 50-day moving average (DMA) in three months. The 50-DMA is represented by the blue line in the chart below. As you can see, it’s unusual for the S&P 500 NOT to touch this line for such a long period of time.

I would also add that the S&P 500 is ~5% above the 50-DMA. Historically, this degree of extension has market a top of sorts.

With all of this in mind, the odds favor a correction to the 50-DMA (upper 4700s) some time in the next few weeks. After that, we’ll revisit our market forecast to see what’s next.

As I keep stating, you CAN outperform the overall market, but it takes a lot of work and insight!

To start receiving our daily market insights every weekday before the market’s open (9:30AM EST), use the link below. There is no fee or cost to GAINS PAINS & CAPITAL. Access is free to the public.

The most critical companies to monitor are the MAG 7/ big tech plays. These are the largest companies in the S&P 500. Because of their size, they account for ~30% of the index’s weight.

Thus far, Tesla (TSLA), Microsoft (MSFT), and Alphabet (GOOGL) have reported. The results have been interesting.

TSLA reported on 1/24/24. The stock was down 10% on its results.

Last night, MSFT and GOOGL reported. MSFT is down about 0.5% while GOOGL is down over 5%.

So, thus far two of the three MAG 7 have seen their stocks collapse a LOT on earnings results while one of is effectively flat.

This doesn’t bode well for the broader market. It is VERY difficult for the S&P 500 to rally much at all if the MAG 7 plays are weak. Remember, these companies account for 30% of the market’s weight.

Apple (AAPL), Amazon (AMZN) and Meta (META) report on Thursday. Nvidia (NVDA) reports on 2/21/24. If AAPL and META also sell-off on their results, it’s safe to assume the market will experience a decent correction.

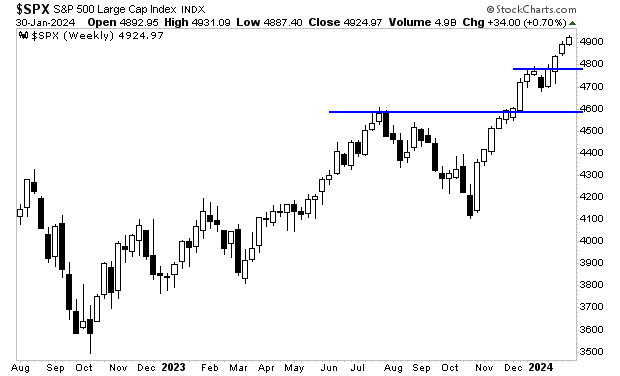

From a technical analysis perspective, the S&P 500 has support just below 4,800. After that is CRITICAL support at 4,595. Given how the MAG 7 plays are responding to earnings, I wouldn’t be surprised to see a correction to 4,595 in the next two months.

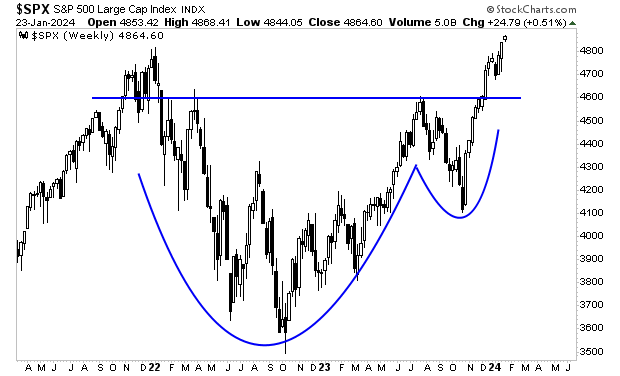

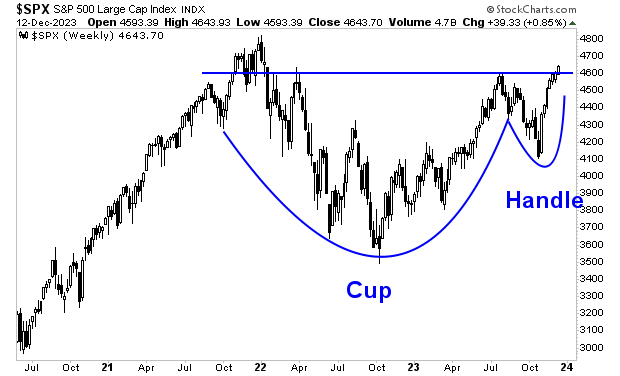

This would represent a back-test of the Cup and Handle formation I showed yesterday. Bear in mind, a correction like this would NOT negate our longer term forecast for the S&P 500 to go to 6,000 before 2025. Rather, this correction is a short-term development and would present a fantastic buying opportunity.

If you’re looking for someone to guide your investing to insure you crush the market, you can sign up for our FREE daily market commentary, GAINS PAINS & CAPITAL.

As an added bonus, I’ll throw in a special report Billionaire’s “Green Gold” concerning a unique “off the radar” investment that could EXPLODE higher in the coming months. It details the actions of a family of billionaires who literally made their fortunes investing in inflationary assets. And they just became involved in a mid-cap company that has the potential to TRIPLE in value in the coming months.

The S&P 500 is up nearly 150 points in just five sessions. This has been quite a move. And what’s truly extraordinary is that every intraday dip is being bought aggressively.

However, a word of caution here.

The S&P 500 is now 4% above its 50-Day Moving Average (DMA) and 9.8% above its 200-DMA. Over these last 18 months, any time the index has become this extended above its trend has resulted in a short term peak. So, it wouldn’t be surprising to see the S&P 500 correct down to back-test the recent breakout at 4,790.

After that, the door is open to 5,000 on the S&P 500. The Cup and Handle formation I outlined a few weeks ago has broken to the upside. Long-term (later in 2024) we are likely going MUCH higher.

For more market insights swing by https://gainspainscapital.com/

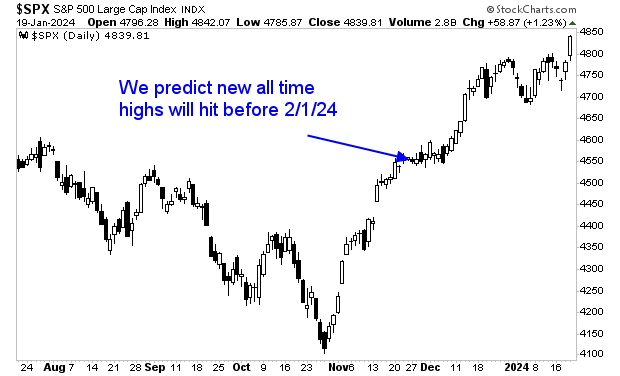

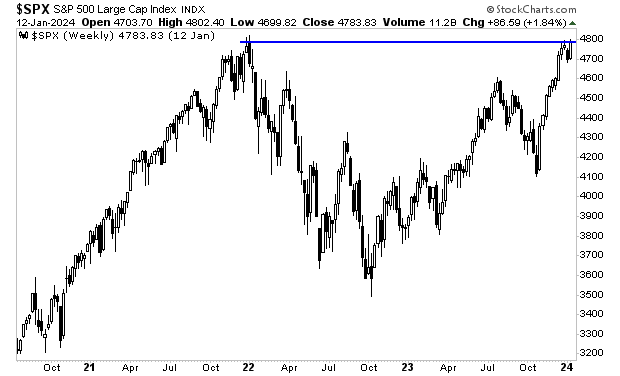

On November 28th, 2023, I predicted that stocks would hit new all-time highs before February 1, 2024.

Bear in mind, the S&P 500 was at 4,550 when I wrote this. So my prediction meant that the index would have to rally to over 4,818 (the former all-time high established January 3, 2022) in eight weeks’ time.

On Friday this happened, a full two weeks ahead of schedule. Anyone who followed our prediction made a killing!

So what happens now?

Stocks are now quite stretched to the upside. I anticipate we’ll see a drop to backtest this recent breakout at 4,800 sometime in the next 10 days. But after that, the door is open to a run to 4,920 by the end of 1Q24. That’s the upside target for the inverse Head and Shoulders pattern the S&P 500 has established in the last four weeks.

So, in the last seven months, we’ve predicted:

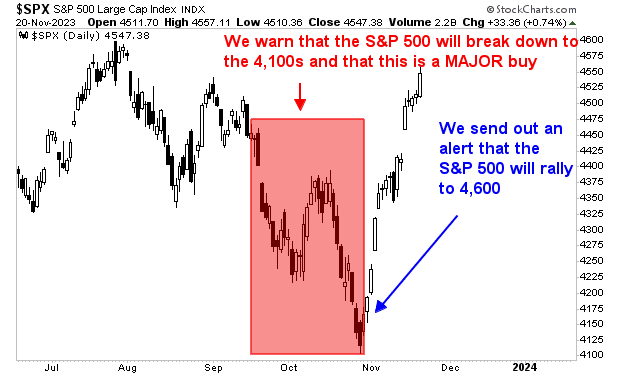

1) The S&P 500 to decline to 4,100s (when it was at 4,500).

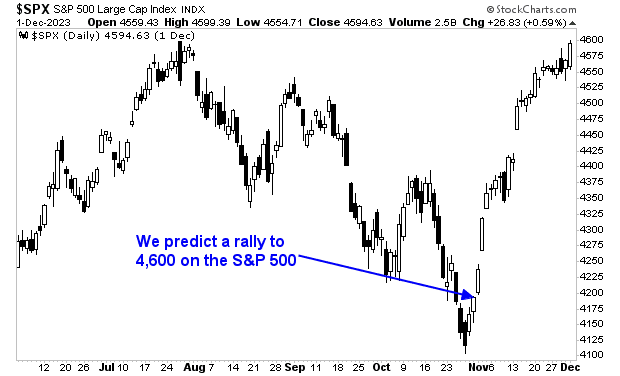

2) The S&P 500 to rally from the 4,100s to 4,600 (when it was at 4,200).

3) The S&P 500 to hit new all-time highs before February 1st 2024(when it was at 4,550).

As I keep stating, you CAN outperform the overall market, but it takes a lot of work and insight!

If you’re looking for someone to guide your investing to insure you crush the market, you can sign up for our FREE daily market commentary, GAINS PAINS & CAPITAL.

As an added bonus, I’ll throw in a special report Billionaire’s “Green Gold” concerning a unique “off the radar” investment that could EXPLODE higher in the coming months. It details the actions of a family of billionaires who literally made their fortunes investing in inflationary assets. And they just became involved in a mid-cap company that has the potential to TRIPLE in value in the coming months.

On December 20th 2023, I predicted that stocks would hit new all-time highs before February 2024. Despite all the drama in Washington as well as the geopolitical risk in the world, stocks are within spitting distance of doing this… and we’re only halfway through January.

The S&P 500 bounced hard off of support at 4,700. If the index closes this week even marginally higher, it will be at new all-time highs.

This is not our first accurate prediction for stocks.

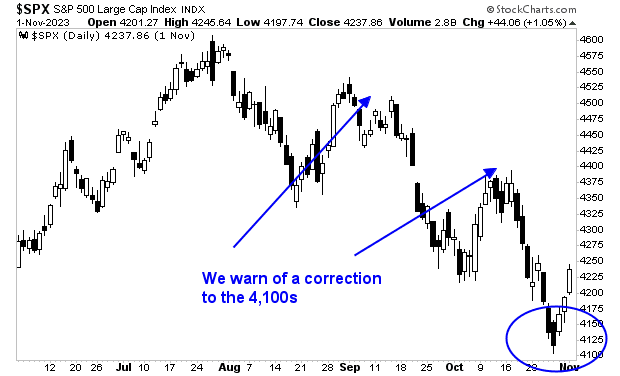

Throughout September and October of 2023, we warned clients that the S&P 500 was due for a pull back down to the 4,100s. Time and again, we warned our readers not to buy into the rally and to preserve their capital for an incredible buying opportunity that would soon hit.

And hit it did! And our readers “backed up the truck.”

Then, on November 2, when the S&P 500 was still at 4,200, we told clients to buy aggressively because the S&P 500 was going to 4,600 before year end. Remember, the S&P 500 had only just bottomed at 4,100 and we were predicting a 400 point move to hit in the span of eight weeks. So this was an EXTREMELY aggressive forecast. But our research backed it up and we trust our work!

The market then rallied to 4,600 in just four weeks! Those clients who followed our recommendation and loaded up on stocks at 4,100 made an absolute killing!

So, in the last seven months, we’ve predicted:

1) The S&P 500 to decline to 4,100s (when it was at 4,500).

2) The S&P 500 to rally from the 4,100s to 4,600 (when it was at 4,200).

3) The S&P 500 to hit new all-time highs before February (when it was at 4,600).

As I keep stating, you CAN outperform the overall market, but it takes a lot of work and insight!

If you’re looking for someone to guide your investing to insure you crush the market, you can sign up for our FREE daily market commentary, GAINS PAINS & CAPITAL.

As an added bonus, I’ll throw in a special report Billionaire’s “Green Gold” concerning a unique “off the radar” investment that could EXPLODE higher in the coming months. It details the actions of a family of billionaires who literally made their fortunes investing in inflationary assets. And they just became involved in a mid-cap company that has the potential to TRIPLE in value in the coming months.

Governments around the world are issuing staggering amounts of debt to “paper over” any weakness in the private sector with public spending. As Bloomberg notes, collectively, the U.S., U.K., E.U., and Japan will issue $2 trillion in new debt this year.

This is keeping the world from entering a recession, while simultaneously setting the stage for the next round of inflation. Remember that the first wave of inflation (2021-2023) was triggering by egregious levels of public spending/ stimulus during a time of private sector weakness.

In the U.S., it is clear the Biden administration is implementing policies to prop up the economy and financial markets for the 2024 election regardless of the consequences the policies will bring down the road.

Case in point, the U.S. is running the levels of deficit you usually see during a recession, at a time when the economy is technically still growing. Indeed, the only periods in which the U.S. was running a larger deficit as a percentage of GDP in the last 100 years during World War II, and the Great Financial Crisis.

As you likely know, deficits are financed via the issuance of debt. And because the U.S. is constantly having to roll over old debt into new debt while also issuing new debt to finance its deficit, the country has added some $2 TRILLION in debt in the last seven months alone!

My question to policymakers: what if all this spending brings back higher inflation when the U.S. finally rolls over into recession? What’s the plan, then?

Gold has figured it out already. Other asset classes will soon, too.

If you’re looking for someone to guide your investing to insure you crush the market, you can sign up for our FREE daily market commentary, GAINS PAINS & CAPITAL.

As an added bonus, I’ll throw in a special report Billionaire’s “Green Gold” concerning a unique “off the radar” investment that could EXPLODE higher in the coming months. It details the actions of a family of billionaires who literally made their fortunes investing in inflationary assets. And they just became involved in a mid-cap company that has the potential to TRIPLE in value in the coming months.

The U.S. passed a debt ceiling resolution in May of 2023. Both the GOP and the Democrats claimed victory for the deal, but the reality is the government won and Americans were screwed.

How do I know this?

It took the U.S. 232 years to generate its first $10 trillion in debt. It added another $10 trillion in debt in just nine years once the Fed pinned interest rates at zero and cornered the bond market with Quantitative Easing (QE) from 2008 to 2017.

The U.S. then added another $10 Trillion in debt in just five years when the Fed reintroduced ZIRP and QE in NUCLEAR fashion in response to the pandemic. Obviously, you’re beginning to see the trend here: the U.S. added $10 trillion in debt in 232 years, nine years, and five years.

But the “debt deal” has really added fuel to the fire.

The U.S. has added another $4 trillion in debt since 2022. But~ $2 trillion of this was added in the seven months since the debt deal was passed! And thanks to the debt deal removing the debt ceiling until 2025, there is little chance that the pace of debt issuance will slow anytime this year.

How will this end? With a debt crisis of some sort. The details, for now, are unclear.

What isn’t unclear is that investors can potentially make a LOT of money from this situation. Those who invested in the right assets at the right times during the last 20 years while the U.S. has engaged in a debt bonanza have seen some truly OBSCENE returns.

And no, I’m not talking about gold. The precious metal has traded sideways for four years, while the U.S. has tacked on another $10 trillion in debt.

If you’re looking for someone to guide your investing to insure you crush the market, you can sign up for our FREE daily market commentary, GAINS PAINS & CAPITAL.

As an added bonus, I’ll throw in a special report Billionaire’s “Green Gold” concerning a unique “off the radar” investment that could EXPLODE higher in the coming months. It details the actions of a family of billionaires who literally made their fortunes investing in inflationary assets. And they just became involved in a mid-cap company that has the potential to TRIPLE in value in the coming months.

Since early 2023, numerous pundits and gurus have been calling for a recession. And despite numerous indicators flashing that one is coming… the recession has yet to arrive.

Why?

This:

The U.S. is running a GARGANTUAN deficit equal to 5.5% of GDP.

To put this into perspective, it’s larger than the deficit the U.S. ran during EVERY recession in the last 100 years except for the Great Financial Crisis and when the economy was shutdown in 2020.

Put simply, the U.S. is running the kind of spending that we usually see during periods in which the private sector is in a total free-fall… at a time when the private sector is weak, but not yet collapsing.

This has managed to keep the economy positive. But it’s a short-term fix.

Ultimately, the U.S. cannot stay out of recession forever as no amount of government spending can replace the economic impact of the private sector (we learned this during the shutdowns when the Fed and Uncle Sam spent $8 trillion in 12 months but the economy still collapsed).

Moreover… this situation presents us with a MAJOR problem down the road: if the U.S. is already spending at a pace usually associated with recessions while the economy is still growing, what is going to happen when the economy finally does roll over into recession? How much spending will it be doing then? 8% of GDOP? 10% of GDP? More?

And bear in mind, this spending is being funded by debt (it is a deficit after all). What happens to the bond market if the U.S. cranks up its spending to 8% or more of GDP when the actual recession hits?

Gold has started to figure it out. Other assets will figure it out soon.

As I keep stating, you CAN outperform the overall market, but it takes a lot of work and insight!

If you’re looking for someone to guide your investing to insure you crush the market, you can sign up for our FREE daily market commentary, GAINS PAINS & CAPITAL.

As an added bonus, I’ll throw in a special report Billionaire’s “Green Gold” concerning a unique “off the radar” investment that could EXPLODE higher in the coming months. It details the actions of a family of billionaires who literally made their fortunes investing in inflationary assets. And they just became involved in a mid-cap company that has the potential to TRIPLE in value in the coming months.

As I keep telling you, it IS possible to time the market. The key is to put in the work to do so.

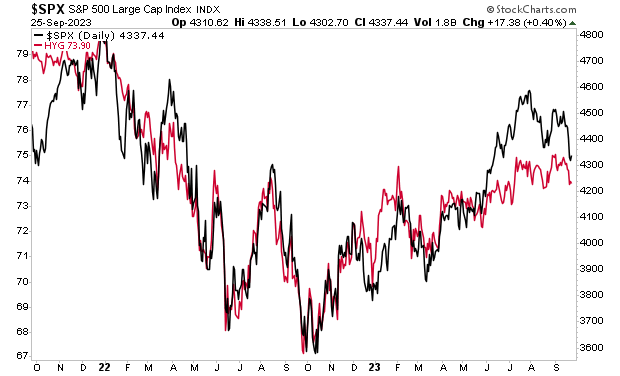

For me, one of the best means of predicting stock market moves is to focus on “market leading” indicators, or assets that typically lead stocks to the upside and the downside during market turns.

One of my favorite such indicators is high yield credit, or junk bonds.

Bonds/ credit are senior to stockholders. If a company goes bust and needs to liquidate its assets, bond/ credit holders will be paid out long before stockholders see a dime. And generally speaking, bond investing is more sophisticated than stock investing largely due to bonds’ greater sensitivity to Fed policy, the economy, and more.

As a result of this, credit, particularly high yield credit, or credit for companies that are at a greater risk of going bust, typically leads stocks when it comes to pricing future risk on or risk off moves.

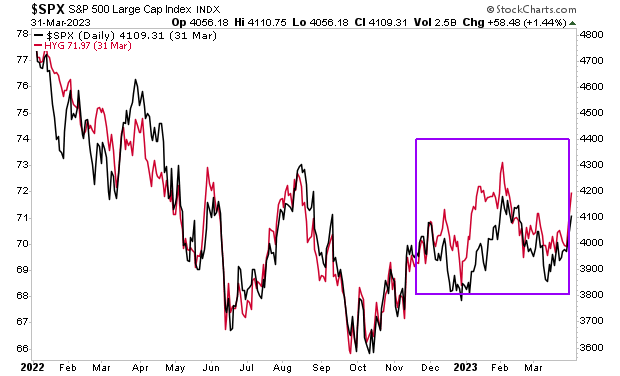

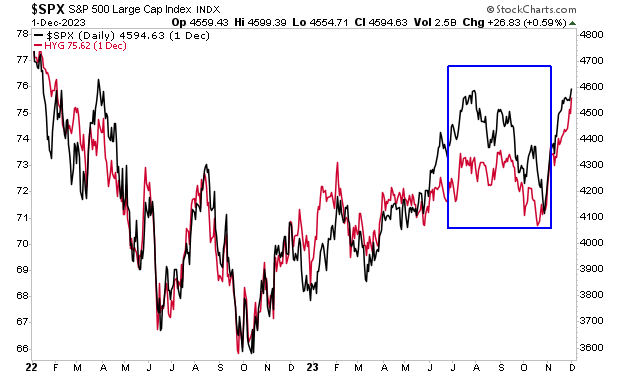

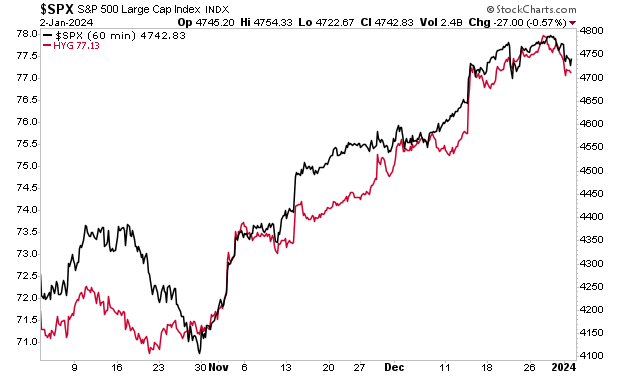

You can see this clearly in the following charts which depict the High Yield Corporate Bond ETF (red line) and the S&P 500 (black line). Sometimes the two assets move in tandem, but other times, credit leads stocks clearly to the point that you can accurately predict the next market move for stocks.

The first chart concerns the risk on move in assets that occurred from late 2022/ early 2023. At that time, HYG lead the market to the upside, rallying aggressively even when stocks would dip for a day or two. I’ve illustrated this with a purple rectangle below. Throughout that time period, the ongoing strength in HYG was a reliable indicator that the stock market would continue to rally.

Another example concerns the risk off move in assets that occurred from July 2023 through November 2023. During that period, high yield credit failed to confirm any rally in stocks, with the red line (credit) rolling over quickly even when the black line (stocks) bounced aggressively. I’ve illustrated this with a blue rectangle in the chart below.

So, what is high yield credit telling us about the future of the stock market today?

HYG is leading stocks to the downside, though it is doing so in a very controlled manner. Right now, HYG is suggesting that the S&P 500 will drop to 4,700 or so. Obviously this can change as things develop, but for now, HYG is telling us that any stock pullback should be relatively shallow.

As I keep stating, you CAN outperform the overall market, but it takes a lot of work and insight!

If you’re looking for someone to guide your investing to insure you crush the market, you can sign up for our FREE daily market commentary, GAINS PAINS & CAPITAL.

As an added bonus, I’ll throw in a special report Billionaire’s “Green Gold” concerning a unique “off the radar” investment that could EXPLODE higher in the coming months. It details the actions of a family of billionaires who literally made their fortunes investing in inflationary assets. And they just became involved in a mid-cap company that has the potential to TRIPLE in value in the coming months.

The S&P 500 is ~5% above its 50-Day Moving Average. Historically, this degree of extension above the primary trend has marked a temporary top. It doesn’t mean that stocks will collapse, rather is suggests the upside is limited and consolidation/ correction is the high probability scenario.

The question now is how deep the correction will be…

For that analysis we turn to bonds and the Fed.

The yield on the 2-Year U.S. Treasury has declined from 5.25% to 4.2% where it is now. This decline has been driven by the Fed pivot, in that the Fed will no longer be raising rates, but instead will begin cutting them in the near future.

This will be a boon for stocks as this declining yield means:

1) Stocks will be priced at a higher future Earnings Per Share (EPS) multiple.

2) Money will begin to flow out of bonds and money market accounts into stocks as yields have peaked.

All of the above suggests that any and all dips in stocks will be relatively shallow. Put simply the coming decline is an opportunity to “buy the dip” in a new bull market.

In terms of specific price points, the S&P 500 has major support at 4,700. I would be very surprised to see the market drop much below that level. The S&P 500 might decline into the upper 4,600s to “run the stops” for stock bulls, but a drop below 4,680 is unlikely.

For more market insights and analysis, join our free daily market commentary Gains Pains & Capital. You’ll immediately start receiving our Chief Market Strategist Graham Summers, MBA’s briefings to your inbox every morning before the market’s open.

And if you sign up today, you’ll also receive a special investment report How to Time a Market Bottomthat the market set-up that has caught the bottoms after the Tech Crash, Housing Bust, and even the 2020 pandemic lows.

Even more importantly, you’ll find out what this trigger says about the market today!

This report usually costs $249, but if you join Gains Pains & Capital today, you’ll receive your copy for FREE.

On Monday I told you that the S&P 500 was headed for 4,700. At that time, the market was hovering around 4,600. And given all the risks in the world (turmoil in the Middle East, slowing economic data in the U.S.), I’m sure many people thought I was bonkers to predict that stocks would continue higher.

Fast forward 48 hours and it looks as if the S&P 500 will hit my target before the week ends. As I write this, the S&P 500 futures are at 4,656.

The gains won’t stop there either. I believe the market will reach new all-time highs before February 1 2024. The former high was 4,818 set in October of 2022. I believe we’ll break that within six weeks’ time.

The long-term chart is clear… I’ll tell you what it portends tomorrow. But for now, here’s a hint.

As I keep stating, you CAN outperform the overall market, but it takes a lot of work and insight!

If you’re looking for someone to guide your investing to insure you crush the market, I’m your guy. Since 2015, subscribers of my Private Wealth Advisory have maintained a win rate of 74%.

Yes, we made money on three out of every four trades we closed.

Throughout this time, we completely OBLITERATED the S&P 500, returning over 200% compared the market’s 125%.

So you are looking for someone to help you profit from the markets… few analysts have the ability to navigate volatile markets like I do.

And I believe 2023 is going to be our best year yet!

To join us in turning the coming roller coaster into a source of life-changing profits, all you NEED to do is take out a 30-day $3.99 trial subscription to Private Wealth Advisory.

A full SIX (6) MONTH subscription to Private Wealth Advisory includes:

Frankly, this is a ridiculous amount of material to offer for just $3.99…

Heck, the book alone is worth $9.99, and you’re getting FREE shipping on it!

So technically, you’re getting the weekly market updates, the weekly podcast, and the trades and trade alerts FREE OF CHARGE.

The doors close on this offer soon… don’t delay taking advantage of it!

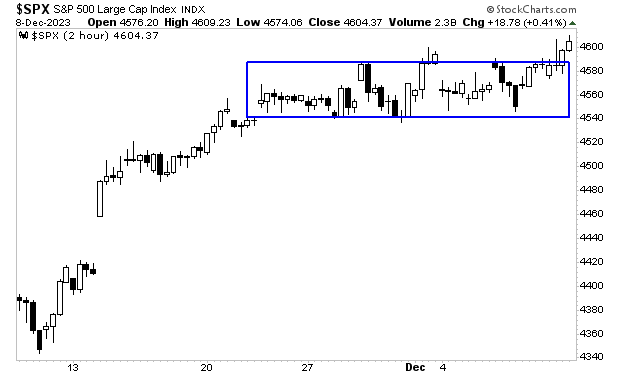

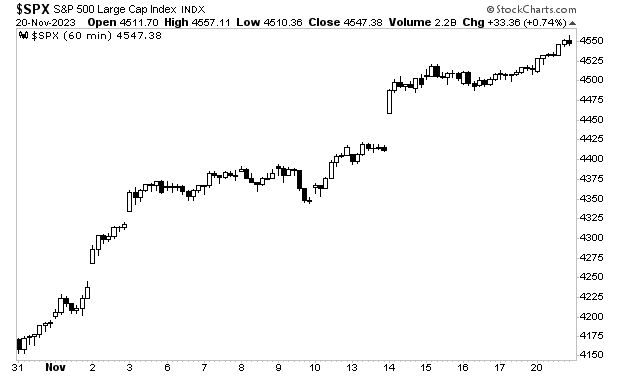

The S&P 500 has been trading in a 40-point range since mid-November. I know that sounds difficult to believe, but it’s true. For all the issues in the world (conflict in the Middle East, the ongoing war between Russia and Ukraine, economic data weakening in the U.S., political issues/ potential impeachment for the Biden administration), the stock market has gone nowhere.

See for yourself. I’ve illustrated this with a blue rectangle in the chart below.

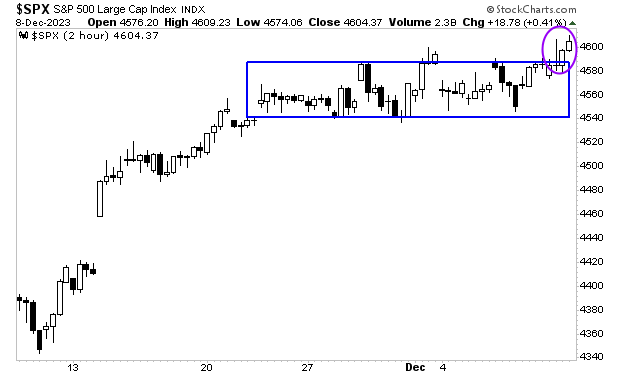

Having said that, the market DID reveal something MAJOR in the last month… but it’s what DIDN’T happen as opposed to what happened.

What didn’t happen?

Stocks didn’t break down.

In spite of all the issues and potential risks in the world right now, the bears couldn’t generate enough selling pressure to push stocks down more than 1%. And considering the market was EXTREMELY overbought going into this period, it REALLY suggests the bears are weak right now.

Which means…

The Santa rally is about to hit. Indeed, just last week, the market managed to break out of its trading range and stay there. I’ve illustrated this development with a purple circle in the chart below.

If stocks hold this today, then the door opens to a Santa rally that sees the S&P 500 hit 4,700 before year-end. Take out 4,600 on a weekly basis and you’ve got an opening to 100 points higher relatively quickly.

For more market insights and analysis, join our free daily market commentary Gains Pains & Capital. You’ll immediately start receiving our Chief Market Strategist Graham Summers, MBA’s briefings to your inbox every morning before the market’s open.

And if you sign up today, you’ll also receive a special investment report How to Time a Market Bottomthat the market set-up that has caught the bottoms after the Tech Crash, Housing Bust, and even the 2020 pandemic lows.Even more importantly, you’ll find out what this trigger says about the market today!This report usually costs $249, but if you join Gains Pains & Capital today, you’ll receive your copy for FREE. To do so…

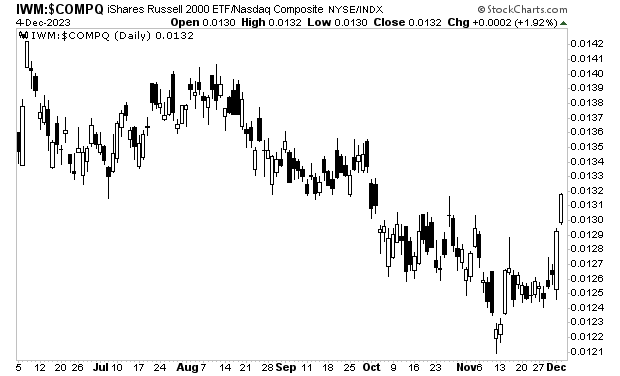

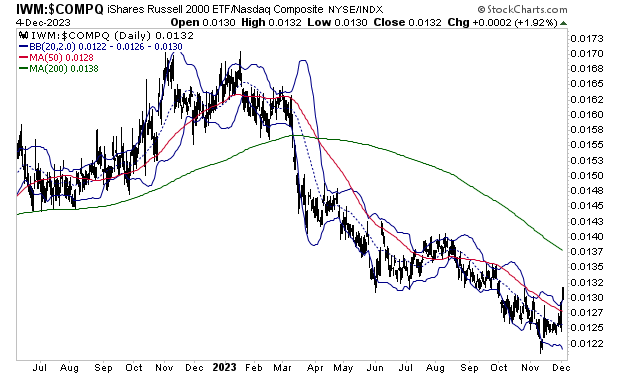

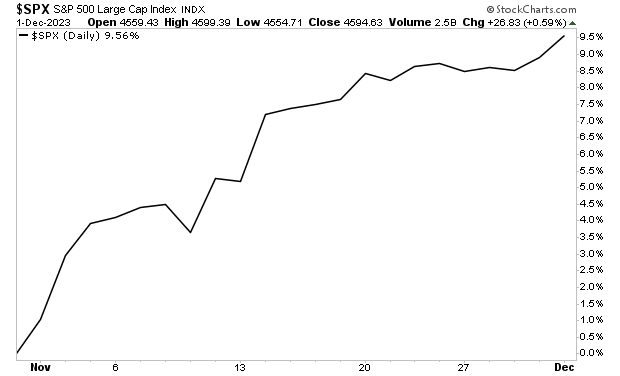

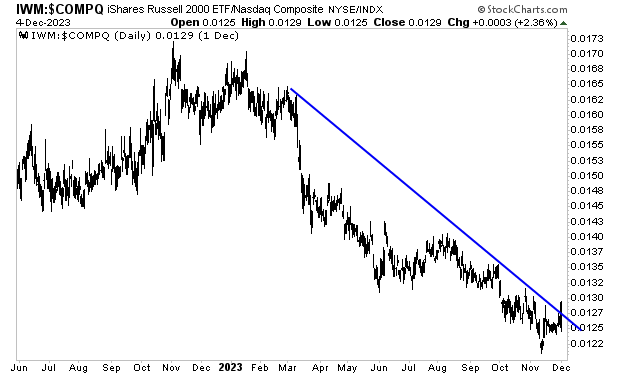

Yesterday’s market action could not have illustrated the current market rotation any better.

As I recently outlined:

1) The S&P 500 is currently consolidating after one of its best monthly performances in 30 years.

2) This consolidation has consisted of large tech correcting while laggard sectors and indices (small caps/ the Russell 2000, industrials/ the Dow Jones Industrial Average) catch a bid.

Yesterday’s price action illustrated this perfectly: microcaps (the Russell 2000) caught a major bid relative to tech (the NASDAQ) as the Russell 2000 ROSE over 1% while the NASDAQ fell nearly 0.9%.

If you heeded yesterday’s missive you did quite well! Again, you CAN outperform the overall market, but it takes a lot of work and insight!

This trend is likely to play out over the next two weeks until the Russell 2000/ NASDAQ ratio reaches its 200-day moving average (DMA) sometime around the Fed’s next FOMC (December 12th-13th).

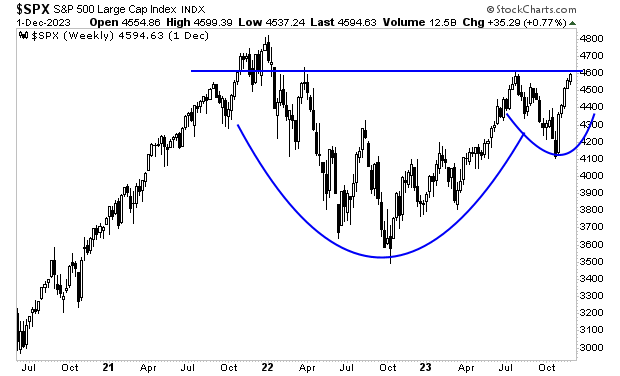

At that point the overall market should complete its consolidation/ correction and begin its next leg up. I’ve said previously that the S&P 500 will hit 5,000 sometime in the 1Q24. The setup is clear in the longer-term Cup and Handle formation.

For more market insights and analysis, join our free daily market commentary Gains Pains & Capital. You’ll immediately start receiving our Chief Market Strategist Graham Summers, MBA’s briefings to your inbox every morning before the market’s open.