The following is an excerpt from my latest issue of Private Wealth Advisory. In it I outline the brutal reality about Spain’s “bailout”= the money currently doesn’t exist and it’s unlikely Spain will ever get it any time soon… if ever. To learn more about Private Wealth Advisory and how we help our clients profit from the “unquantifiable” opportunities in the markets… Click Here Now!!!

Spain has supposedly been “saved” by a €100 billion bailout.

However, the details surrounding the source of the funding for this “bailout” still remain a mystery as there is no entity capable of providing the €100 billion in capital: neither the IMF, nor the Federal Reserve, nor the ECB have the political backing to launch a bailout of this size… and of the two EU mega-bailout funds, the EFSF and the ESM, the former can’t even raise €10 billion successfully while the latter doesn’t even exist yet.

Indeed, EU leaders have already pushed back the deadline for the creation of the ESM from July 1st to July 9th. And even if they do manage to hit the July 9th deadline (unlikely given that no EU political decision has made its deadline since the Crisis began) both Germany and Finland have stated that they are against the ESM buying sovereign bonds without “conditions.”

As we’ve already seen with Greece, those on the receiving end of the bailout gravy train are not prone to meeting “conditions.” Spain is no different: not only has it missed its budget deficit requirements several times but it is now openly ignoring demands from those propping it up:

Spain PM not to implement IMF suggestions for now

Spain will not immediately implement the International Monetary Fund’s latest recommendations, which include cutting government workers’ wages further, because they are nonbinding advice, the prime minister said Saturday.

The IMF is one of three organizations Mariano Rajoy’s government turned to for an assessment of the state of Spain’s banking sector ahead of a (EURO)100 billion ($125 billion) bailout for failing lenders.

http://www.businessweek.com/ap/2012-06/D9VEB8UG1.htm

Regardless of the underlying realities (there’s no money coming anytime soon), Spanish banks shares have risen during the last two weeks while the yields on Spanish bonds (most notably the ten year) and Spanish CDS have fallen.

There are three reasons for this:

1) Traders are praying that somehow the €100 billion will magically appear AND prove to be enough to support Spain’s banking system.

2) Spain successfully (depending on your definition of that word) sold €2.2 billion worth of two, three- and five year bonds (only €2 billion was expected).

3) Two auditing firms announced that Spain’s banks only need between €51 and €62 billion in capital to be solvent again.

Regarding #1, neither the ECB, nor the Fed, nor the IMF, nor the EFSF, nor the ESM, nor China can provide €100 billion for Spain. Those are the facts. The only one of the above entities that could even be a possibility is the ESM which, as noted before, doesn’t exist yet, and which Germany and Finland do not want buying sovereign bonds without “conditions.”

However, let’s say, for the sake of argument, that somehow the ESM is created on time and does have €100 billion to give to Spain (unlikely given that Spain and Italy account for 30% of the ESM’s funding). Even then Spain would still need more capital: remember, Spanish banks are currently drawing €316 billion from the ECB while Spain’s Prime Minister has admitted in private that Spanish banks’ real capital needs are in the ballpark of €500 billion.

Regarding #2: the “successful Spanish bond auction,” the markets are ignoring the fact that during said auction the yields on Spanish five-year paper hit their highest levels since Spain joined the Euro. So Spain can raise money… but at VERY high yields.

The markets also seem to be ignoring the fact that the majority of the buying during the bond auction came from Spanish banks… which, as noted earlier, are currently receiving €316 billion from the ECB. This tells us that:

1) The rest of the world isn’t interested in Spanish debt (for obvious reasons).

2) Even Spanish banks aren’t interested in buying Spanish sovereign debt unless it’s at very high yields (permitting them to pocket the spread between the interest they earn on the bonds and the interest they owe the ECB for the emergency loans they’re using to buy the debt).

In simple terms, an honest assessment of the Spanish bond auction shows it to be an absolute disaster. However, the EU media and political leaders are desperate to play it off as a great success because telling the truth would result in the acceleration of the Spanish banking system’s collapse (which is still coming regardless).

Finally, let us turn our attention to the alleged “audits” that found Spanish banks only need between €51 and €62 billion in capital to be saved.

First off, these audits were completed in a matter of weeks. Given that no one, not the Spanish Government nor the Spanish Bank themselves, have any incentives to reveal the true extent of the Spanish Banking system’s problems, I highly doubt that the auditing firms were provided with accurate information (remember, the recently nationalized Bankia passed the ECB’s stress tests).

Secondly, the auditors based their analysis on a “worst-case economic scenario” of a 6.5% drop in Spanish GDP between 2012 and 2014.

Let’s put this number into perspective: Greece’s GDP fell 6.9% in 2011 alone. And Spain is sporting comparable unemployment numbers to Greece, while Spanish banks are even more leveraged than their Greek counterparts. Given these facts, assuming that Spain’s economy will only contract by 6.5% between 2012-2014 is laughably naïve.

Indeed, one has to wonder… if these audits were so great and Spain has nothing to hide, why were the deadlines for the audits to be performed by Deloitte, KPMG, PwC and Ernst & Young pushed back from the end of July until September?

Finally, how can Spanish banks only need €51-€62 billion in capital when they’re drawing €316 billion from the ECB every month? And didn’t Spain’s Prime Minister admit in private that real Spanish bank capital needs may be around €500 billion?

Indeed, if Spain’s banks need so little capital to be solvent again, why did Spain plead with the ECB for a rescue in the middle of last week (remember, Spanish banks were the primary buyers of the most recent Spanish sovereign bond auctions)?

Spain pleads for ECB rescue as bond markets slam shut

Yields on 10-year Spanish bonds surged to a record high of almost 7.3pc as investors ignored the victory of pro-bailout parties in Greece’s elections.

The closely-watched two-year yield rocketed by 65 basis points in a matter of hours, signalling a near-total collapse of confidence in Spain’s €100bn (£80.3bn) rescue from the EU last week to shore up its banking system.

Cristobal Montoro, the economy minister, warned that Spain is now in a “critical” condition and pleaded with the European Central Bank to act with “full force” to defeat markets hostile to the euro project.

To conclude, Spain is not going to get €100 billion anytime soon (if ever), Spanish banks are all insolvent, and these recent audits aren’t worth the paper they’re written on.

However, enough folks were suckered into believing that Spain’s woes are not only solvable but will be solved in the near future. As a result of this, the Spanish Ibex has bounced hard in the last few weeks. Spanish bank shares are rallying. And Spanish yields are dropping.

I view all of these developments as a terrific setup to prepare for when Spain begins the “next leg down.”

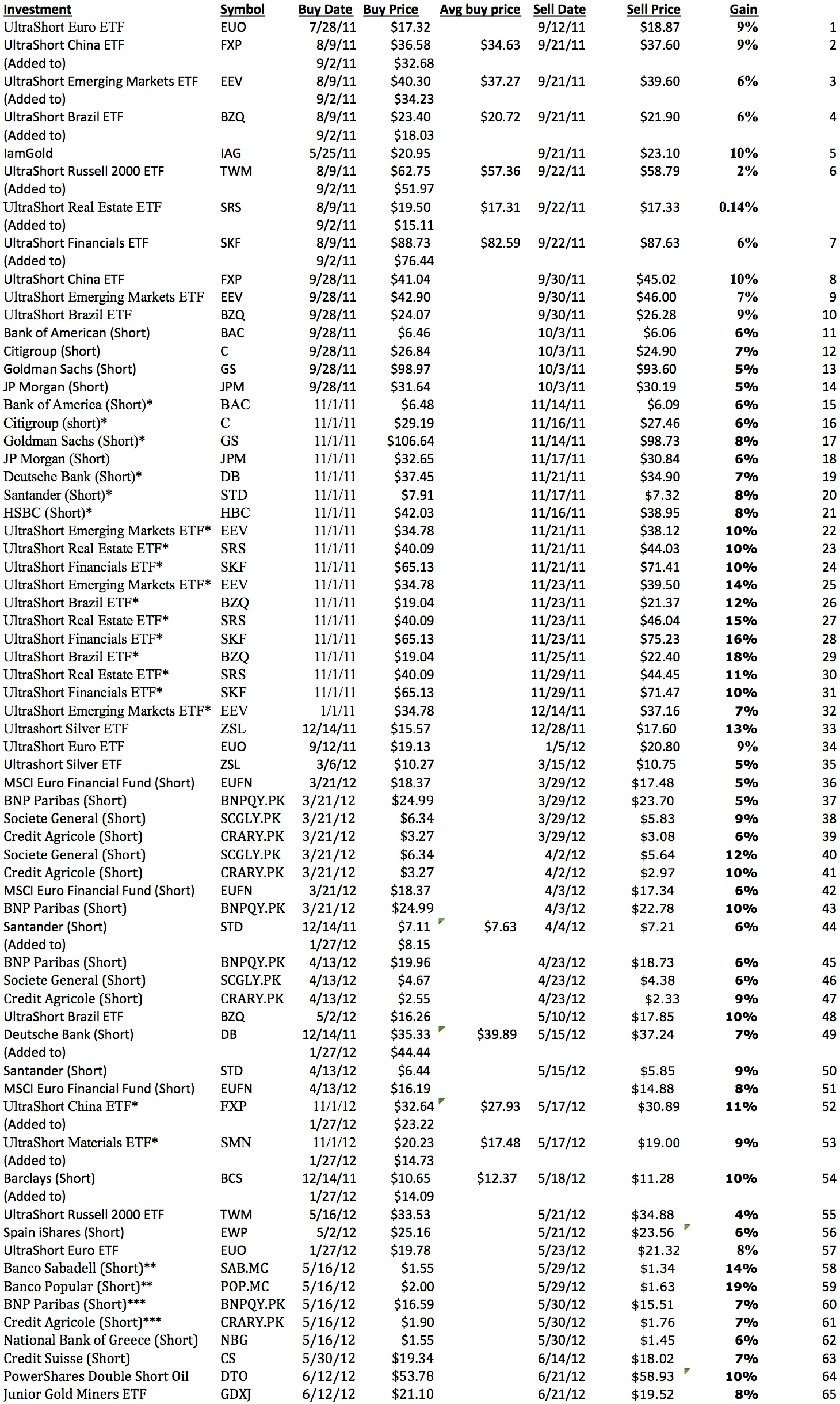

With that in mind, I’ve begun positioning subscribers of my Private Wealth Advisory for the next leg down. We’ve already locked in over 30 winning trades this year by finding “out of the way” investments few investors know about and timing our positions to benefit from the various developments in Europe. When you combine this with our 2011 track record, we’ve had 65 straight winners and not one closed loser since July 2011. If you think this is sounds “too good to be true,” you can Click Here to See Our Confirmed Trades.

Indeed, we just locked in two gains of 8% and 10% in less than two weeks’ time. In fact, this track record is getting so much attention that we’ve decided to only make 100 more slots available before we close the doors on this newsletter and simply start a waiting list. Already 70 slots have been reserved, leaving just 30 left.

To learn more about Private Wealth Advisory and lock in one of those last 30 slots…

Best Regards,

Graham Summers

Chief Market Strategist

Phoenix Capital Research

{kind=link}