To understand the recent shift in policy by the European Central Bank (ECB) and Bank of Japan (BoJ), we need to first revisit what lead us to this point.

With that in mind, let’s take a step back to mid-2016.

At this time, the US Fed was the ONLY Central Bank that was tightening policy. Meanwhile, the ECB, BoJ, Bank of England (BoE) and Swiss National Bank (SNB) were engaged in what can only be described as EMERGENCY levels of easing.

The worst offender was the BoJ, which launched a policy of targeting 0% on the 10-Year Japanese Government Bond (effectively announcing “we will print as much money as it takes to keep these bonds at this level”).

All told, Central Banks were printing over $160 BILLION in new currency per month at this time. This was MORE than they were printing at the depths of the 2008 crisis. And they were doing this at a time when their respective economies (Europe, Japan, the UK and Switzerland) were all growing.

Put another way, Central Banks, with the exception of the Fed, were pumping record amounts of liquidity into their respective financial systems at a time in which their respective economies were no longer flat lining.

And that is when inflation was unleashed.

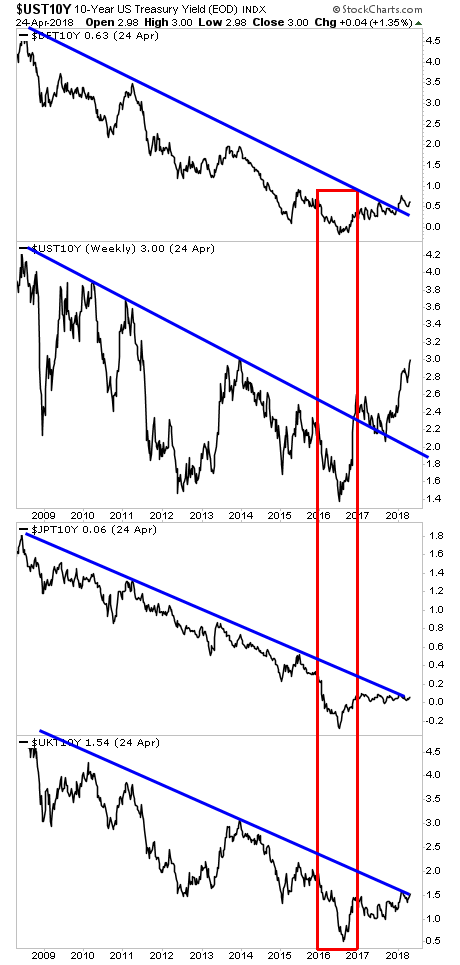

The most notable illustration of this concerns the bond markets. Sovereign bond yields are meant to trade based on economic activity and inflation. So if inflation rises, bond yields should rise and bond prices should fall.

This is precisely what happened in mid-2016 with yields on the 10-Year German Bund, 10-Year US Treasuries, 10-Year Japanese Government Bonds, and 10-Year UK Gilds, all rapidly rising (see the red rectangle below). Since this time, these same bonds have either broken their long-term downward trendlines (Germany and US) or are now challenging them (Japan and UK).

Put simply, starting in mid-2016 it became clear that Central Banks had overstepped with their monetary policies and the bond markets were beginning to revolt. I say “beginning” because it wasn’t until mid-to-late 2017, that things really became problematic in the bond markets.

While the financial media likes to focus on stocks because they are more volatile and therefore offer greater potential reward, Central Banks are FAR MORE interested in the bond markets. If stocks crash, some investors go bust. If bonds crash, entire nations go bust (see Greece in 2010-2012).

For this reason, I stated back in mid-2017 that Central Banks had a choice:

- Continue to engage in reckless money printing and risk blowing up the bond markets, thereby rendering most developed nations insolvent (current debt loads are so great that higher interest rates would rapidly lead to these nations failing to make debt payments).

- Taper monetary policy, save the bond bubble, and sacrifice stocks.

From mid-2017 until this month, Central Banks opted for #2. Both the ECB and the BoJ began sending signals that they would be walking back/ tapering their monetary policies.

Here’s the ECB in November 2017:

The European Central Bank is assessing a key element of its stimulus plan that looks likely to gain in prominence next year.

The ECB is reviewing its corporate-bond buying program, according to euro-area officials familiar with the matter. The study by the Market Operations Committee is largely looking at the effectiveness of the strategy, which has spent 126 billion euros ($148 billion) so far, and how it influences the supply of credit to the euro-area economy.

Source: Bloomberg

Here’s the BoJ that same month:

… it looks as if Kuroda (should he be reappointed by Prime Minister Shinzo Abe) has every intent of abandoning his fixation with a zero percent 10-year government bond yield. Kuroda said this of the consequences of keeping interest rates too low:

Another issue that has recently gained attention with regard to the impact on the functioning of financial intermediation is the “reversal rate.” This refers to the possibility that if the central bank lowers interest rates too far, the banking sector’s capital constraint tightens through the decline in net interest margins, impairing financial institutions’ intermediation function, so that the effect of monetary easing on the economy reverses and becomes contractionary.

Source: Bloomberg

Put simply, from mid-2016 onward:

- Central Banks engaging in emergency levels of QE at a time in which their respective economies were growing.

- Inflation bottoming then beginning to rise.

- Bond markets starting to revolt.

- Central Banks opting to walk back their QE programs.

This concludes this first part of our analysis of current Central Bank policy. Stay tuned for the second part due out tomorrow.

In the meantime, if you are growing concerned about the current Central Bank created bubble bursting…. we are putting together an Executive Summary outlining all of these issues as well as what’s coming down the pike when the Everything Bubble bursts.

It will be available exclusively to our clients. If you’d like to have a copy delivered to your inbox when it’s completed, you can join the wait-list here:

https://phoenixcapitalmarketing.com/TEB.html

Best Regards

Graham Summers

Chief Market Strategist

Phoenix Capital Research