War is inherently inflationary for the following reasons:

- Governments ramp up spending to fund the war effort: weapons, personnel, logistics, and reconstruction.

- The potential for supply side disruptions: in a globalized world, war can disrupt the production of natural resources as well as their shipping routes.

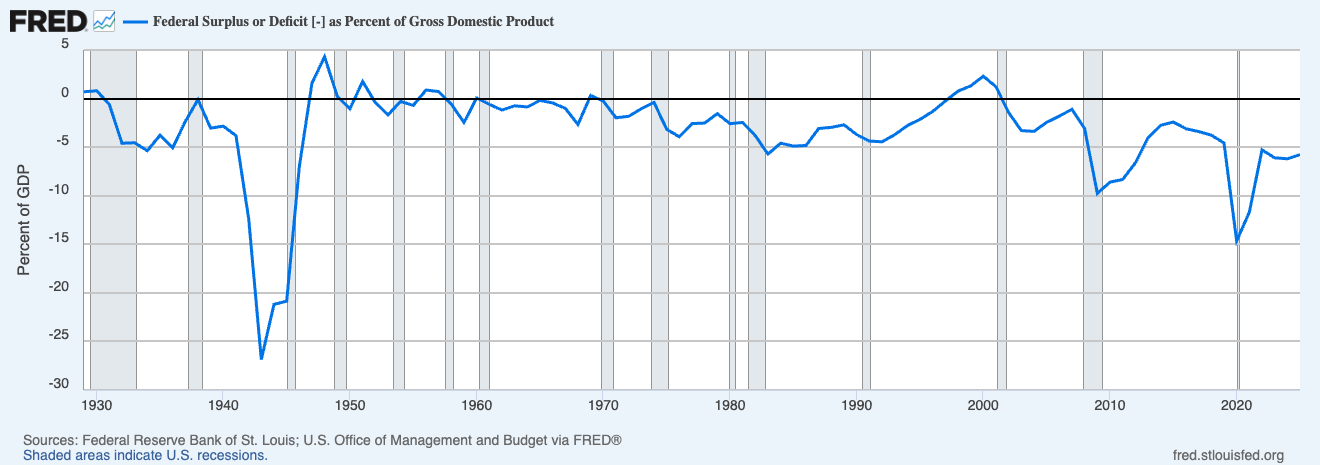

Regarding #1, the Trump administration was already running large-scale deficits before this conflict. As I’ve noted previously, the U.S.’s current Deficit to GDP ratio is larger than those it has run in all but three of the recessions of the last 100 years. And bear in mind, the Trump administration is running these large-scale deficits at a time when the U.S economy is still growing!

In this context, any increase in spending driven by geopolitical tensions will increase the U.S.’s already massive deficit, which in turn will balloon the U.S.’s debt issuance.

That is highly inflationary.

This alone is problematic. But when we consider the War in Iran’s potential for disrupting global energy supplies, and consequently inflation, things become quite serious for the U.S.

Iran borders the Strait of Hormuz to the North. This is a narrow (~30 miles wide at its narrowest point) critical shipping lane for global energy supplies: 20% of the world’s oil and liquified natural gas (LNG) supplies pass through this lane.

Any closure of this shipping lane would be a major problem for the energy markets. Indeed, it was the threat of its closure that triggered the ~80% price spike in oil from $67 per barrel to over $120 per barrel during the first week of this conflict. They’re retesting the highs as I write this.

To be clear, the world could absorb an energy shock like this if it was short-lived. But if the Iran conflict drags on for weeks or months (which is quite likely given all the issues I’ve already outlined), then higher energy prices will rapidly increase inflationary pressures in the U.S.

Why the U.S. is Susceptible to Another Inflationary Spike

One of the dominant themes in the financial media today is that inflation has been tamed and disinflation is taking hold (disinflation is when inflation continues to rise, albeit at a slower pace).

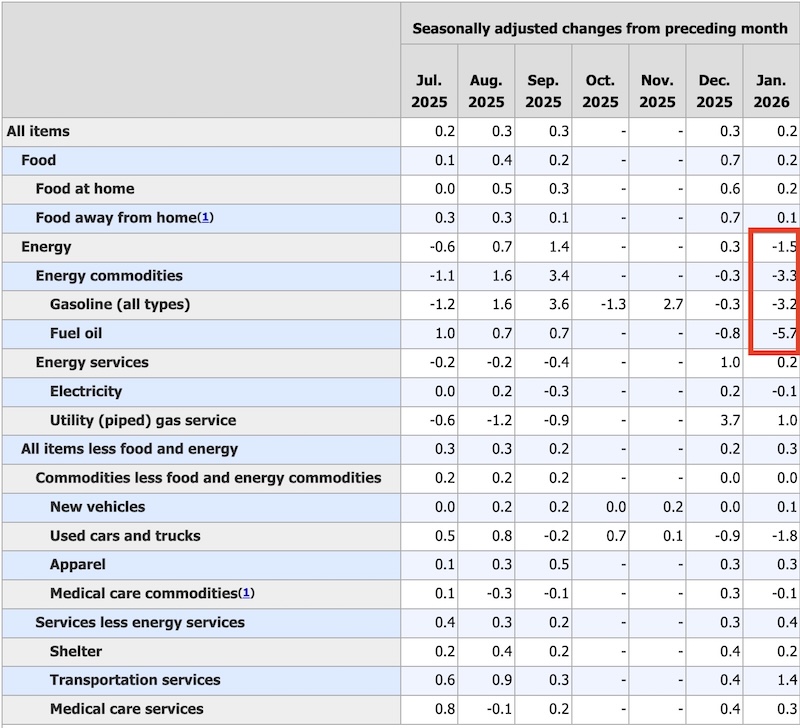

This narrative is largely being driven by accounting gimmicks in the official inflation data. When we dive into the actual components of the CPI, we find that the only segment that is declining in value is energy prices (well that and used cars and trucks).

See for yourself.

In this context, a spike in energy prices driven by the conflict in Iran has the potential to reverse the trend of disinflation rather quickly. This is particularly true when you consider that energy prices input into everything: heating, electricity, shipping, food, manufacturing, etc. This is why oil shocks have precipitated inflationary spikes in the past. And why another oil shock would easily ignite another wave of inflation today.

Please note that we are primarily focusing on the CPI in the above analysis. And the CPI is a highly manipulated data point due its political significance, e.g. the Bureau of Labor Statistics, or BLS, utilizes numerous gimmicks (the weighting of components, bad quality data, outright lying about prices movements) to understate the true increase in cost of living in the U.S.

Indeed, when we look at other, less popular inflation measures that are based on real world economic data, it is clear inflationary pressures in the U.S. were already rising before the conflict in Iran.

Real-World Inflationary Measures Were Rising BEFORE the Iran Conflict Ignited

The Institute for Supply Management (ISM) publishes two monthly surveys — one for manufacturing and one for services. Each includes a Prices Paid sub-index, which asks purchasing managers whether they’re paying more, less, or the same for inputs. A reading above 50 for either survey indicates that prices are rising.

The readings for the ISM Manufacturing Prices Paid since December 2025 are:

- December: 58.5

- January: 59.0

- February: 70.5

The readings from the ISM Services Prices Paid surveys since December 2025 are:

- December: 65.4

- January: 66.6

- February: 63.0

Unlike the headline inflation numbers like the Consumer Price Index (CPI) or Personal Consumption Expenditures (PCE), these are real-world surveys taken from the frontlines of the economy without gimmicks. And they tell us that inflation was already surging BEFORE the U.S. struck Iran.

So again, the War in Iran is a major wildcard as far as inflation is concerned. And I believe the stock markets are underestimating this risk.

Please note that the yield on the 1-Year U.S. Treasury, which moves in anticipation of inflationary expectations (among other things) is rising not falling. Since early February the yield on this bond has risen from a low of 3.35% to its current level of 3.6%. This suggests the bond market has removed ANY expectation of additional Fed rate cuts over the next 12 months (the Fed Funds rate is currently 3.5%).

Put simply, the markets are indicating another round of inflation is coming shortly. The time to position for this is now before it hits.

On that note, we just published a Special Investment Report concerning FIVE secret investments you can use profit from the next major bull run in precious metals miners.

The report is titled Survive the Inflationary Storm. And it explains my top precious metals plays, including their names, their symbols, and the resources they own. These are HIGH OCTANE positions that

rallied 75%, 140%, 150%, 180%, 280% and an incredible 574% in 2025! And I wouldn’t be surprised to see them repeat this performance in 2026.

Normally I’d charge $499 for this report as a standalone item, but in light of what is unfolding today, we are making just 100 copies available to the public.

To grab one of the last remaining copies…

Best Regards

Graham Summers

Chief Market Strategist

Phoenix Capital Research