As I have outlined since November, the Tech sector was the primary reason the stock market was struggling. Obviously, the war in Iran was the catalyst for the rapid decline, but stocks were poised for a correction long before that conflict began.

In broad strokes, the issues for Big Tech were:

- Big Tech had gone “all in” on the AI-revolution, committing over $400 billion per year building out AI-infrastructure.

- These capital expenditures were so massive that companies such as Meta and Alphabet were issuing debt to cover these expenses, despite earnings hundreds of billions of dollars in profits per year.

- Multiple “red flags” had arisen concerning the productivity and profitability of AI. Specifically…

- AI cannot “think,” it can only organize information based on probabilities.

- AI hallucinates or makes things up 15%-52% of the time (depending on the model).

- AI suffers from “hive mind” or lack of creative responses with different models providing similar answers to the same open-ended questions.

As a result of this, the current chapter for the AI revolution began to stall out in late 2025. From that point onward, the Big Tech/ Mag-7 stocks struggled to catch a bid. Once the war in Iran began, things got ugly fast.

This presented something of a conundrum…

Yes, AI in its current had numerous issues, but at the same time, Big Tech (and the Trump administration) were “all in” on this technology, investing hundreds of billions of dollars in its build out/ development. Put simply, the “demand/ economic growth” of the AI-buildout will happen regardless of how successful the technology proves to be in the long-run.

As a result of this, capital has begun shifting away from the Big Tech hyperscalers to various bottlenecks in the AI theme, specifically energy/hard asset requirements.

The great irony of AI is that it’s more of a hard asset/ commodity story than a tech story. Let’s start with some jaw-dropping numbers:

- The International Energy Agency (IEA) projects that electricity demand from data centers will more than DOUBLE from 460 terawatts-hours in 2024 to over 1,000 terawatt-hours by 2030. To put that into perspective it is equal to the energy demands for France AND Germany combined.

- From a chips perspective, the global race for Graphics Processing Units (GPUs) is so aggressive that…

-

- Even older chips (Nvidia’s B200 chips were first introduced in late 2024) cannot be acquired. The Big Tech hyper-scalers have bought every chip to the point that new orders will take 12-16 MONTHS to be fulfilled.

- Taiwan Semiconductor Manufacturing Company (TSMC) which builds chips for Nvidia has sold out every manufacturing slot for 3mn chips through 2028. Put another way, if you want to order a 3mn chip today, your order won’t be filled for at least 16 months.

- The stacking of memory chips required to give GPUs the data they need can only be performed by three companies in the world. All three of them are booked solid through 2026.

- Data centers and chips both require an ungodly number of natural resources. A single 100 MW Hyperscale AI Data Center requires:

- Copper: ~2,200 tonnes for wiring, cooling loops, and power distribution — 3-4x more than a conventional data center

- Iron/steel: up to 14,000 tonnes for structural framework, transformers, generators

- Aluminum: ~1,200 tonnes — busbars, enclosures, cooling components

- Graphite: ~290 tonnes — backup power systems and UPS units

- Lead: ~240 tonnes — backup battery systems

- Nickel: ~220 tonnes — backup power and battery systems

- Cobalt: ~40 tonnes — backup batteries and UPS systems Lithium: ~30 tonnes — battery backup systems

- Water: up to 5 million gallons per day, ongoing — equivalent to a city of 50,000 people

- Power draw: 100–500 MW continuous, 24/7/365

And remember, this is happening regardless of how AI turns out. Big Tech/ the U.S./ China are fully committed to this process to the tune of $500+ BILLION per year.

In this sense, from an investment perspective, the AI trade has morphed from focusing on hyperscalers to the hard asset/ tech needs of the revolution.

This is where the BIG money will be made going forward.

Some examples…

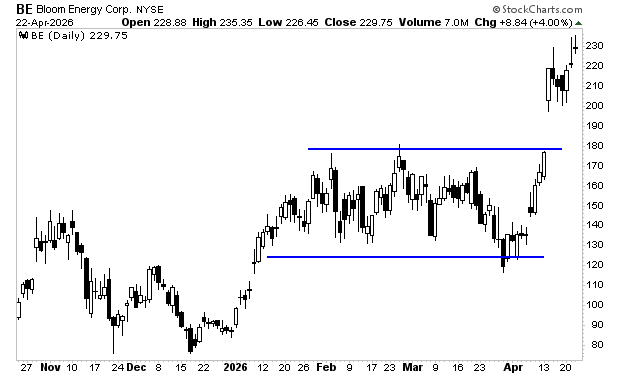

Bloom Energy (BE) builds solid oxide fuel cells (SOFCs) — essentially small, modular power plants that generate electricity on-site. As such it’s becoming a major player for AI energy needs. The stock has gone vertical.

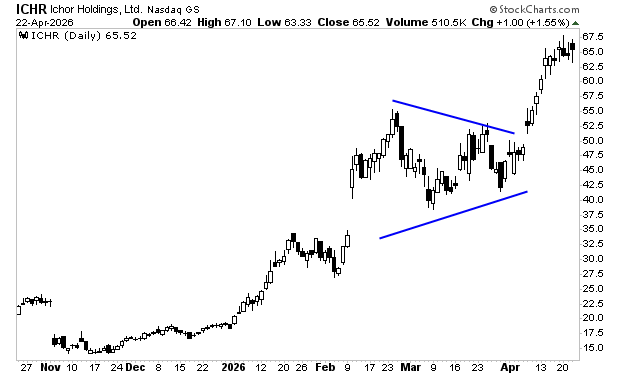

Ichor Holdings (ICHR) makes the precision plumbing systems inside chip-making machines that control the exact flow of gases and chemicals used to manufacture semiconductors. Its stock is breaking out in a big way.

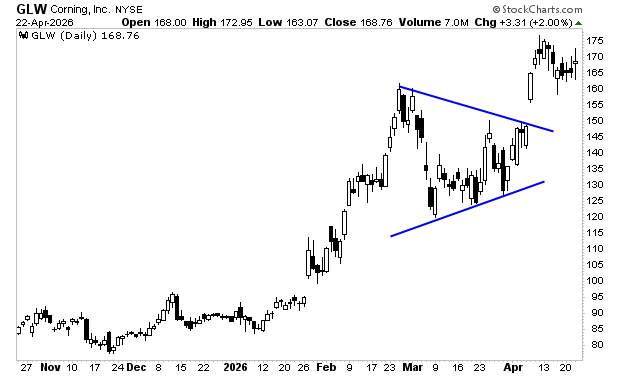

Corning (GLW): their optical fiber is the backbone of the data center networks that connect thousands of servers together.

Big picture: there is a LOT of money to be made in the AI trade. But the focus has shifted from the hyperscalers to the “picks and shovels” plays profiting from the AI buildout. These companies will do well no matter how the AI revolution turns out.

Join 30,000 serious investors in receiving my daily daily market commentary FREE.