So, the gold is free?!?

I just found a company that might be the single most exciting potential buyout target in the entire precious metals space.

For starters, this company doesn’t need to find gold. The gold’s already there. Some six million ounces of it valued at over $2 billion (with a “B”). And thanks to the history of these assets, the company knows the gold can be mined.

You see, this company owns the rights to not one but two historic mines that were actively producing gold (over 3.2 million ounces) a few decades ago. However, because the price of gold was just $300 at that time, once the gold that was cheap to mine had been extracted, the resource was no longer economical, so the mines were closed and the exploration for new discoveries ended.

Fast forward to 2026, and gold is now over $4,500 per ounce and both mines are not only economical but under new ownership and being fast-tracked for production.

Why?

Because these mines are in Utah and Idaho, two of the most mining friendly places in the world right now: the Trump administration is fast-tracking the domestic production of critical minerals to reduce the U.S.’s reliance on foreign adversaries, specifically China. And the President’s team has deemed gold a “strategic resource.”

In this context, the company I’m writing about is extremely attractive as a takeover target, both for its resource base (~6 million ounces of gold) and its location (the western U.S.).

Now, here’s where things get really interesting.

As I mentioned before, the mines this company owns were actively producing in the past. As a result of this, the company already has a lot of mining infrastructure in place. I’m talking about roads, powerlines, offices, an ADR (Adsorption-Desorption-Regeneration) gold processing facility, solution ponds, a water treatment plant and more.

All told, these infrastructure assets are valued between $150 million and $250 million in capital savings on potential redevelopment of the mines.

The company’s entire market cap is just ~$200 million.

So, at today’s prices, the company is trading at the value of its mining infrastructure alone. Put another way, you are getting the value in gold, all ~$2 BILLION worth of it, FREE.

I’m not the only one who has noticed this situation. Legendary natural resource investors Rick Rule and Jonathan Goodman have stakes in this company. Numerous smart money natural resource investment firms like EMR Capital, Sun Valley Gold and others have positions as well. In fact, if you break down the company’s share structure, only about 16% of its shares are owned by the general public.

Now, in precious metals mining, nothing is guaranteed. Any number of things can go wrong between finding gold and getting it out of the ground.

But the opportunity to get ~$2 billion worth of value in gold for FREE is a rare situation. And I doubt it will last long.

Think of it this way…

If I’ve already uncovered the hidden value of this company and its resources, what do you think the gold mining majors like Newmont or Barrick and the many mid-tier gold miners like SSR, Centerra, and others, with their army of analysts, consultants and lawyers, are doing? Do you really think they’re going to pass up the opportunity to acquire two western U.S.-based assets with over $2 billion worth of value in gold that could be actively mined beginning as soon as 2029?

Me neither. As Rick Rule puts it, either shares go MUCH higher as these projects are de-risked or the company gets “bought out.”

I’m talking about Revival Gold (TSX Venture Exchange: RVG, OTC: RVLGF).

Two Historic Assets with 6 Million Ounces of Gold in the Most Mining Friendly Region in the World

Revival owns two primary assets:

- The Mercur project in Utah.

- Beartrack-Arnett project in Idaho.

First and foremost, we need to assess the fact that these assets are located in extremely mining-friendly regions. The Trump administration has moved aggressively to accelerate mining in both states, framing domestic mineral production as a matter of national security.

The centerpiece of this effort is Executive Order 14241, signed in early 2025, directing federal agencies to facilitate domestic mineral production “to the maximum possible extent.”

In broad strokes, this EO aims to do two primary things:

- Reduce U.S. dependence on foreign adversaries (primarily China) for critical mineral supply by boosting domestic production (cutting regulations, accelerating permits, and reorienting federal land use to focus on mineral extraction).

- Treat mineral production as a national security imperative, not just an economic one, using national security funding mechanisms (Defense Production Act) to finance domestic mining.

To summarize, the Trump administration is “all in” on fast-tracking the domestic production of critical minerals, including gold. So, the fact that Revival Gold’s primary assets are located in the U.S., specifically in the mining-friendly states of Utah and Idaho makes it extremely attractive as a takeover target compared to other mining companies with assets in less friendly locations.

Now let’s talk about the assets themselves.

The Mercur Project: 1.4 Million Ounces of Gold

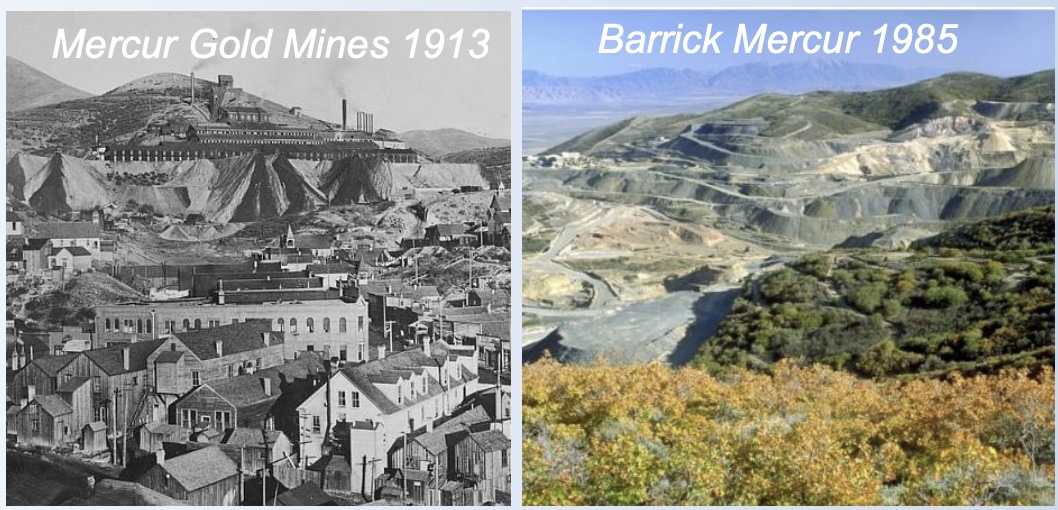

Revival Gold’s primary focus is on resuming production at the Mercur Project located in the Oquirrh Mountains of Utah about 60 miles southwest of Salt Lake City.

The Mercur project has been actively mined for over a century. However, it’s critical to note that the property has never been consolidated into one Company’s hands before and much of the property hasn’t been actively drilled or explored using modern techniques. Barrick Gold mined the resource from 1985 to 1997 and, together with others, produced over 2.6 million ounces of gold. Barrick stopped mining when low gold prices (sub-$300 per ounce) made the project uneconomical.

Today, gold is trading north of $4,500 per ounce… and Mercur is VERY economical.

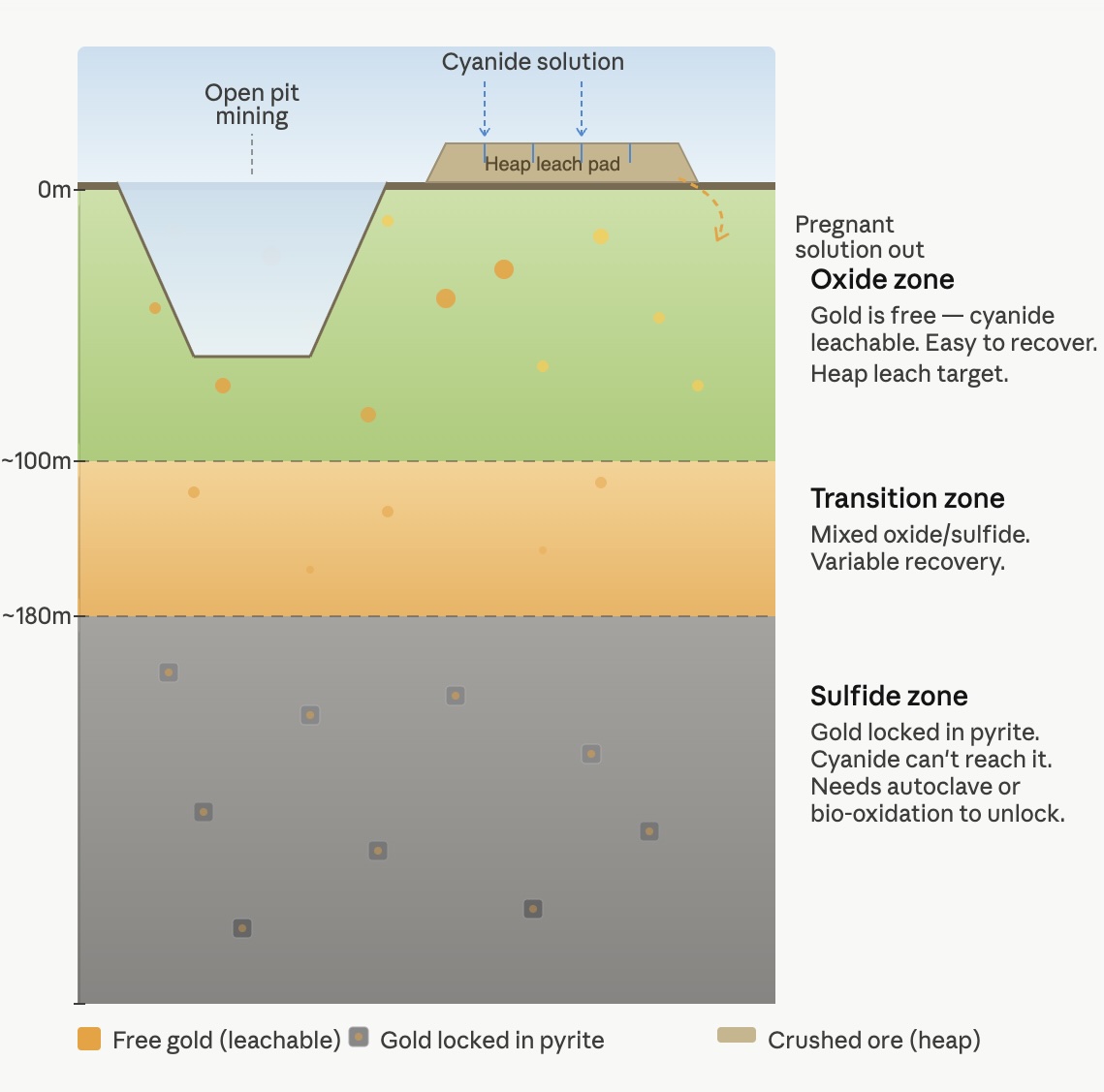

In terms of the geology, the Mercur Project is a Carlin-type deposit.

If you’re unfamiliar with “Carlin-type” deposits, they are named after the Carlin Trend in northeastern Nevada, where these types of deposits were first identified and described in the 1960s.

Without getting too technical, the defining characteristic of Carlin-type deposits is that the gold is invisible to the naked eye. Instead, it exists as submicroscopic particles — often just nanometers in size — locked within the crystal structure of iron sulfide minerals.

Now, there are two types of gold ore found in Carlin-type deposits: oxidized or sulfide. Of the two, oxidized is the preferred version because it means the gold is located close to the surface and can be mined relatively cheaply (the rocks can simply crushed and piled up and then treated with cyanide solution to recover the gold). The below graphic does a good job of illustrating the differences in locations for oxidized and sulfide gold in Carlin deposits.

The gold Revival has found at Mercur is oxidized. And we are not talking about a little, either. Revival estimates the Mercur project has 1.4 MILLION ounces worth and the deposit is still open to further discovery.

Revival has already completed its Preliminary Economic Assessment (PEA) on this resource, estimating that it will cost roughly $208 million to bring the resource to active production for the mine’s 10-year lifetime.

Once active, Revival believes the mine will be able to produce between 95,000 and 100,000 ounces of gold per year generating after tax annual cash flow in the ballpark of $180 million to $200 million assuming gold stays over $4,000 per ounce. This gives the mine a Net Present Value of $1.2 BILLION at $4,000 gold.

Again, Revival’s market cap is just ~$200 million.

So, there is already a four or even five-fold repricing potential as Revival moves forward de-risking this asset (the company expects to start production in 2029).

However, that’s not the only potentially good news for the company. Indeed, I’ve identified two potential upside catalysts for this resource that could hit within the next year.

Catalyst #1: Additional Discoveries at Mercur

Revival began a new drilling program at Mercur on April 28th 2026. As I write this, the company has two reverse circulation (RC) rigs engaged in a 16,000-meter drill campaign. The primary purpose of this drilling campaign is to upgrade the company’s knowledge of this resource in anticipation of its Preliminary Feasibility Study (PFS) due out in 1Q27 (more on this shortly).

This comes on the heels of a 2025 program that delivered. The final results, released April 7, included 2.75 g/t gold over 74.3 meters — with a high-grade intercept of 8.04 g/t over 12.5 meters inside that interval — at South Mercur.

Let me be clear: an 8.04 g/t hit was NOT in Revival’s original resource model. So, the current drilling program also aims to find out if there is in fact more gold at Mercur than Revival’s early 2025 estimate of 1.4 million ounces (0.8 million in Measured and Indicated and 0.6 million in Inferred).

Any additional discoveries here have the potential to push Revival shares higher. The company aims to continue drilling through to year end and should have initial data to share with the markets this summer so current shareholders won’t have to wait long for a potentially good surprise.

Which brings me to Catalyst #2…

Catalyst #2: the Preliminary Feasibility Study (PFS) Due Out in 1Q27

As I mentioned earlier, Revival has already published its Preliminary Economic Assessment (PEA) on the Mercur Project (that’s where the NPV of $1.2 billion comes from). The company is now moving towards completing its Preliminary Feasibility Study (PFS) which is the next step towards actively mining the resource.

This has the potential to ignite Revival shares higher.

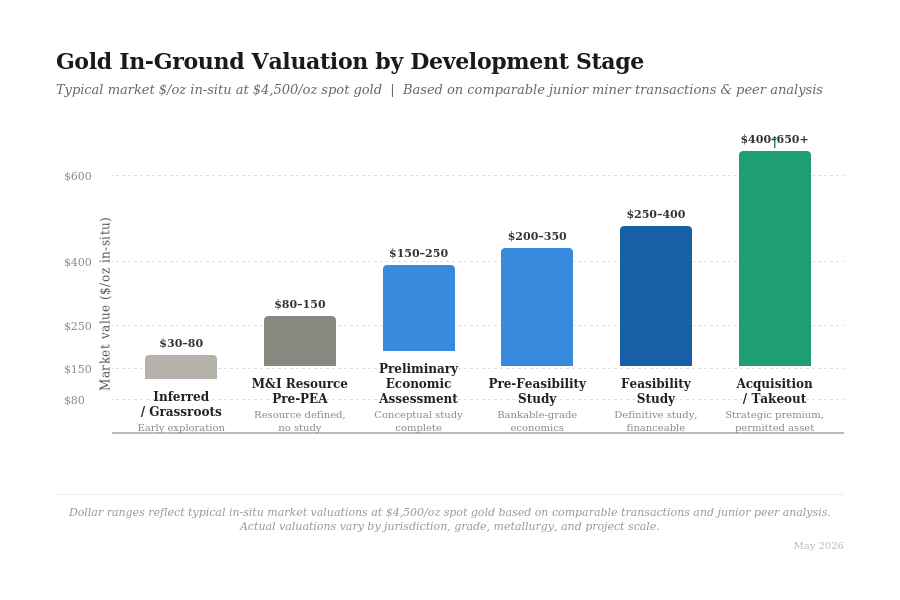

You see, the process of developing a gold resource has six primary steps. Each step from the initial discovery to the eventual takeout/ production “de-risks” the resource by reducing the uncertainty.

As the resource is de-risked, the market begins to give its gold a higher valuation as the below graphic illustrates.

Obviously, Revival is already underpriced based on this math (the company has done a PEA on Mercur which should result in the asset being valued at $210 million alone while its entire market cap is ~$200 million).

However, the point I’m making here is that when Revival publishes its PFS in 1Q27, even more risk will have been removed from the Mercur project which could result in a serious repricing of Revival’s shares.

Put simply, by buying shares in Revival Gold today, shareholders have not one but two distinct rerating catalysts on the horizon. Again, as legendary natural resource investor Rick Rule puts it… either shares go MUCH higher as Revival’s projects are de-risked or the company gets “bought out.”

Which brings me to Revival’s second, larger resource: Beartrack-Arnett in Idaho.

The Development of a Larger Resource Awaits Shareholders Down the Road

As I mentioned earlier, Revival is currently focusing on resuming production at the Mercur Project. This is primarily because Mercur is located on private land, so permitting runs through Utah’s Department of Oil, Gas and Mining (a state process) rather than the federal NEPA/BLM/Forest Service which is slower (more on this later).

However, it’s critical to note, that based on Mercur’s potential alone, Revival is undervalued: with gold at $4,000 per ounce the NPV for Mercur is $1.2 billion, while Revival’s entire market cap is just $200 million.

And Mercur isn’t even Revival’s largest asset! So, there’s another major catalyst awaiting Revival shareholders down the road.

That catalyst is the development of the Beartrack-Arnett project.

The 3rd Largest U.S.-Based Discovery since 2010

Beartrack-Arnett is a 6,300 hectares property located in Idaho.

As was the case with Mercur, Beartrack-Arnett previously produced gold, and in fact was the largest past-producing gold mine in the state: producing over 600,000 ounces of gold between 1994 and 2000. It too was closed when gold prices fell below $300 per ounce and the resource was no longer economical.

Revival assembled this package between 2017-2023. Today the company owns/ has optioned 100% of this property. And it has already discovered a considerable amount of gold: 2.4 million ounces of Measured & Indicated resources and 2.2 million ounces in Inferred resources (a total of 4.6 million ounces).

To put this into perspective, this is the 3rd largest U.S.-based new gold discovery since 2010 (Mercur is the 10th). And you’ll also note that Beartrack-Arnett is a higher-grade resource than the 1st or 2nd largest gold discoveries during this period.

Revival is actually further along in the process of derisking this project than it is with Mercur; the company has already completed both a Preliminary Economic Assessment (PEA) and a Preliminary Feasibility Study (PFS) on the first phase (open pit, heap leach) portion of this resource. The PFS was completed in 2023 forecasting annual production of 63,000 ounces with an All-In Sustaining Cost (AISC) of $1,235 per ounce. Based on gold price of $4,000 per ounce, the NPV for this resource is $790 million.

Remember, Revival’s entire market cap is just $200 million. And gold is over $4,500 per ounce, so the current NPV for Beartrack-Arnett is in fact much higher.

Revival plans to develop this resource, albeit at a slower pace than Mercur, primarily due to the increased regulatory burden: Beartrack-Arnett is on federal land and so must follow a tedious, 3 – 4 year process.

Without getting too technical, Revival will need to file a Plan of Operations with the Forest Service and State Regulators, perform a federally regulated NEPA Environmental Impact Statement (NEPA EIS), and get both state and federal agencies to sign off on the project. Even if nothing goes wrong, the process is expected to take upwards of four years.

Bottom line: from where Revival stands today, Beartrack-Arnett is on a 3 – 4 year permitting journey. This is another lower risk “brownfield” redevelopment project, but it will take more time for the value to be derisked by the market than for Mercur.

However, this doesn’t mean that Beartrack-Arnett doesn’t have any near-term catalysts. In fact, I’ve identified three of them:

Catalyst #1: Joss Zone Drill Results

Beartrack-Arnett resource is located in two mineralized zones: a near-surface resource amenable to open pit heap leach mining, and a deeper high-grade underground zone.

The PFS for this resource is based solely on the first phase near-surface part of this resource. The upside catalyst comes in the form of Revival’s current drilling on a second phase underground target called the Joss Zone.

Revival is actively drilling there right now with two rigs turning, and the early results are exceptional. The most recent hole hit 5.4 g/t gold over 32.6 meters — including a higher-grade section of 6.4 g/t over 19 meters.

To put that in context, the open pit heap leach resource that the entire PFS for Beartrack-Arnett was built on grades 0.74 g/t. So, the underground material is running six to eight times higher grade.

Several more holes have intersected this target zone with assays still pending. Every strong result that comes back expands the underground resource that currently sits completely outside the PFS economics — meaning the market isn’t pricing it at all.

Which brings me to catalyst #2.

Catalyst #2: Underground Resource Update

The Joss Zone currently hosts an Inferred resource of 877,000 ounces grading 4.05 g/t. An Inferred resource is the lowest confidence category under NI 43-101 — the Canadian standard for reporting mineral resources. It means the mineralization is real but not yet drilled out tightly enough to be classified as Measured or Indicated, which carry higher confidence.

The current drilling program is designed specifically to grow that number and demonstrate the broader scale of the underground deposit.

A materially larger underground resource — say 1.5 to 2 million ounces at similar grades — forces the market to reprice Beartrack-Arnett entirely. If this happens, Beartrack-Arnett stops being a heap leach restart story and starts being one of the highest-grade undeveloped gold deposits in the United States. The market should respond very positively to that news if it plays out.

And the upside continues once the company publishes a PEA on this underground resource (remember, both the PEA and PFS for Beartrack-Arnett are based solely on the near-surface portion of this resource).

Catalyst #3: An Underground PEA

Right now, those 877,000 underground ounces at 4.05 g/t contribute zero to Revival’s stated project economics. They don’t appear in the PFS. They don’t show up in the NPV. They’re essentially invisible to anyone doing a standard asset valuation.

An underground Preliminary Economic Assessment — a PEA — puts numbers on that resource for the first time. It models what it would cost to mine it, what it would produce, and what it’s worth. Revival’s CEO Hugh Agro has said publicly that the potential addition of an underground study to the heap leach restart creates a third phase of development and moves Revival toward its production target of 300,000 ounces per year. If a study gets published on the underground, that would be catalytic and the market would have to price it. That’s a rerating event.

In simple terms, Beartrack-Arnett may take longer to develop than Mercur, but it presents investors with significant upside catalysts due to the fact that the resource is currently being valued solely on the near-surface portion of this resource. So while Beartrack-Arnett likely won’t enter production until the early to mid-2030s, it still has the potential to unlock additional value to investors in the near-term.

OK, we’ve covered a lot of ground here, so let’s do a brief recap of the entire Revival Gold story

Overview

- Revival Gold (TSX-V: RVG, OTC: RVLGF) owns two past-producing gold mines in the U.S. with ~6 million ounces of gold currently valued at ~$2 billion.

- The entire company trades at a market cap of ~$200 million — meaning you’re paying for its mining infrastructure and getting the gold for free

- Only 16% of shares are available to the public — the other 84% of the company is locked up by Rick Rule, Jonathan Goodman, EMR Capital, and Sun Valley Gold and other smart money natural resource investors/ firms.

Mercur (Utah) — The Near-Term Catalyst

- Mercur is a 1.4 million ounce Carlin-type oxide deposit, 60 miles southwest of Salt Lake City

- Mercur is located on private land — permitting runs through Utah’s state process

- The PEA is already complete: NPV of $1.2 billion at $4,000 gold, $208 million capex, 95-100,000 oz/year production, $180-200 million annual after-tax cash flow

- Production targeted for 2029

- Two near-term catalysts for share price rerating:

- Two RC rigs drilling now in a 16,000-meter campaign — initial results expected this summer.

- PFS due Q1 2027 — which will significantly derisk the asset and force a repricing in the market’s perceived value of the asset.

Beartrack-Arnett (Idaho) — The Longer-Dated Prize

- Beartrack-Arnett is a 6 million ounce resource located in Idaho, representing the 3rd largest U.S.-based new gold discovery since 2010

- The PFS for the first phase near-surface portion of the resource is already complete: NPV of $790 million at $4,000 gold, 65,300 oz/year, AISC of $1,235/oz

- Beartrack-Arnett is located on federal land and will require a 3 – 4 year Forest Service/NEPA EIS permitting process with production slated to start in the mid-2030s

- There are three near-term catalysts regardless of the permitting timeline on the first phase operation:

- Underground Joss Zone drill results hitting now — 6.4 g/t over 19 meters, six to eight times the open pit grade

- Underground resource update — Joss currently hosts 877,000 oz at 4.05 g/t none of which is included in PFS economics

- Underground PEA for the second phase underground portion of Beartrack-Arnett would reveal a value on ounces the market is currently pricing at zero

So, what’s it worth?

To be clear, Revival has a lot going for it.

For one thing, its resources are based in the U.S., which is one of if not the most mining friendly regions in the world thanks to the Trump administration’s push for the domestic production of critical minerals (including gold).

Secondly, the company knows the gold is there: both resources were previously producers. And Revival has already done the work to establish both resources’ current market values based on what’s it has discovered in today’s dollars. All told, the NPV for Mercur and Beartrack-Arnett are worth ~$2 billion with gold at $4,000 per ounce.

The company’s market cap is just $200 million. The NPV absolutely dwarfs this number at any reasonable gold price.

Finally, and perhaps most importantly, the smart money is heavily invested in this company. It has one of the best share structures I’ve ever seen with natural resource legends like Rick Rule and Jonathan Goodman putting their capital to work alongside management/ insiders. Indeed, only about 16% of its shares are understood to be freely available to the general public.

A U.S.-based asset, that previously was active, currently trading at ~10% of its NPV with some of the biggest names in natural resource investing and management locking up 84% of the shares?

As Rick Rule puts it, either shares go MUCH higher as these projects are de-risked or the company gets “bought out.” Whichever option plays out, investors will benefit.

With that in mind, we are adding Revival Gold to the Resource Vault. We will be introducing you to the company’s management directly, taking a trip to visit Mercur, and providing regular updates on drilling results going forward.

More to come…

Good Investing,

Graham Summers, MBA

DISCLAIMER

Disclosure: This document has been disseminated on behalf of Equity Catalyst Partners, LLC. Equity Catalyst Partners, LLC has been engaged by Revival Gold Corp to provide marketing and investor relations services and is compensated by Revival Gold Corp in the amount of $45,000. Equity Catalyst Partners, LLC is not registered under applicable Canadian securities laws and does not provide investment advice, recommendations, or solicitations to buy, sell, or hold securities. Any information provided by Equity Catalyst Partners, LLC is for general information only and should not be relied upon for investment decisions. Readers should conduct their own research and consult a registered investment advisor.