By Graham Summers, MBA

Thus far in 2023, there have been three major bank failures. And I do mean MAJOR: all told the three banks had $532 billion in assets. That amount is actually greater in size that the combined assets of the 25 banks that failed in 2008.

What is going on here?

What is going on is that the Fed created this mess… and bad risk management at the banks has exacerbated it.

Let me explain.

Traditionally, banks make money as follows:

1) You deposit your money at the bank.

2) The bank pays you a low interest rate on this deposit.

3) The bank turns around and loans out $5, $7, even $10 in loans for every $1 you deposited. The bank charges a much higher rate of interest on these loans than the interest rate it pays you on your deposit.

4) Alternatively, the bank buys $5, $7, or even $10 in long-duration assets (Treasuries, or other long-term bonds) for every $1 you deposited.

5) The bank pockets the spread between the interest it earns on its loans/ bonds and the interest rate is pays you on your deposits.

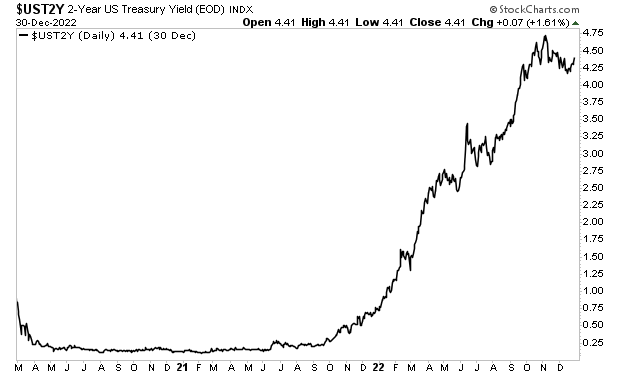

This situation works well provided the Fed keeps interest rates low. Unfortunately for the banks, the Fed unleashed inflation by printing ~$5 TRILLION between 2020 and 2022.

Bond yields trade based on many things… including inflation. And once inflation entered the financial system, Treasury yields ripped higher.

When Treasury yields rise, bond prices FALL. And who was sitting on trillions of dollars’ worth of long-term Treasuries and loans that traded based on long-term Treasuries?

You guessed it… the regional banks.

Courtesy of the Fed’s idiocy, the banks were destined to be sitting on hundreds of billions of dollars worth of losses on these assets.

But it gets worse.

Once the Fed finally decided to get off its rear and do something about inflation, it embarked on its most aggressive rate hike cycle in history, raising rates from 0.25% to 5% in the span of a single year.

Why does this matter?

Remember how banks pay you a low interest rate on your deposit? Well who is going to want to keep his or her money in a bank that pays 0.3% at best… when he or she can earn 4% or even 5% in a money market fund or short-term Treasury bond, courtesy of the Fed raising rates so high so fast ?

And so, depositors began pulling their money from banks… and not by a little: 2022 was the first year since 1945 in which money on a NET BASIS left the banking system in the U.S.

But hang on… remember how the bank loaned out or bought $5, $7, or even $10 worth of loans or long-term assets based on every $1 you deposited in the bank? Well when you pull your money out of the bank, the bank has to unload all that stuff to maintain its capital requirements.

And so, the Fed delivered the ultimate 1-2 punch to the U.S. regional banking system.

The first punch was it ignored inflation to the point that the banks were sitting on hundreds of billions of dollars’ worth of losses.

However, the KO punch was the Fed raised rates aggressively, which resulted in depositors pulling money out of the banks in search of higher returns on their cash.

Now, don’t get me wrong. The banks are partially to blame for the fact that didn’t act once the Fed announced it would be raising rates to end inflation. With proper risk management (bond hedges for instance) these banks would have been better prepared for the bond market massacre of 2022.

However, even careful risk management would have done nothing to help these banks once depositors started pulling their money out. And no bank could raise its deposit rates to 4% or 5% to compete with money market funds or short-term Treasuries while staying in business.

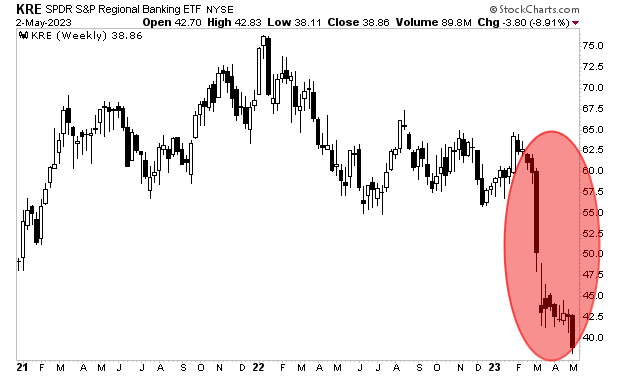

And so we get this: a situation in which MAJOR regional banks are going bust and the regional bank ETF has lost a third of its value in the span of six weeks.

This situation is nowhere near over. According to some analysis, HALF of the U.S.’s banks are currently insolvent.

The clock is ticking here. Ignore trader games, something BAD is coming to the markets.

If you’ve yet to take steps to prepare for what’s coming, we have published an exclusive special report How to Invest During This Bear Market.

It details the #1 investment to own during the bear market as well as how to invest to potentially generate life changing wealth.

This report is usually $250, but we’re giving away 100 copies for FREE to those who sign up for our free daily market commentary.

As I write this, there are less than 19 left.

To pick up one of the remaining copies, use the link below…

https://phoenixcapitalmarketing.com/BM2.html