The following is an excerpt from my latest issue of Private Wealth Advisory. In it I outline the real dynamic between Greece and the EU leaders, how Greece has actually increased its number of Government workers during its “austerity measures” and when this whole mess will come Crashing down. To learn more about Private Wealth Advisory and how we help our clients profit from the “unquantifiable” opportunities in the markets… Click Here Now!!!

…the second Greek parliamentary elections in as many months came and went. While the media is making a big deal of the fact that the anti-bailout SYRIZA party didn’t win, the facts remain that the elections haven’t really accomplished anything of significance for Greece’s fiscal condition or the likelihood of it staying within the EU.

What I mean by this is that while the game of political musical chairs in Europe creates the appearance of change, the fact remains that Greece is broke and that the only thing stopping it from facing systemic collapse is continued support from the EU, particularly Germany.

Put another way, the primary dynamic of Greece attempting to procure more money by either paying lip service to the EU or playing the financial terrorism card (“kick us out and the whole EU system will fall”) remains firmly in place regardless of who’s in office.

Indeed, the New Democracy party, which now has the majority in Greece’s parliament, (due to a loose alliance with the socialist PASOK party which has shown itself to be just as willing to join the completely anti-bailout SYRIZA party) is already calling for a revision to the Second Greek bailout’s terms.

Greece outlines plan to ease bailout burden

Greece wants tax cuts, extra help for the poor and unemployed, a freeze on public sector lay-offs and more time to cut its deficit under a plan likely to run into strong opposition at a European Union summit next week.

The new coalition government’s programme, seen by Reuters on Saturday, reflected public pressure to ease the terms of a 130 billion euro ($163 billion) bailout saving Greece from bankruptcy but only at the cost of harsh economic suffering.

If implemented in full, the new programme would undo many austerity measures the country agreed in February to clinch the bailout package, its second since 2010.

http://in.reuters.com/article/2012/06/23/greece-idINL5E8HN1MI20120623

Three key takeaway items from this development:

1) Greek leaders, no matter what party they belong to, are unwilling to get Greece’s fiscal house in order (how many debt repayments and deadlines have they missed now?)

2) The current Greek Government is formed via a very loose coalition, which could very easily fall apart, resulting in yet another election.

3) Greece already wants a third bailout (note the additional €16 billion needed to cover the country’s financing needs).

In simple terms, at this point things have become truly farcical: Greece threatens, begs, and even lies in order to receive bailout funds only to then turn around and complete renege on the terms of the agreement. Indeed, we now have evidence that Greece was hiring more Government workers at a time when it was supposed to be implementing austerity measures:

Greece breached bailout rules with staff hirings: report

Greece breached the rules of its EU-IMF loan agreement by taking on some 70,000 public sector staff in two years, undermining efforts to reduce the state payroll, a report said on Sunday.

To Vima weekly said the hirings in 2010 and 2011 were highest in local administration, health, the police and culture, where the number of employees actually increased.

http://www.france24.com/en/20120624-greece-breached-bailout-rules-with-staff-hirings-report

This is extremely problematic for several reasons.

For one thing, this sends a clear message to the EU as well as the ECB and IMF that Greece is lying to their faces every time it promises to implement reforms. This doesn’t make for much political goodwill (note the survey quoted in the article below).

Greek PM cannot attend EU summit due to surgery

German Finance Minister Wolfgang Schaeuble repeated this view Sunday, in an interview to newspaper Bild am Sonntag.

“It must now be the most important task of Prime Minister Samaras’ new government to swiftly and immediately implement the agreed program without hesitation or asking, yet again, what the others could do in addition for Greece,” German Finance Minister Wolfgang Schaeuble was quoted as saying. “The ball is in Greece’s field; it is in their hands to achieve that Europe’s citizens can regain trust. But this will only be achieved through concrete measures and actions.”

The Sunday tabloid published a survey on Greece that it had commissioned with Italy’s Corriere della Sera, Spain’s ABC and France’s Le Journal Du Dimanche.

In it, 78 percent of the Germans polled, 65 percent of the French and about a half of the Italians said Greece should leave the Eurozone if it fails to pay its debt.

http://www.foxnews.com/world/2012/06/24/greek-pm-cannot-attend-eu-summit/#ixzz1yjbQVEOR

EU political leaders and their respective citizenry aren’t the only ones realizing that Greek political leaders are a bunch of crooks; the Greek people are also beginning to realize that their political leaders are not looking out for their best interests or for Greece’s: only 20% of the Greek bailout money went into the economy, the rest went towards paying off Greece’s creditors (read EU banks) and the ECB.

As a result of this, Greeks are increasingly voting for the SYRIZA party which is completely anti-bailout, anti-Euro, and anti-austerity:

| October 2009 | May 2012 | June 2012 | |

| SYRIZA’s % of Vote | 4% | 16.8% | 26.9% |

As you can see, SYRIZA is rapidly gaining popularity amongst Greek voters. This is extremely problematic as it indicates that should the current, new Greek government fall to pieces (as it most assuredly will… the new Finance Minister just resigned after being in office for only one week), it’s quite possible SYRIZA will win whatever subsequent election takes places.

European leaders will be meeting this Thursday and Friday to discuss Greece and other issues. As the above articles headline reveals, neither Greece’s new PM nor its Finance Minister (they no longer have one) will be in attendance.

However, we already know from the headlines this morning that Angela Merkel will not agree to Euro bonds or any kind of shared deposit insurance if it means “joint liability” (read: Germany being on the hook for other EU members’ bank losses).

We also know that the ECB is not interested in buying more government bonds (it hasn’t for 14 weeks now). And the ECB has stated point blank that Greek negotiations will not begin with Greece “wish[ing] for more time.”

So, there is a relatively high probability that a Grexit will be coming sooner rather than later. It all boils down to one simple fact: the second the money spigot from the EU to Greece gets turned off, Greece leaves.

Consequently, the real question is: “when does Germany and the rest of the EU stop picking up the tab for Greece?” Judging from the above survey in which even the French and Italians now think Greece should leave the EU if it doesn’t start paying its bills, it won’t be long: Greece will need another €16 billion in financing if the EU accepts its request for another extension (yes, this would be the third bailout).

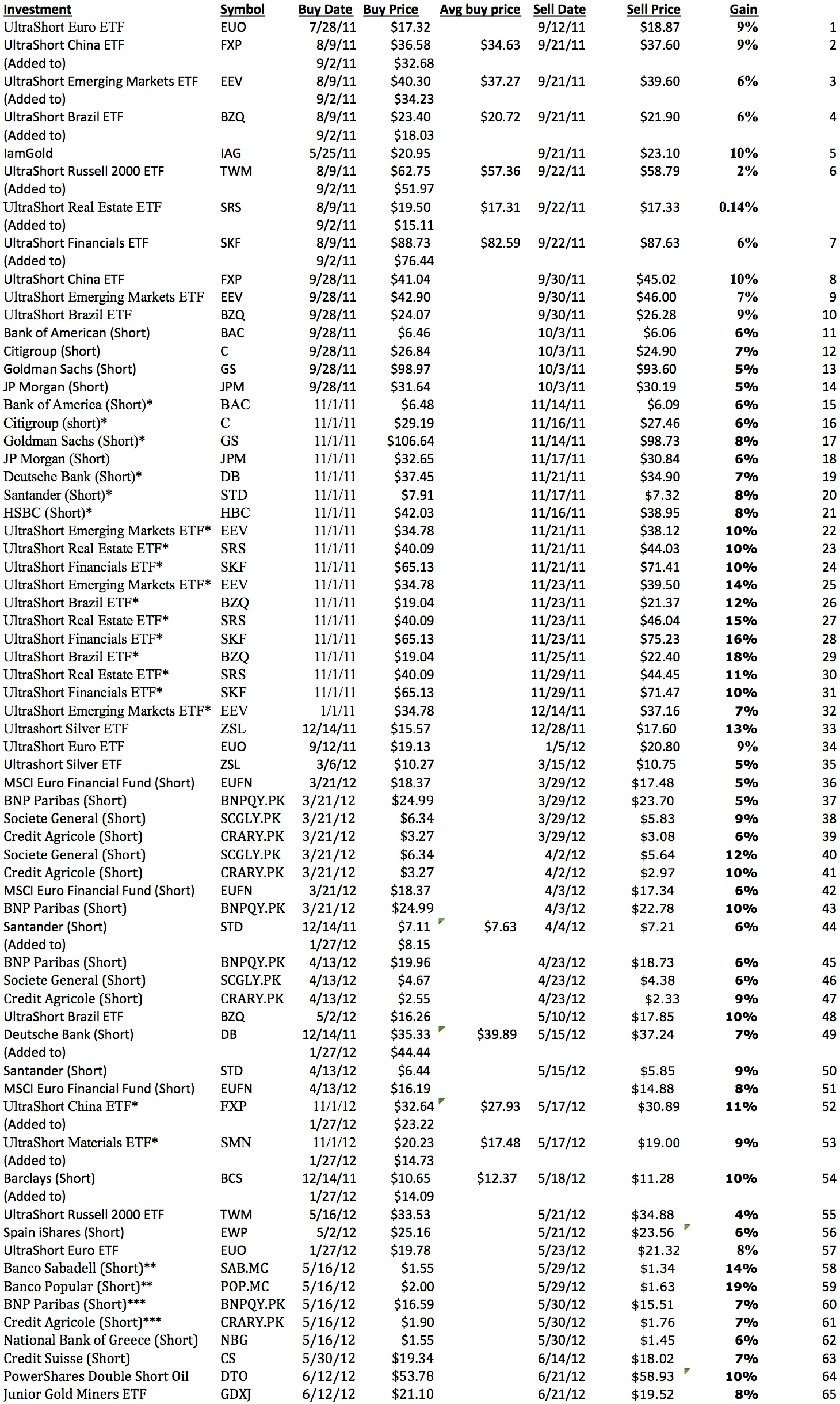

With that in mind, I’ve begun positioning subscribers of my Private Wealth Advisor for the possibility of a Grexit coming sooner rather than later. We’ve already locked in over 30 winning trades this year by finding “out of the way” investments few investors know about and timing our positions to benefit from the various developments in Europe. When you combine this with our 2011 track record, we’ve had 65 straight winners and not one closed loser since July 2011. If you think this is sounds “too good to be true,” you can Click Here to See Our Confirmed Trades.

Indeed, we just locked in two gains of 8% and 10% in less than two weeks’ time. In fact, this track record is getting so much attention that we’ve decided to only make 100 more slots available before we close the doors on this newsletter and simply start a waiting list. Already 65 slots have been reserved, leaving just 35 left.

To learn more about Private Wealth Advisory and lock in one of those last 40 slots…

Best Regards,

Graham Summers

Chief Market Strategist

Phoenix Capital Research

{kind=link}