It all boils down to Germany.

I’ve been forecasting for months that the country will increasingly focus on domestic interests and that it will ultimately opt to leave the Euro rather than prop up the EU.

The former (focusing on domestic issues) is already underway.

Germany Plans Joint Federal-State Debt in Merkel Fiscal Deal

Chancellor Angela Merkel agreed to share borrowing costs with Germany’s states to help ease their budget squeeze, completing a deal the opposition said will help secure German ratification of the European Union’s fiscal pact.

Germany’s federal and state governments plan their first joint debt sale in 2013 to help the states meet the pact’s deficit limits, the German government’s press office said in an e-mailed statement in Berlin today.

Pressed by the Social Democrat-led opposition that could block the stricter European fiscal rules in parliament, Merkel agreed to a policy she opposes in confronting the debt crisis in the rest of the 17-nation euro area. She signaled her rejection of joint euro-area debt as recently as June 23, saying “liabilities and controls” must “go together.”

“We reached a solution that makes it clear there will be approval” of the fiscal pact in the upper house of parliament, Kurt Beck, the premier of Rhineland-Palatinate state and member of the opposition SPD, said in an ARD television interview.

As for the latter development (Germany leaving the Euro), I believe that this will occur once the EU Crisis spreads to France. At that point any discussion of EU bailouts is pointless, as the very countries needing aid (France, Italy, Spain, and Greece) account for 53% of the ESM’s funding.

So far the markets have been willing to ignore the fact that Spain and Italy are meant to contribute 30% of the ESM’s funding. However, if France starts needing aid (and it will) it’s GAME OVER as any discussion of where the money will come from is moot.

By the look of things, this development is not too far away. France’s Socialist party took its lower house during the most recent elections. Already they are proposing reforms that will result in French businesses and capital leaving the country.

France’s new Socialist government is embarking on a series of risky experiments in business

Michel Sapin, the labour minister, has promised to make it so expensive for companies to lay off workers that it will no longer be worth their while. Firms that fire people while still paying dividends may be penalised. Another planned ruse is to force companies to sell factories, presumably along with the brands manufactured there, to competitors rather than close them down…

Paris is full of rumours of hasty departures. PPR, a luxury-goods group which owns Gucci and Yves Saint Laurent, is reported to have plans to move its entire executive committee to offices in London as soon as this summer. Technip, a global oil-services firm, is rumoured to be about to move its official headquarters across the Channel. (PPR declined to comment, and Technip said it has no plans to move for now.) To the fury of a French member of parliament, David Cameron, Britain’s prime minister, this week promised to “roll out the red carpet” for French companies on the run from the new tax.

But the most important consequence of stratospheric taxes will be less visible, at least at first. Marc Simoncini is one of France’s best-known entrepreneurs—and one of the few business leaders to denounce the new measures publicly. Why, he recently asked, would anyone want to start a business, invest and succeed in the most taxed country in the world?

Tax is not the only threat to executive pay. Last week Pierre Moscovici, the finance minister, announced that pay for bosses of companies in which the French state holds the majority of shares will be capped at a flat rate of €450,000, or roughly 20 times the wage of the lowest-paid worker. The French experiment will no doubt be watched with interest around the rich world. In some cases it will lead to a 70% pay cut. Over time, the quality of management at these state firms, which had become more professional over the past decade, will surely suffer. Executives such as Guillaume Pepy, the boss of SNCF, the national railways, for instance, could secure a top position anywhere in his industry. Measures to limit pay at fully private firms are expected before long.

http://www.economist.com/node/21557318?fsrc=rss|bus

As one would expect, the wealthy French are fleeing the country.

Wealthy French Take Their Assets to London

It began in 2010, when wealthy Greeks started coming to London and buying up expensive townhouses in upmarket neighborhoods. Amid fears that Greece might leave the euro zone, they believed their money would be safe in Britain in its splendid isolation from the euro and the Continent’s sovereign debt crisis.

Then rich Spaniards started arriving. They were following by well off Italians, who at the start of the year overtook Russians as the biggest group of foreign buyers snapping up property in London, according to a survey.

Whenever the euro crisis heats up somewhere in Europe, the demand for expensive homes increases in Western Europe’s largest city particularly among well-heeled foreigners beset by asset angst.

London real estate agents are like the canary in the coalmine for the debt crisis. They can sense early on the next country to get sucked into the vortex. So who’s up next? Apparently it’s the French.

Real estate agents have been aware of a new wave of interest for months, but it’s been especially noticeable since Feb. 28. The night before, the then Socialist candidate for French president, François Hollande, who famously said “I don’t like the rich,” announced that, if elected, he would raise the top rate of tax on incomes over €1 million to 75 percent. At home, he got much applause for the announcement. But in London, the news produced a reaction that was noticeable on the computers of the London-based property company Knight Frank.

“Since February, when Hollande announced his wealth tax, there has been a large rise in web searches from French customers,” Liam Bailey, head of residential research at Knight Frank, recently told the Daily Telegraph…

To meet the demand, the property company Douglas & Gordon has just opened an office in South Kensington, where four native French speakers will be available to help out their house-hunting compatriots. Hollande’s tax speech immediately led to a 40 percent increase in inquires from worried French citizens, says David Blanc from the London asset management firm Vestra Wealth.

French banks are already leveraged at 25-to-1. The impact of a capital exodus by the wealthy will rapidly push leverage levels even higher. And given that French banks’ exposure to the PIIGS is equal to 30% of French GDP, it’s no surprise that French banks are posting some truly horrible charts.

I expect the EU Crisis to spread to France before autumn. At that point, it’s game over for any notion of the current EU lasting. Germany will walk.

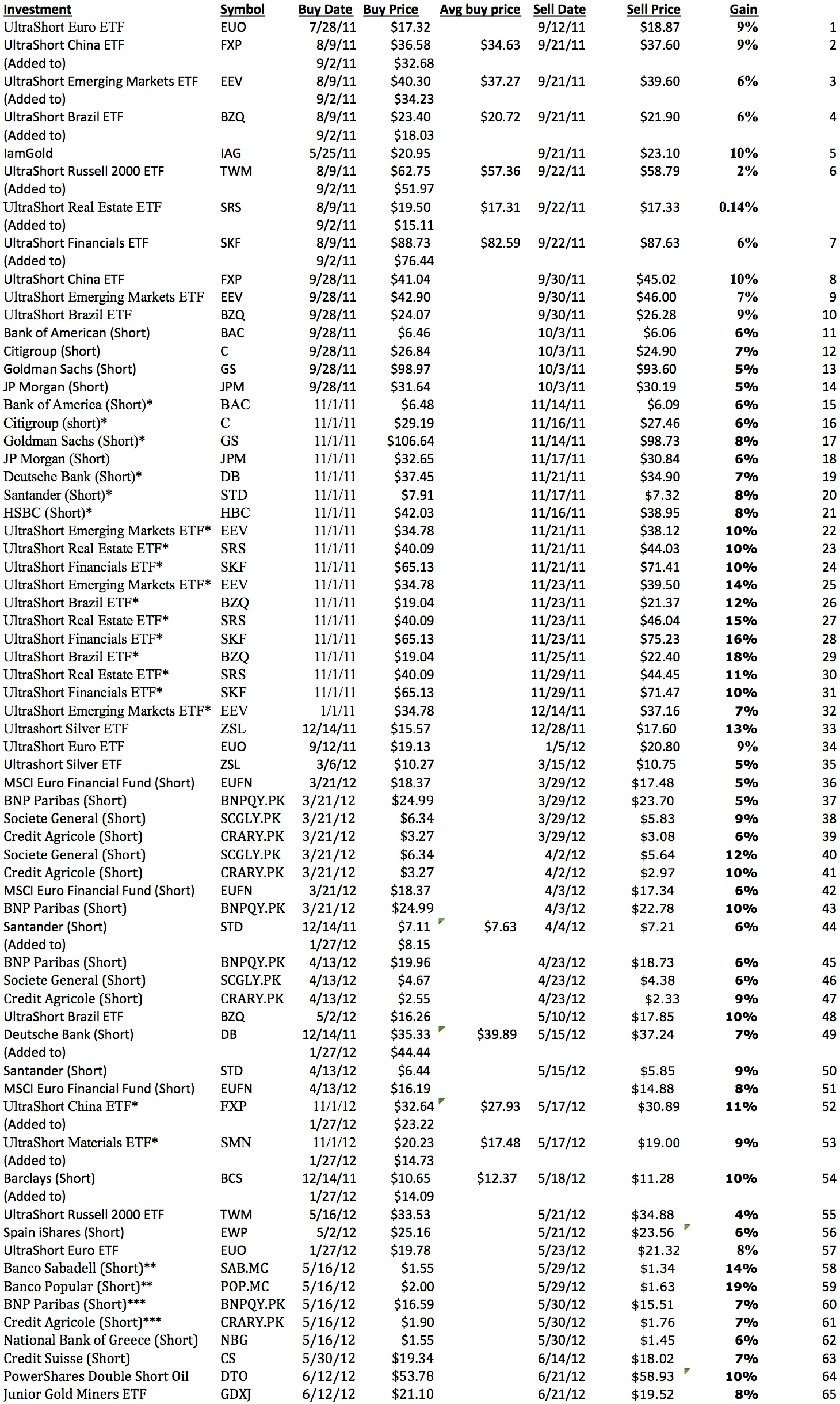

With that in mind, I’ve begun positioning subscribers of my Private Wealth Advisory for the next leg down. We’ve already locked in over 30 winning trades this year by finding “out of the way” investments few investors know about and timing our positions to benefit from the various developments in Europe. When you combine this with our 2011 track record, we’ve had 65 straight winners and not one closed loser since July 2011. If you think this is sounds “too good to be true,” you can Click Here to See Our Confirmed Trades.

Indeed, we just locked in two gains of 8% and 10% in less than two weeks’ time. In fact, this track record is getting so much attention that we’ve decided to only make 100 more slots available before we close the doors on this newsletter and simply start a waiting list. Already 70 slots have been reserved, leaving just 30 left.

To learn more about Private Wealth Advisory and lock in one of those last 30 slots…

Best Regards,

Graham Summers

Chief Market Strategist

Phoenix Capital Research

{kind=link}