The Fed Finally Created Inflation… And Now It’s Going To Blow Up the Financial System

By Graham Summers, MBA

The Fed finally succeeded in creating its much-desired inflation… and the great irony is that it will likely blow up the financial system.

For decades now the Fed argued that it should keep interest rates at zero… and continue printing hundreds of billions of dollars, because it wanted inflation to hit “2%.”

This is why the Fed did what it did after the Tech Crash, the Housing Crash, and the C-O-V-I-D-19 Crash. Anytime someone pointed out that the Fed’s monetary policies were creating another, even larger bubble, the Fed told us, “We need to keep doing what we’re doing until inflation hits 2%!”

The whole thing was a joke. After all, how can you create inflation of 2%, and make sure it stays at 2%? Inflation isn’t like a car where you can hit the desired speed and then press “cruise control.”

Regardless, the Fed has spent well over $7 trillion pursuing this goal. And now that inflation has arrived, it’s clear the Fed has no idea what it’s doing.

The official inflation numbers claim inflation is at 6.8%. However, everyone, including the Fed, knows this is fiction.

The real inflation number is well over 9%. The Bureau of Labor Statistics get away with stating that inflation is just 6% by claiming housing/ shelter prices are only up a mere 3% over the last 12 months. The reality, using actual data shows housing prices are up 19% and apartment rents are up over 8%.

Put simply, real inflation is much higher than 6%. But even the 6% inflation number is systemically problematic.

The Fed now claims it needs to tighten monetary conditions to stop the very inflation it has been trying to create. Stopping inflation means the Fed needs to raise rates. But the world is awash in debt and quite a bit of it was issued based on rates being at EXTRAORDINARY lows.

Some $2 trillion in corporate debt was issued in the U.S. last year alone. The U.S. Government issued another $5+ trillion. So right off the bat, you’ve got $7+ trillion in debt that was issued while rates were effectively at zero.

How is this going to adjust to rates at 1%? 2%? Higher?

For bonds with yields this low, every time the Fed raises rates, there is a dramatic impact. Remember, the yield on U.S. Treasuries represent the “risk free” rate of return against which the entire financial system is valued.

So, when the Fed raises rates, that $7+ trillion must adjust accordingly. This means those bond prices FALL and their yields RISE. And if they rise enough, the investors begin to default.

And we’re just getting started here.

As Lawrence McDonald recently noted, globally there is $30+ TRILLION MORE debt with sub-2% yields than there was the last time the Fed attempted to raise rates.

How is all that debt going to handle higher rates? What if the Fed has to raise rates way over 2% to stop inflation? What happens to the mountain of debt that was created BASED on yields being at 0%?

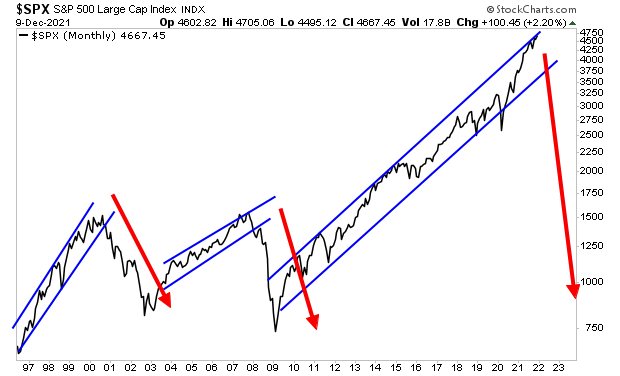

If you think the Fed can navigate this successfully, I would like to point out that the Fed wasn’t able to deflate the Tech Bubble nor the Housing Bubble without creating full-scale crises.

What are the odds the Fed can successfully deflate this current Everything Bubble… which is exponentially larger than the first two?

Look at the below chart and you tell me.

For those looking to prepare and profit from this mess, our Stock Market Crash Survival Guidecan show you how.

Within its 21 pages we outline which investments will perform best during a market meltdown as well as how to take out “Crash insurance” on your portfolio (these instruments returned TRIPLE digit gains during 2008).

To pick up your copy of this report, FREE, swing by:

https://phoenixcapitalmarketing.com/stockmarketcrash.html

Best Regards