The great debt crisis of out lifetimes is approaching.

The U.S. has now reached the point at which it is adding debt at an exponential rate.

It took the U.S. 232 years to rack up its first $10 trillion in debt. Thanks to the Fed’s egregious monetary policies following the Great Financial Crisis, the U.S. added another $10 trillion in debt in just nine years as the government went on a spending spree.

It’s added another $10 trillion in a little over FOUR years, thanks to the insane spending the U.S. implemented following the pandemic.

And the pace is only accelerating.

In June of this year, the U.S. had $31 trillion in debt. Today, it’s over $33 trillion. So we’ve just added another $2 trillion in a little over FOUR MONTHS.

And the Fed is confused as to why U.S. Treasuries are collapsing!?!

Basic economics tells us that the more of something there is… the less value it holds. Small wonder then that as the U.S. issues more and more debt, the debt is collapsing in value.

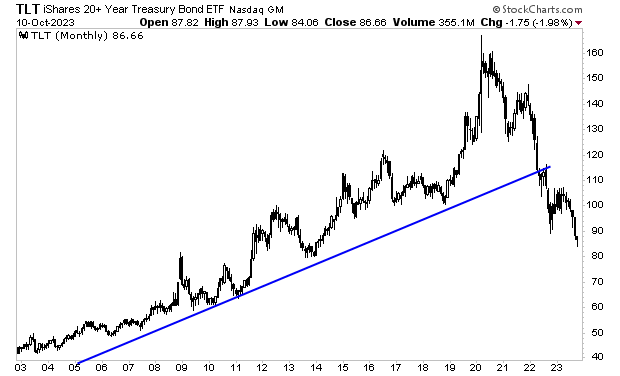

Below is a chart of the long-term U.S. Treasury ETF (TLT). It needs no explanation.

Again, the great debt crisis of our lifetimes is fast approaching.

In 2000, the Tech Bubble burst.

In 2007, the Housing Bubble burst.

The U.S. Treasury bubble burst in 2022. And the crisis is now approaching.

Smart investors are already taking steps to prepare for this.

I’ve identified a series of market events that unfold before every crash.

I detail them, along with what they’re currently saying about the market today in a Special Investment Report How to Predict a Crash.

Normally this report would be sold for $249. But we are making it FREE to anyone who joins our Daily Market Commentary Gains Pains & Capital.

Yesterday I

outlined why I believe most crypto-currencies will eventually prove worthless.

By way of quick

review, crypto is a tech asset.

And all technological revolutions follow two phases:

The

initial breakthrough phase, which occurs before social/legal frameworks are in

place.

The

“normalization” phase during which social/legal frameworks are implemented

giving the technology a societal and financial legitimacy.

If you need a real-world example of this, think of the

electronic music file or MP3 revolution. The first phase was Napster, which

featured the sharing of music in what was later deemed as illegal activity (the

legal framework was not yet ready for the technology).

Then along came iTunes: the normalized version of

the technology in which MP3s could be bought and sold in a legally acceptable

form.

I believe bitcoin and crypto currencies are currently in

the Napster phase of their development. And the Fed will soon introduce

“iTunes.”

We know that as far back as 2017, the Fed was already

studying this issue:

As the price of the

cryptocurrency continues to soar, the Federal Reserve apparently is giving thought

to having a product like bitcoin for its own.

William Dudley, president and CEO of the Federal Reserve Bank of New

York, said at a conference Wednesday that the Fed is exploring the idea of its own digital currency, according

to reports from Dow Jones.

Any product likely would be well off in the future, he said, adding that

it would be “very premature” to estimate when the Fed would come up

with its own offering, according to Bloomberg.

Source: CNBC

More recently, on February 5th 2020, Lael

Brainard who sits on the Federal Reserve’s Board of Governors, which is in

charge of establishing Fed policy, stated the following:

In a Bank for

International Settlements survey of 66 central banks, more than 80 percent of

central banks report being engaged in some type of central bank digital

currency (CBDC) work.12 … a few

central banks report that they are moving forward with issuing a CBDC. Building

on the tremendous reach of its mobile payments platforms, China is

reported to be moving ahead rapidly on plans to issue a digital currency.13

Given the dollar’s

important role, it is essential that we remain on the frontier of

research and policy development regarding CBDC… we are conducting

research and experimentation related to distributed ledger technologies and their

potential use case for digital currencies, including the potential for a CBDC.

We are collaborating with other central banks as we advance our understanding

of central bank digital currencies.

Here is a senior member of the Fed

stating point blank that the Fed needs to introduce a central bank

digital currency (CBDC) in order to maintain the geopolitical standing of the

U.S. dollar. The fact she mentions this RIGHT after discussing the fact China

is moving forward with a sovereign digital currency tells us that this is a

matter of national security for the U.S.

And then just this week, Fed Chair

Jerome Powell commented that crypto currencies are “not convenient for payment”

due to swings in value. He added that the Fed will issue a report on U.S.

digital currency this summer.

Look, it’s obvious what the Fed is

doing here. China has already launched a pilot version of the digital yuan.

Ukraine, Saudi Arabia, Sweden and Thailand are also doing the same.

Do you think the Fed, the single most

important central bank in the world, which controls the world’s reserve

currency (the $USD) is going to sit back and let the world move into the

digital currency space without moving itself?

No chance in hell.

Which means at some point in the

not-so-distant future, the Fed will introduce “Fed

Coin” or whatever its CBDC will be called

When that happens, 99.9% of crypto currencies will go to

zero.

After all once the Fed introduces its own crypto

currency, EVERY other crypto currency would then exist in direct

competition to the Fed’s CBDC, which opens the door to charges of

counterfeiting and other Federal felonies.

Currently crypto does NOT compete with the Fed because

the Fed doesn’t have a CBDC yet. Once it does, everything changes.

Let me put it this way… what happened to Napster when

iTunes showed up?

Bear in mind, Apple the company is nowhere near as

powerful or formidable a competitor as the U.S. government. Someone might win a

lawsuit against Apple. Very few people win lawsuits against the U.S.

government.

Enjoy crypto in its current form, but know that it’s like Napster, and soon iTunes will come along.

Yesterday I

outlined why I believe most crypto-currencies will eventually prove worthless.

By way of quick

review, crypto is a tech asset.

And all technological revolutions follow two phases:

The

initial breakthrough phase, which occurs before social/legal frameworks are in

place.

The

“normalization” phase during which social/legal frameworks are implemented

giving the technology a societal and financial legitimacy.

If you need a real-world example of this, think of the

electronic music file or MP3 revolution. The first phase was Napster, which

featured the sharing of music in what was later deemed as illegal activity (the

legal framework was not yet ready for the technology).

Then along came iTunes: the normalized version of

the technology in which MP3s could be bought and sold in a legally acceptable

form.

I believe bitcoin and crypto currencies are currently in

the Napster phase of their development. And the Fed will soon introduce

“iTunes.”

We know that as far back as 2017, the Fed was already

studying this issue:

As the price of the

cryptocurrency continues to soar, the Federal Reserve apparently is giving thought

to having a product like bitcoin for its own.

William Dudley, president and CEO of the Federal Reserve Bank of New

York, said at a conference Wednesday that the Fed is exploring the idea of its own digital currency, according

to reports from Dow Jones.

Any product likely would be well off in the future, he said, adding that

it would be “very premature” to estimate when the Fed would come up

with its own offering, according to Bloomberg.

Source: CNBC

More recently, on February 5th 2020, Lael

Brainard who sits on the Federal Reserve’s Board of Governors, which is in

charge of establishing Fed policy, stated the following:

In a Bank for

International Settlements survey of 66 central banks, more than 80 percent of

central banks report being engaged in some type of central bank digital

currency (CBDC) work.12 … a few

central banks report that they are moving forward with issuing a CBDC. Building

on the tremendous reach of its mobile payments platforms, China is

reported to be moving ahead rapidly on plans to issue a digital currency.13

Given the dollar’s

important role, it is essential that we remain on the frontier of

research and policy development regarding CBDC… we are conducting

research and experimentation related to distributed ledger technologies and their

potential use case for digital currencies, including the potential for a CBDC.

We are collaborating with other central banks as we advance our understanding

of central bank digital currencies.

Here is a senior member of the Fed

stating point blank that the Fed needs to introduce a central bank

digital currency (CBDC) in order to maintain the geopolitical standing of the

U.S. dollar. The fact she mentions this RIGHT after discussing the fact China

is moving forward with a sovereign digital currency tells us that this is a

matter of national security for the U.S.

And then just this week, Fed Chair

Jerome Powell commented that crypto currencies are “not convenient for payment”

due to swings in value. He added that the Fed will issue a report on U.S.

digital currency this summer.

Look, it’s obvious what the Fed is

doing here. China has already launched a pilot version of the digital yuan.

Ukraine, Saudi Arabia, Sweden and Thailand are also doing the same.

Do you think the Fed, the single most

important central bank in the world, which controls the world’s reserve

currency (the $USD) is going to sit back and let the world move into the

digital currency space without moving itself?

No chance in hell.

Which means at some point in the

not-so-distant future, the Fed will introduce “Fed

Coin” or whatever its CBDC will be called

When that happens, 99.9% of crypto currencies will go to

zero.

After all once the Fed introduces its own crypto

currency, EVERY other crypto currency would then exist in direct

competition to the Fed’s CBDC, which opens the door to charges of

counterfeiting and other Federal felonies.

Currently crypto does NOT compete with the Fed because

the Fed doesn’t have a CBDC yet. Once it does, everything changes.

Let me put it this way… what happened to Napster when

iTunes showed up?

Bear in mind, Apple the company is nowhere near as

powerful or formidable a competitor as the U.S. government. Someone might win a

lawsuit against Apple. Very few people win lawsuits against the U.S.

government.

Enjoy crypto in its current form, but know that it’s like Napster, and soon iTunes will come along.

I’ve received a number of emails from readers asking for my thoughts on crypto currencies.

First and foremost, I must warn you, I am a no-BS type analyst. So, if you want me to write something fluffy because you personally are a big fan of crypto, don’t read another word.

It’s not that I’m opposed to crypto currency per se, it’s that I know how policymakers think as well as how central banks work.

And I know BOTH groups have BIG plans for crypto currencies.

First let’s address the technology itself.

Crypto is in fact NOT a currency. Prior to 1913, by law, Congress was the only entity in the United States permitted to issue currency. It then handed this responsibility off to the Fed in 1913. And the Fed is the ONLY entity that can legally issue currency.

So crypto currencies are NOT currencies. They are just another asset class. To argue otherwise is to say you are counterfeiting money, which is ILLEGAL.

Now, crypto is a tech asset. And all technological revolutions follow two phases:

1) The initial breakthrough phase, which occurs before social/legal frameworks are in place.

2) The “normalization” phase during which social/legal frameworks are implemented giving the technology a societal and financial legitimacy.

If you need a real-world example of this, think of the electronic music file or MP3 revolution. The first phase was Napster, which featured the sharing of music in what was later deemed as illegal activity (the legal framework was not yet ready for the technology).

Then along came iTunes: the normalized version of the technology in which MP3s could be bought and sold in a legally acceptable form.

Bitcoin and crypto currencies are currently in the Napster phase of their development.

As such I am inherently wary of them. Moreover, we’re in something of a mania for this with over 5,000 currencies in the world. We are seeing crypto currencies that were literally created in TWO HOURS as a joke (Dogecoin as the tweet below shows), being valued at tens of billions of dollars.

I believe over 99% of cryptos are ultimately worthless.

Why?

Because at some point the US Government is going to do one of two things:

1) Start taxing cryptos like regular liquid assets (stocks).

2) Introduce its own “cash-less” means of exchange/ digital currency.

Regarding #1, since 2014 the IRS currently views crypto as “property” and suggests it should be taxed as such.

Now there is no federal property tax, so this would mean you would have to tax your crypto holdings based on what property taxes are in your local government. As of 2020, this ranged from the lowest state (Hawaii at 0.3%) up to the highest, (New Jersey at 2.2%.)

By law, come tax season you are supposed to value your crypto holdings at market values and pay taxes on them.

If you think that is bad news, you’re not going to want to read the rest of this article.

The current Secretary of the Treasury, Janet Yellen, has floated the idea of taxing cryptocurrencies as much as 80%, yes EIGHTY percent.

She is not alone, President Biden’s proposed tax increases would see capital gains taxes as high as 43%.

So, you literally have the Commander in Chief and the person in charge of the U.S. Treasury BOTH pushing for taxing cryptos at a minimum of 40%.

You can ignore this or claim its bunk, but if the government has proved one thing over the last 300 years, it’s that if there is money to be made from taxing an asset, they will start taxing it.

On top of this, at some point in the future, the Fed is going to introduce its own digital currency. We’ll address this topic in tomorrow’s article.