The US Federal Reserve is obsessed with market reactions to its policies. Because of this, anytime the Fed plans to announce a major change in policy, it preps the markets via numerous leaks and hints… oftentimes for months in advance.

An excellent example of this concerns the Fed’s decision to taper QE back in 2013.

At that time, the Fed had been engaging in two open ended-QE programs… programs that had been running for over six months.

Rather than simply beginning to taper the programs, then-Fed Chairman Ben Bernanke, hinted that the Fed was contemplating a taper in June.

The markets reacted sharply with bond yields rising.

The Fed then spent six months allowing the market to get used to the idea of a taper, before the actual taper finally began in December 2013.

Put another way, the Fed gave the markets a full six months to adjust to a change in policy, before actually implementing said change. This only highlights just how focused the Fed is on market reactions to its policies.

In the simplest of terms: the Fed will NEVER surprise the market. This is particularly true now that the Fed is in the political cross hairs due to ample evidence showing its policies have increased wealth inequality.

If the Fed is planning on something new, particularly something that might have political repercussions, we’ll see numerous hints and suggestions well before the actual policy is unveiled.

With that in mind, we need to consider the number of Fed officials who have recently been hinting at Negative Interest Rate Policy or NIRP.

- First we find that a Fed official hinted at NIRP during the Fed’s September 2015 meeting.

- Then, on October 9th, Fed President Bill Dudley stating that negative rates were “an option” though not a “relevant conversation” right now.

- This statement was followed up by Minneapolis Fed President Narayana Kocherlakota stating point blank that the Fed should “consider negative rates.”

The Fed has never once hinted at or discussed NIRP during its policy meetings. Then, in the span of three weeks, we’ve not only had an anonymous Fed official state that he or she believes NIRP is coming to the US, but two highly visible Presidents have called to NIRP consideration.

This is simply part of the Fed’s larger War on Cash.

For six years straight, the Fed has been trying to “trash” cash.

First it cut interest rates to zero… making it so that savings deposits produced almost nothing in the way of interest income. Consider that at current rates, a retiree with $1 million in savings earns a measly $2,500 per year in interest income.

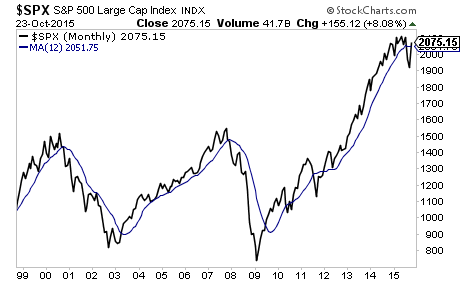

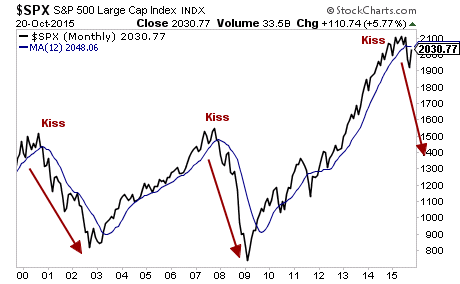

The Fed’s hope was that by making it painful for savers to sit in cash, said savers would move into risk assets such as bonds and stocks. This has worked in that stocks are now in one of, if not THE biggest bubbles in history… while bonds are trading at yields never before seen outside of wartime.

However, the Fed overlooked two outlets for investors who didn’t want to be forced into risk. They are: Gold bullion and physical cash.

The Fed has been dealing with bullion via clear manipulation of prices for years (that’s an article for another time). And now it is moving to make physical cash obsolete.

This is just the beginning. Indeed… we’ve uncovered a secret document outlining how the US Federal Reserve plans to incinerate savings in the coming months through NIRP, and possibly even by outlawing physical cash.

We detail this paper and outline three investment strategies you can implement

right now to protect your capital from the Fed’s sinister plan in our Special Report

Survive the Fed’s War on Cash.

We are making 1,000 copies available for FREE the general public.

To pick up yours, swing by….

http://www.phoenixcapitalmarketing.com/cash.html

Best Regards

Graham Summers

Chief Market Strategist

Phoenix Capital Research

Our FREE daily e-letter: http://gainspainscapital.com/