Today is also the

second to last day of the week, which means we are about to see a new weekly

candle on the charts.

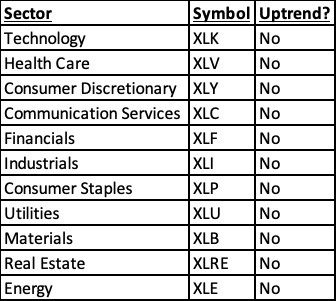

If the markets do not rally hard into the end

of the week, we will end this week without a single sector is in a definitive

uptrend. We have two potential uptrends (Consumer Discretionary and

Financials), but everything else would be in a confirmed DOWN-trend.

This means NONE of the market would be in a

confirmed uptrend and a full 76% of the market would in a DOWN-trend.

Sector

Symbol

Uptrend?

Weighting

Technology

XLK

No

27.60%

Health Care

XLV

No

13.50%

Consumer Discretionary

XLY

Maybe

12.70%

Communication Services

XLC

No

10.80%

Financials

XLF

Maybe

10.40%

Industrials

XLI

No

8.40%

Consumer Staples

XLP

No

6.50%

Utilities

XLU

No

2.80%

Materials

XLB

No

2.60%

Real Estate

XLRE

No

2.40%

Energy

XLE

No

2.30%

In Uptrend

0.00%

Counting Maybes

23.10%

This is the kind of environment in which real FIREWORKS can hit. Indeed, the below chart needs no explanation.

This has many investors asking themselves, “

is a crash about to hit?”

To figure this out, I rely on certain key

signals that flash before every market crash.

I detail them, along with what they’re currently saying about the market today in

a Special Investment Report How to Predict a Crash.

The markets are

bouncing today, but nothing has been resolved.

The technical

damage from the last few weeks has been horrific. The two most heavily weighted

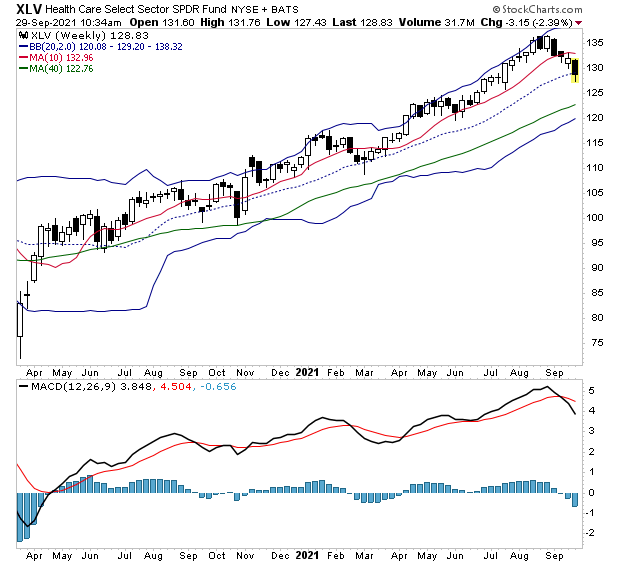

sectors in the S&P 500 (Tech and Healthcare) are in confirmed downtrends.

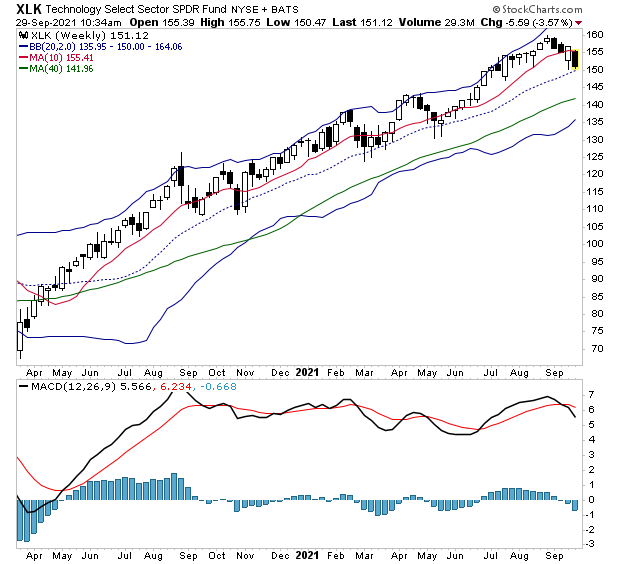

Tech (XLK) has broken

below its 50-DMA. It also as a sell on its weekly MACD.

It’s the same

story for Healthcare (XLV).

These two sectors

alone count for 40% of the S&P 500’s weighting. With both breaking down

like this, the market is under significant duress. Throw in the fact that all

but three sectors are in a similar situation, and we have some 85% of the

market’s weighting in DOWNTRENDS.

This is the kind of environment in which fireworks can hit.

But is a crash

about to hit?

To figure this out, I rely on certain key signals that

flash before every market crash.

I detail them, along with what they’re currently saying

about the market today in a Special Investment Report How to Predict a

Crash.

The

Fed continues to push the narrative that inflation is transitory.

On one level, Fed officials are correct. Everything is transitory. But the Fed isn’t being

philosophical here…it’s

attempting to argue that they don’t need to do anything, and the current wave

of inflation will naturally dissipate.

I know, this is ridiculous. But the Fed is so

desperate to maintain its $120 billion per month money printing scheme, that it

must come up with ridiculous excuses.

First it tried Climate Change, but since it’s

not clear how printing money fixes the weather, they’ve shifted gears to

claiming inflation isn’t an issue and will go away on its own.

Why do this?

Well, it’s difficult to claim that printing

$1.4 TRILLION per year is a benign enterprise when the cost of living is rising

by double digits. And so we end up with ridiculous situations in which Fed

officials are forced to make foolish claims such as their biggest concern is

that we won’t have enough inflation.

I’m not kidding.

Yesterday, Chicago Fed President Charles

Evans stated the following whopper: “I am more uneasy about us not generating enough inflation in

2023 and 2024 than the possibility that we will be living with too much.”

It’d be hilarious if it wasn’t causing so

much suffering for everyday Americans. Anyone who’s been to the grocery store

or filled up their cars at the gas station knows this is bunk.

The same goes for anyone who is paying

attention to what the markets are actually saying. If you turn off the news and

simply focus on the charts, it’s clear the market is SCREAMING “inflation!”

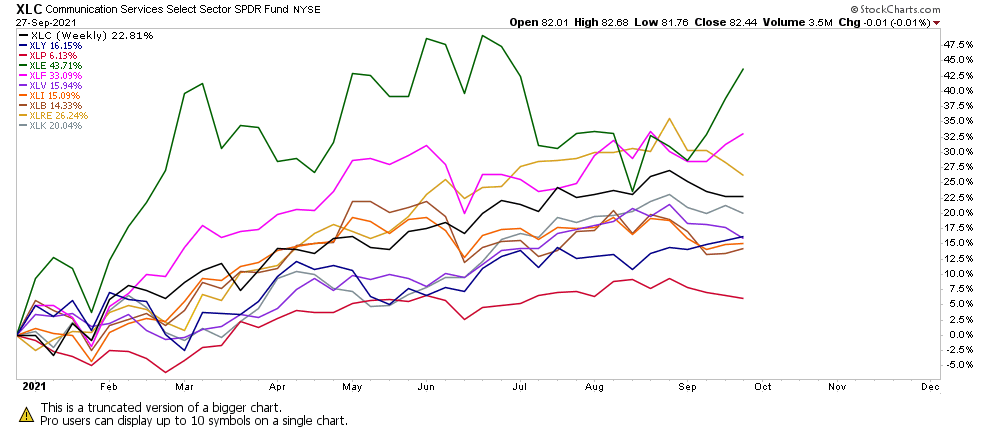

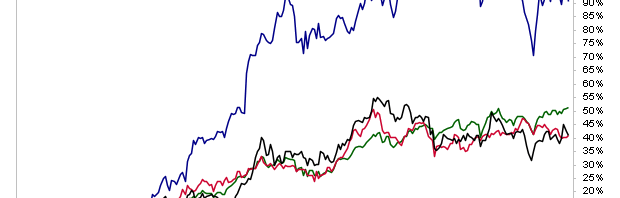

The top performing asset classes this year

are Energy (XLE), Financials (XLF) and Real Estate (XLRE). They are up 43%, 33% and 26%, respectively.

These are all inflation plays.

Energy and real estate are obvious. And

Financials rally when yields rise (and yields are rising due to inflation).

Heck, even Goldman Sachs has figured this out and is warning its private

clients about a commodities super-cycle courtesy of an inflationary storm.

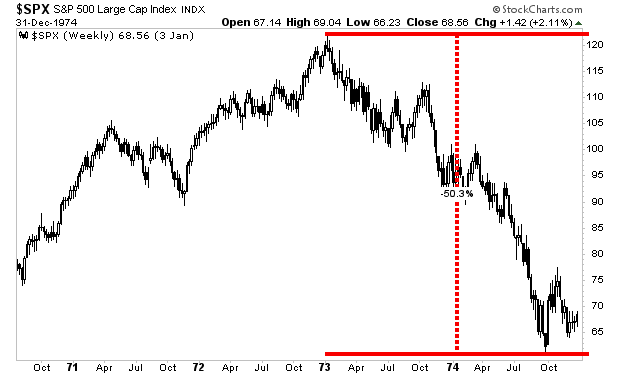

If you think this will be great news for the stock market, think again. During the last major bout of inflation in the 1970s, stocks collapsed some 50%. Even worse, they finished the decade DOWN.

Put another way, a crash is coming. The big question is, “WHEN?”

To figure this out, I rely on certain key signals that

flash before every market crash.

I detail them, along with what they’re currently saying

about the market today in a Special Investment Report How to Predict a

Crash.

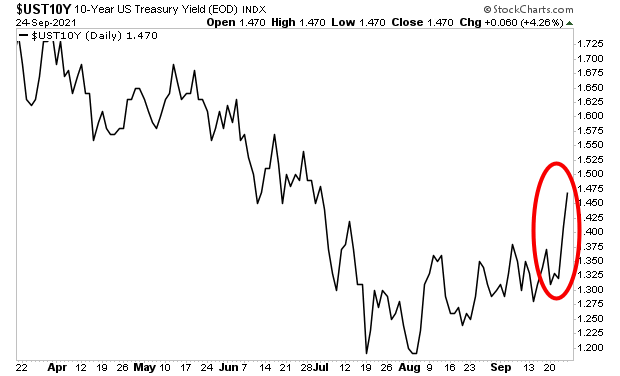

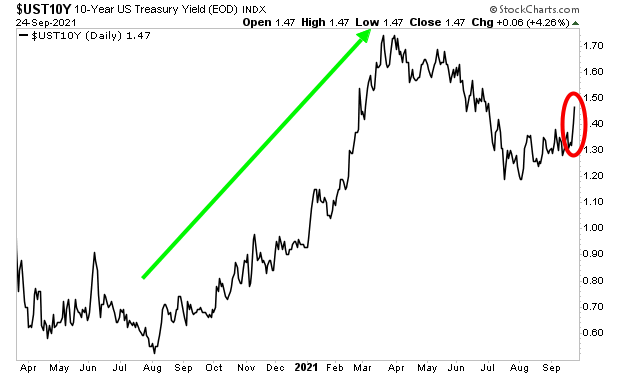

The biggest

development last week was the breakout in the 10-year U.S. Treasury.

The 10-year US

Treasury is arguably the single most important bond in the world.

The yield on this bond represents the risk-free rate of return against which

all risk assets (stocks, corporate bonds, mortgages, real estate, etc.) are

valued.

Now, this yield

moves based on a slew of issues: economic growth, portfolio balancing, Fed

monetary policy, what’s happening in international bond markets… and inflation.

I mention all of

this, because the yield on the 10-year US Treasury SPIKED sharply higher last

week.

Let’s put this

spike in a larger context.

From August of

last year (2020) until March of this year (2021), the yield on the 10-Year

Treasury spiked rose rapidly as inflation entered the US financial system. I’ve

illustrated this spike with a green arrow in the chart below.

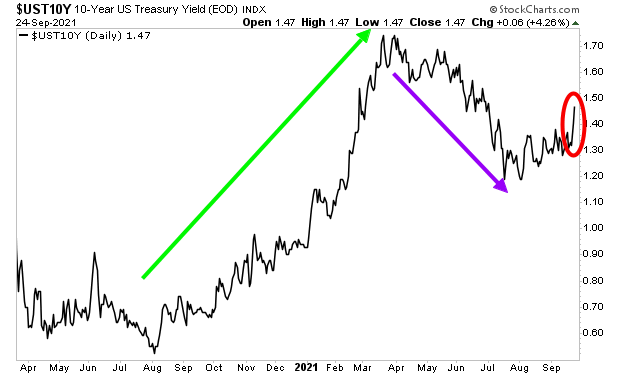

Then, in March of

2021, the Fed began to suggest that it was planning to tighten monetary policy.

This hurt inflation expectations as the financial system began to believe the

Fed would act quickly enough to stop inflation before it became a real problem.

As a result of this, the yield on the 10-year Treasury dropped from March of

2021 until July.

I’ve illustrated

this with a purple arrow in the chart below. This was, effectively, the bond

market giving the Fed the benefit of the doubt when it came to monetary policy.

In this context,

last week’s spike in the yield on the 10-year US Treasury represents the first

time since March that the bond market began to freak out about inflation again.

This is a MASSIVE

deal. It tells us that the market has called the Fed’s bluff: that the Fed won’t

act to stop inflation in time and that the economy and financial system are

heading towards a crisis in the near future.

If the Fed acts

now, by tightening monetary policy aggressively, it will crash stocks. After

all, the primary driver of this insane stock market bubble has been the Fed keeping

rates at zero and pumping $120 billion per month into the financial system.

And if the Fed DOESN’T

act now, inflation will rage, leading to a stag-flationary collapse in the economy…

and stocks will still crash as inflation destroys profits in the

corporate sector.

Just like in the mid-1970s, when stocks dropped 50% as inflation crippled the economy.

Put simply: a

crisis is coming no matter what the Fed does.

The big question is “WHEN”!?!?

To

figure this out, I rely on certain key signals that flash before every market

crash.

I

detail them, along with what they’re currently saying about the market today in

a Special Investment Report How to Predict a Crash.

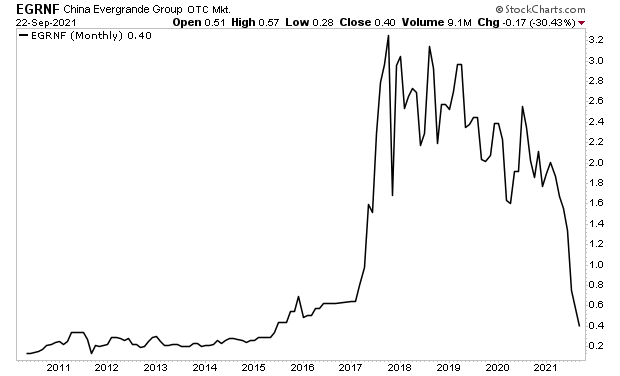

On

Monday, the markets were melting down due to fears of contagion from

Evergrande, China’s second largest real estate company, going bankrupt.

Since

that time, the market has bounced hard… despite the fact nothing has changed

about Evergrande, or its $300 billion in debt, or the contagion issues that it

presents to the financial system (commodities, EU banks, Australian miners,

etc.).

So,

the big question for stocks is: was this a dead cat bounce or the start of a

new major rally?

Let’s

find out.

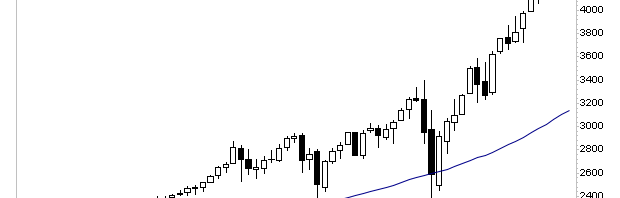

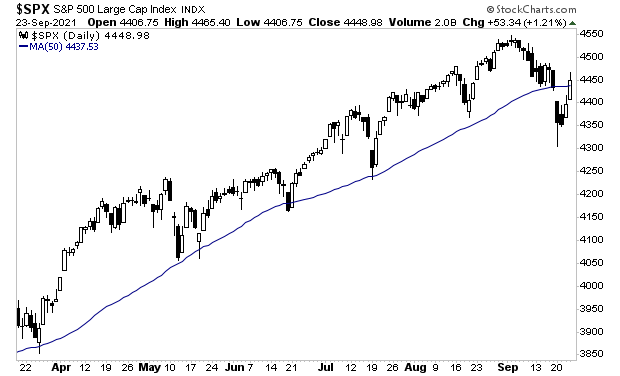

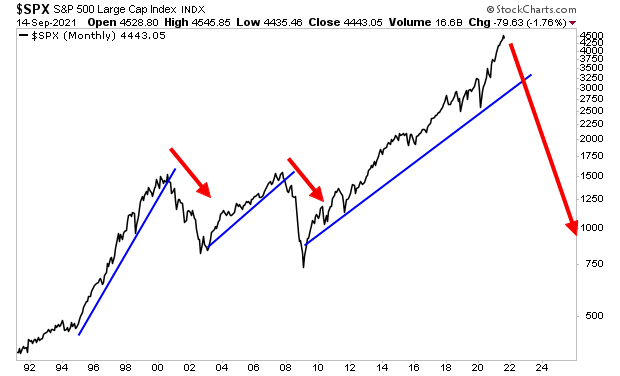

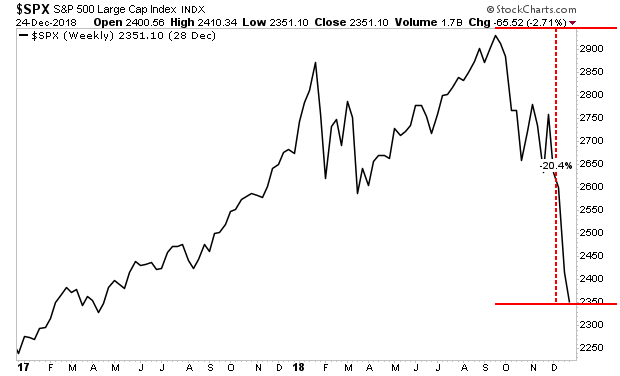

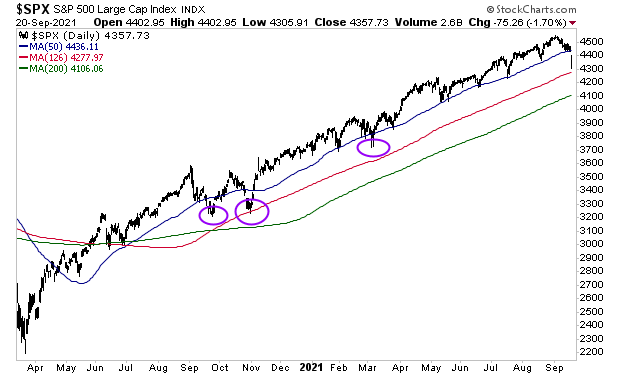

The S&P 500 is attempting to reclaim its 50-day moving average (DMA). As the below chart shows, this line has acted as major support throughout much of 2021. So, the fact we broke below it is significant. If the S&P 500 cannot reclaim this level and stay there… then stocks are in MAJOR trouble.

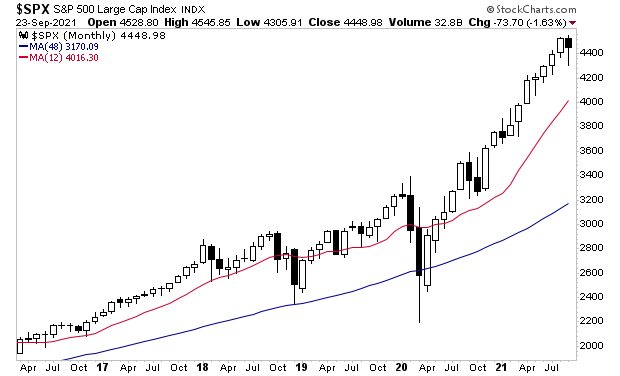

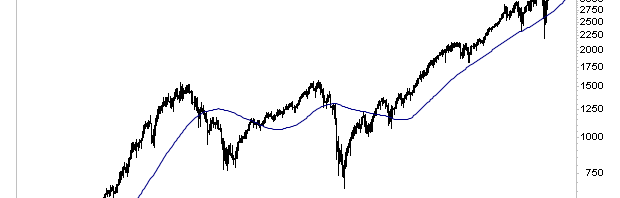

For anyone who understands risk management, the below chart has been a MAJOR concern for the last few months. On a monthly basis, the S&P 500 is EXTREMELY overstretched to the upside. At a minimum, you would expect a drop to the 12-month moving average (MMA) to occur sometime this year.

This would mean a 10% drop in stock prices.

Note in

the above chart that every drop to the 12-MMA started with a significant black

candle. We’ve got one week left in September, but it looks like we could be

getting our first black candle of the year.

However,

given that stocks are in their largest bubble of all time by some measures…

that leverage levels are obscene, and that we are seeing the kind of mania

associated with major tops… smart investors are asking…

“Is a Crisis about to hit?”

To

figure this out, I rely on certain key signals that flash before every market

crash.

I

detail them, along with what they’re currently saying about the market today in

a Special Investment Report How to Predict a Crash.

The

markets have rallied hard on news of a potential Evergrande debt payment.

In

case you’ve missed this story, Evergrande is a massive property developer in

China. The company is effectively insolvent, and with $300 billion worth of

debt many analysts were predicting this would lead to China’s “Lehman moment.”

We

had some fireworks on Monday, but the markets have since rallied hard on news

that Evergrande would make a payment on one of its Yuan-denominated

bonds.

That

payment is expected to be made today.

Regardless of what happens with this specific payment, the fact remains that Evergrande is effectively insolvent. The chart says it all.

Moreover, this company is not an isolated situation. China’s government has made it clear it wants the real estate sector to deleverage, which means many of the over-indebted property developers are at risk of similar issues. Real estate and construction account for 16% of China’s ~$15 trillion economy… so this is not a small problem.

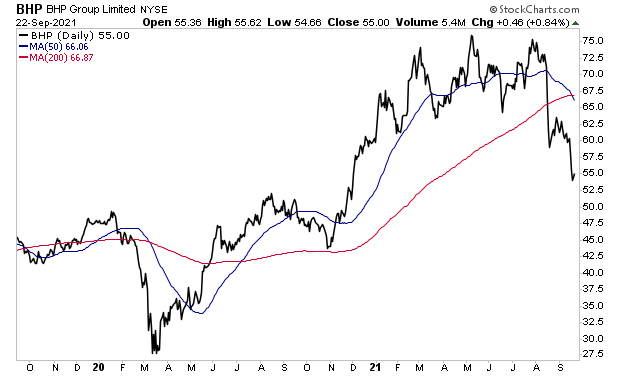

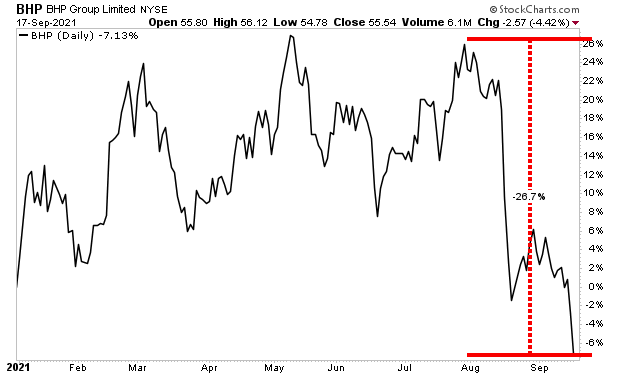

Keep an eye on BHP Group limited (BHP). As one of the largest

Australian mining companies responsible for supplying China’s construction/real

estate sectors, it’s a decent litmus test for whether or not this issue

is really resolved or not.

As I write this, BHP is staging a VERY small bounce. The chart is profoundly ugly.

At the end of the day, whether Evergrande pays its bond or not

today is just one paragraph in the book of bad debts that are floating around

the financial system. The fact the Fed has spent over $4 trillion propping

things up since 2020 doesn’t mean this whole mess won’t come crashing down.

In chart terms, it’s only a matter of time before this happens.

The multi-trillion dollar question is…

WHEN?!?!

To

figure this out, I rely on certain key signals that flash before every market

crash.

I

detail them, along with what they’re currently saying about the market today in

a Special Investment Report How to Predict a Crash.

The Fed is expected

to announce its tapering schedule for its current $120 billion per month Quantitative

Easing (QE) program. The Fed has been hinting at its plan for months, via both

Fed officials and media proxies.

The current proposal

appears to be a $10-$15 billion per month tapering program, starting in

November 2021. This is a very rapid scheme that would bring its QE program

to a complete end by mid-2022.

By way of comparison,

during the Fed’s last QE taper (that pertaining to QE 3 in 2017), the Fed reduced

the pace of its then-QE program by $10 billion every THREE months, with the pace

stopping at $30 billion per month.

Again, the current

proposed tightening is much faster and aggressive than the last.

The big question

is how the markets digest this. The last time the Fed attempted to taper a

major QE program, it ultimately blew up the corporate debt markets resulting in

stocks collapsing 20% in a matter of weeks.

Will the Fed blow

things up again?

It’s quite

possible, particularly when you consider that stocks are currently in their

largest bubble in history by some measures… financial leverage is

extraordinarily high… and we are seeing the types of mania associated with

major market tops.

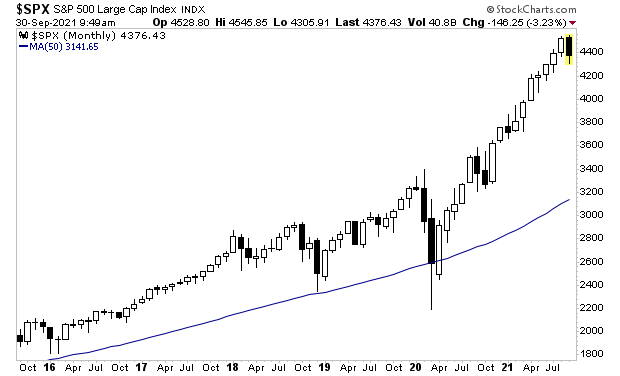

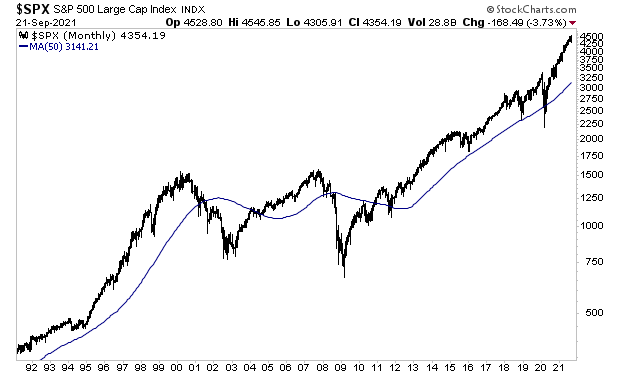

At the end of the

day, the stock market is EXTREMELY overstretched above its 50 -month moving average.

The only time it’s been more stretched was before the 1987 Crash and during the

Tech Bubble.

At some point we

are revisiting that blue line. The market always does.

By the way, the

50-MMA is currently at 3,141 while the S&P 500 is at 4354.

The big question

is WHEN will this happen?

To

figure this out, I rely on certain key signals that flash before every market

crash.

I

detail them, along with what they’re currently saying about the market today in

a Special Investment Report How to Predict a Crash.

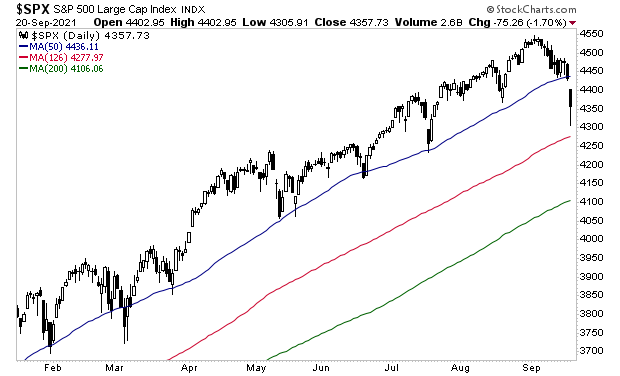

Stocks got creamed

yesterday, but thanks to late day manipulation, they ended up well off the

bottom.

From a purely

technical perspective, the S&P 500 has broken below its 50-day moving

average (DMA) for the first time since March 2021. Stocks then bounced hard off

the 126-DMA (six month moving average).

It will be crucial

to see how the markets act the next few days. We’ve had three significant

breaks below the 50-DMA since the March 2020 bottom: one in September ’20,

October ’20 and March ’21 (purple circles in the chart below). All of those

were resolved in a little over a week.

On the surface

things don’t look that bad. But “underneath the hood” things are terrible. None

of the S&P 500’s sectors are in uptrends.

Moreover, four out

of the five most heavily weighted stocks (AAPL, FB, AMZN, and GOOGL) have lost

their 50-DMAs and are losing their uptrends.

This is the kind

of environment in which actual crashes can happen.

To

figure this out, I rely on certain key signals that flash before every market

crash.

I

detail them, along with what they’re currently saying about the market today in

a Special Investment Report How to Predict a Crash.

The issue at hand

is China’s massive Evergrande property developer. The company is effectively

insolvent, with over $300 billion in bad loans. Many are calling this “China’s

Lehman Moment.”

The company’s

stock is down 80% Year to Date.

How serious is

this?

Serious.

Real estate

comprises nearly 8% of China’s economy. Construction is another ~8%. So, all in

all, you’re looking at 16% of the second largest economy in the world

experiencing the bankruptcy of one of its largest players. This has significant

implications for everything from commodities (use in construction) to finance

(the loans used to build the buildings and finance the mortgages for

consumers).

And in these types

of situations, there is never just one player at risk.

Contagion has

already begun. Hong Kong property developers and Chinese industrial producers

are getting hit. And if you think this will be confined to China you are

mistaken.

Australia supplies

much of the commodities China uses for its construction. It is not coincidence

that BHP Group (BHP) and other major Australian miners are nosediving, crashing

26% in the last few weeks.

And then there’s

European banks, which have massive exposure to China. By the look of the

bloodbath this morning, things are spreading to there as well.

This is the

problem with an Everything Bubble: you never know where the black swan is going

to come from.

With the financial

system in the single largest bubble of all time, and leveraged to the hilt by

easy debt courtesy of Central Bank policies, even a single spark can set the

whole thing to blow.

As I warned a few

weeks ago, this whole mess will come crashing down one day. In market terms,

this is going to happen, it’s just a matter of time.

The question of

course is “when”?

To

figure that out, I rely on certain key signals that flash before every market

crash.

I

detail them, along with what they’re currently saying about the market today in

a Special Investment Report How to Predict a Crash.

That the Fed knows the

official inflation measure, the Consumer Price Index (CPI) is

practically useless for forecasting future inflation.

In a little-known paper published in 2001, the

Fed found that food inflation, NOT CPI

or PCE, is the best predictor of future inflation. Fed researchers wrote

the following:

We see that past inflation in food prices has

been a better forecaster of future inflation than has the popular core measure [CPI and PCE]…Comparing the past

year’s inflation in food prices to the prices of other components that comprise

the PCEPI (as in Table 1), we find that the food component still

ranks the best among them all…

Source: St Louis Fed (emphasis added).

I want you to focus on these two admissions:

The Fed has admitted that

its official inflation measures do not accurately predict future inflation.

The Fed admitted that

FOOD prices are a much better predictor of future inflation. In fact, food

prices were a better predictor of inflation than the Fed’s PCE, non-durables

goods, transportation services, housing, clothing, energy and more.

I mention all of this because today food

inflation is erupting higher.

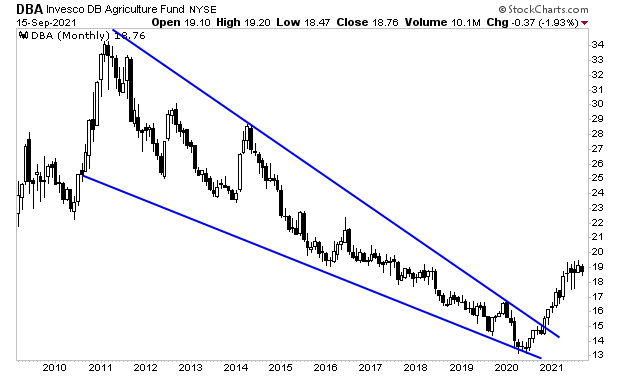

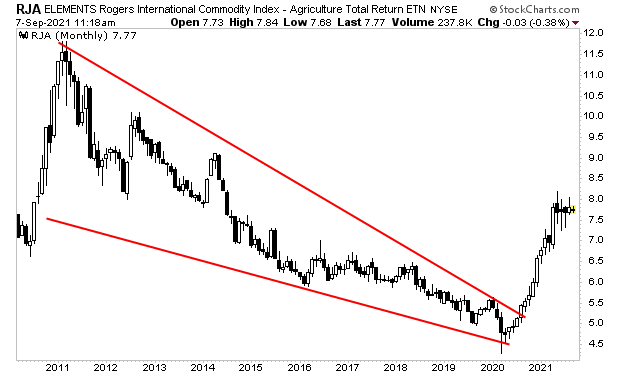

We already noted that agricultural commodities

are ripping higher.

But the situation is even worse than I

imagined. The below quote is truly horrifying…

Adjusted for inflation and

annualized, [food]costs

are already higher now than for almost anytime in the past six decades, according

FAO data. Indeed, it’s now harder to afford food than it was during the 2011

protests in the Middle East that led to the overthrow of leaders in Tunisia,

Libya and Egypt, said Alastair Smith, senior teaching fellow in global

sustainable development at Warwick University in the U.K.

Source: Yahoo! Finance

Put simply, food inflation today than at almost any time in the

last 60 years. That would include the 1970s, when inflation went into the

double digits and the stock market crashed over 50% in a matter of months.

If you think we’re immune to something like this now, take a look

at the below chart. This is a massive bubble, looking for a pin. And by the

look of things, inflation is it!

On that note, we published a Special Investment

Report concerning FIVE secret investments you can use to make inflation pay

you as it rips through the financial system in the months ahead.

The report is titled Survive the

Inflationary Storm. And it explains in very simply terms how to make

inflation PAY YOU.

We made 100 copies available to the public.

Today is the last day this report is available

to the general public.

Yesterday I explained how the official

inflation statistic used by policymakers, the Consumer Price Index or CPI, is practically

useless.

I realize this is quite controversial.

After all, everyone on the planet from hedge fund managers to social security

administrators uses this data point as THE inflation measure.

Unfortunately for them, CPI is pretty

much useless. It doesn’t accurately measure inflation in any way shape or form.

Today, I’m going to let you in on a

little secret.

The Fed knows this.

In fact, the Fed has known this for

years… since 2001 to be exact.

Back in 2001, the Fed had several

researchers dive into the subject of inflation. Their goal was the analyze

whether the Fed’s preferred measures of inflation (the CPI and the Personal

Consumption Expenditures or PCE) are decent predictors of future inflation.

The Fed also investigated a whole slew of

other inflation measures for comparison purposes.

The results?

The Fed found that food inflation,

NOT CPI or PCE, is the best predictor of future inflation. Fed researchers wrote the following:

We see that past inflation in food prices has been a better forecaster of future inflation than has the popular core measure [CPI and PCE]…Comparing the past year’s inflation in food prices to the prices of other components that comprise the PCEPI (as in Table 1), we find that the food component still ranks the best among them all…

Source: St Louis Fed (emphasis added).

I want you to

focus on these two admissions:

The

Fed has admitted that its official

inflation measures do not accurately predict future inflation.

The

Fed admitted that FOOD prices are a much better predictor of future inflation.

In fact, food prices were a better predictor of inflation than the Fed’s PCE, non-durables

goods, transportation services, housing, clothing, energy and more.

With that in mind,

take a look at what is happening with agricultural commodities, which are the

primary supplies for food.

You are looking at

the end of a 12-year bear market… and the beginning of a new bull market.

If you think this

is going to go well for stocks, you are mistaken. During

the last major bout of inflation in the 1970s, stocks initially ripped higher

for a few years before crashing ~50% erasing all their gains and then some.

Even worse, the stock market finished the decade having gained ZERO in 10

years.

On

that note, we just published a Special Investment Report concerning FIVE secret

investments you can use to make inflation pay you as

it rips through the financial system in the months ahead.

The

report is titled Survive the Inflationary Storm. And

it explains in very simply terms how to make inflation PAY YOU.

The government bean counters are working overtime to hide inflation.

Yesterday’s Consumer Price Index (CPI) number would be hilarious if it wasn’t so damaging to Americans. According to the Bureau of Labor Statistics (BLS), inflation rose only 0.3% month over month for the month of August and 5.3% year over year.

Anyone who lives in America knows this is total bunk

The BLS claims inflation in rents is up a mere 2.9% year over year. The very same day this came out, the Wall Street Journal reported that in the real-world rents are up 10.3%. Also, home prices are up 18% over the same period.

Put simply, unless you live in a cave, your cost of living for shelter (which the BLS uses to calculate total inflation) is up a whole lot more than 2.9%.

Let’s keep going, shall we?

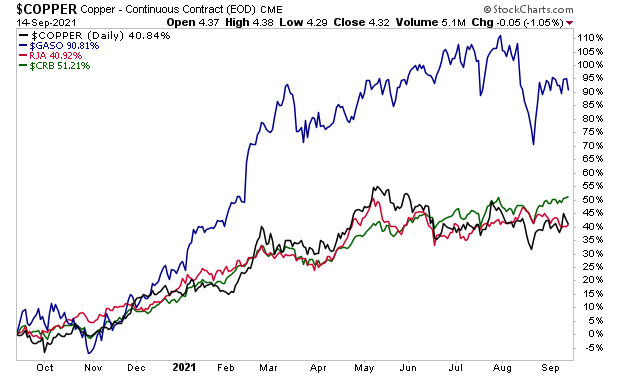

Over the last 12 months, the cost of every commodity is up 51%. Agricultural commodities are up 30%. So is copper. Gasoline prices have nearly doubled at 90%.

And yet, somehow the BLS claims inflation is just 5.3% year over year. I guess if you don’t drive a car, eat food, build anything, or use any commodities in any way, you’re probably fine.

The whole thing is ridiculous. And it begs the question… why is the BLS doing this?

I can’t claim to be psychic, so I have no idea what’s going on in these peoples’ minds. But I do know that a big reason to understate inflation is to mask the fact that real quality of life is in steep decline in the U.S.

This fact stares all of us in the face on a daily basis.

In the 1950s typically only one parent worked, and most Americans were able to afford their homes and live reasonably comfortable lives. In contrast, today typically both parents work, and most families have massive mortgages, student debt, credit card debt, auto loans, etc.

The whole system requires credit/ debt to function. Without it, most people cannot afford to live anything resembling a “middle class’ existence.

This whole mess will come crashing down one day. In market terms, this is going to happen, it’s just a matter of time.

The question of course is “when”?

To figure that out, I rely on certain key signals that flash before every market crash.

I detail them, along with what they’re currently saying about the market today in a Special Investment Report How to Predict a Crash.

The government bean counters are working overtime to hide

inflation.

Yesterday’s Consumer Price Index (CPI) number would be

hilarious if it wasn’t so damaging to Americans. According to the Bureau of

Labor Statistics (BLS), inflation rose only 0.3% month over month for the month

of August and 5.3% year over year.

Anyone who lives in America knows this is total bunk

The BLS claims inflation in rents is up a mere 2.9% year

over year. The very same day this came out, the Wall Street Journal

reported that in the real-world rents are up 10.3%. Also, home prices are

up 18% over the same period.

Put simply, unless you live in a cave, your cost of living

for shelter (which the BLS uses to calculate total inflation) is up a whole lot

more than 2.9%.

Let’s keep going, shall we?

Over the last 12 months, the cost of every commodity is up

51%. Agricultural commodities are up 30%. So is copper. Gasoline prices have

nearly doubled at 90%.

And yet, somehow the BLS claims inflation is just 5.3% year

over year. I guess if you don’t drive a car, eat food, build anything, or use

any commodities in any way, you’re probably fine.

The whole thing is ridiculous. And it begs the question… why

is the BLS doing this?

I can’t claim to be psychic, so I have no idea what’s going

on in these peoples’ minds. But I do know that a big reason to understate

inflation is to mask the fact that real quality of life is in steep

decline in the U.S.

This fact stares all of us in the face on a daily basis.

In the 1950s typically only one parent worked, and most

Americans were able to afford their homes and live reasonably comfortable

lives. In contrast, today typically both parents work, and most families have

massive mortgages, student debt, credit card debt, auto loans, etc.

The whole system requires credit/ debt to function. Without

it, most people cannot afford to live anything resembling a “middle class’

existence.

This whole mess will come crashing down one day. In market

terms, this is going to happen, it’s just a matter of time.

The question of

course is “when”?

To figure

that out, I rely on certain key signals that flash before every market crash.

I

detail them, along with what they’re currently saying about the market today in

a Special Investment Report How to Predict a Crash.

Yesterday, I explained why I believe we are due for a period of below average stock market returns.

By quick way of review:

Inflation is roaring higher. Official inflation measures put it at over 5%. Unofficial, more accurate measures have it clocking in at over 8%. And we are seeing corporations raise prices to deal with this.

Inflation is NOT good for stocks. During the last major bout of inflation in the 1970s, stocks initially ripped higher for a few years before crashing ~50% erasing all their gains and then some. Even worse, the stock market finished the decade having gained ZERO in 10 years.

The stock market is now extremely overstretched to the upside. On a monthly chart, the market is 40% above its 50-month moving average (MMA). The only time it has been more stretched above this line was right before the 1987 crash and during the Tech bubble.

So now the big question is… how do we profit from the inevitable collapse?

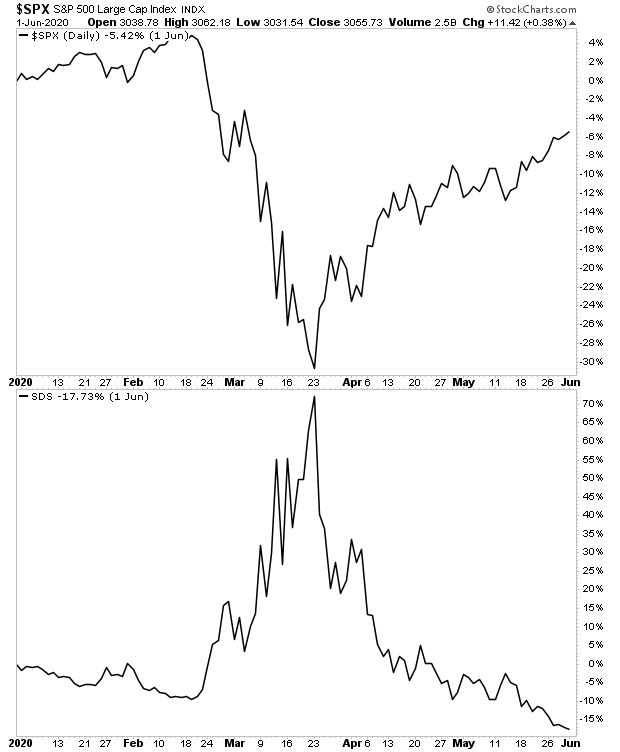

One method of doing this is the UltraShort S&P 500 ETF (SDS).

SDS was a leveraged play on the U.S. stock market collapsing.

You see, the SDS returns TWO TIMES the inverse of the S&P 500 ETF (SPY).

So, if the SPY falls 5%… the SDS returns 10%. Etc.

During market meltdowns, SDS is a great means of profiting from stocks collapsing. The below chart shows how it performed during the 2020 meltdown. Note SDS (bottom box) skyrocketed over 70% while the S&P 500 dropped some 30% in the month of March 2020.

However, I want to be clear here, DO NOT go out and buy this investment right now. SDS is a TRADE, not a long-term investment. Put another way, SDS ONLY works when the market is melting down. So, if you buy it at any other time, you’ll lose money.

So how do we know when the market is going to melt down?

To do that, I rely on certain key signals that flash before every market crash.

I detail them, along with what they’re currently saying about the market today in a Special Investment Report How to Predict a Crash.

One of the most

difficult things to learn about the stock market is the fact that it has little,

if anything, to do with the real economy.

This is a fact

borne out by both statistical studies and real-world analysis. And yet I would

argue that over 95% of investors don’t understand this.

For whatever

reason, most investors believe that the stock market is effectively a

derivative of economic growth.

The reality is

that the people thinking this haven’t really thought their arguments through to

their logical conclusions.

Indeed, if you

think I’m being naive with my views of the weak correlation between stocks and

the economy, consider that the mutual fund giant Vanguard performed a study

analyzing the correlation between stock market returns and various items

(dividend yield, stock market valuations, etc.), from 1926 to 2011.

They found that

the correlation between stock market returns and the direction or trend of GDP growth

was 0.05, or about 5%. Put another way, the trend of the economy only

explained roughly 1/20th of the stock market’s returns.

To put this into

perspective, it’s lower than the correlation between rain and stock

market returns. Yes, rain, as in whether or not it’s raining outside on

a given day.

If you still find

this hard to believe, let’s take a real-world example.

Between

1972 and 1982, the US economy nearly tripled in size from $1.2 trillion to $3.2

trillion. And yet, throughout that entire period the stock market traded

sideways for ZERO GAINS!

In

contrast, from 1982 to 2000, the US economy again nearly tripled in size from

$3.2 trillion to $10 trillion. But during this particular time, the stock

market exploded higher rising nearly 1,500%!

So, we

have two time periods in which the economy nearly tripled in size. During

one of them, the stock market went nowhere. During the other, the stock market

rose nearly 1,500%.

Again, stocks have little if any correlation to the economy. This is especially true during asset bubbles like the one we’re in today.

So how

do you determine when a bubble has burst and a crisis is about to begin?

To do

that, I rely on certain key signals that flash before every market crash.

I detail them, along with what they’re currently saying about the market today in a Special Investment Report How to Predict a Crash.

That the Fed is very likely now a political entity.

By quick way of review:

Fed Chair Jerome Powell’s term as Fed Chair ends this year.

The Biden administration has leaked in the media that it is considering giving Powell a second term.

Powell failed to present any meaningful information concerning the tightening of monetary policy at the Fed’s annual Jackson Hole meeting.

Based on inflation, GDP, and unemployment numbers, there are ZERO economic reasons for the Fed to NOT be already tightening monetary policy aggressively.

The above items suggest strongly that Powell has cut a deal with the Biden administration to gain reappointment.

That deal?

Keep the easy money flowing.

Again, there are no economic reasons for the Fed to continue its current monetary path. The fact that Jerome Powell won’t even commit to presenting a clear timeline for when the Fed will taper is truly negligent.

So where does this leave us?

As I’ve outlined recently, there are clear signs that inflation has entered the financial system.

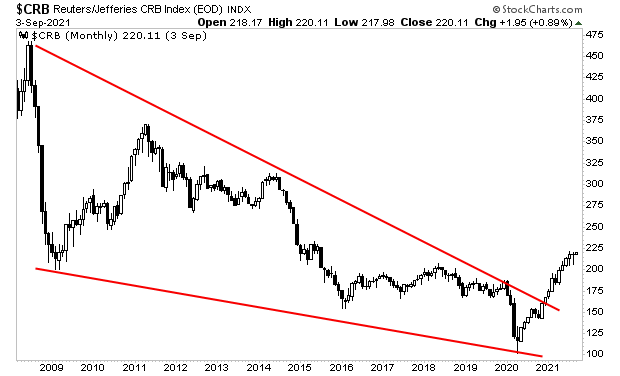

Commodities, which are inflationary hedges, have just broken out of a 13-year BEAR market.

Most important in this sector are agricultural commodities. The Fed’s own research has shown that the single best predictor of future inflation is food inflation. Well, take a look at what agricultural commodities are doing.

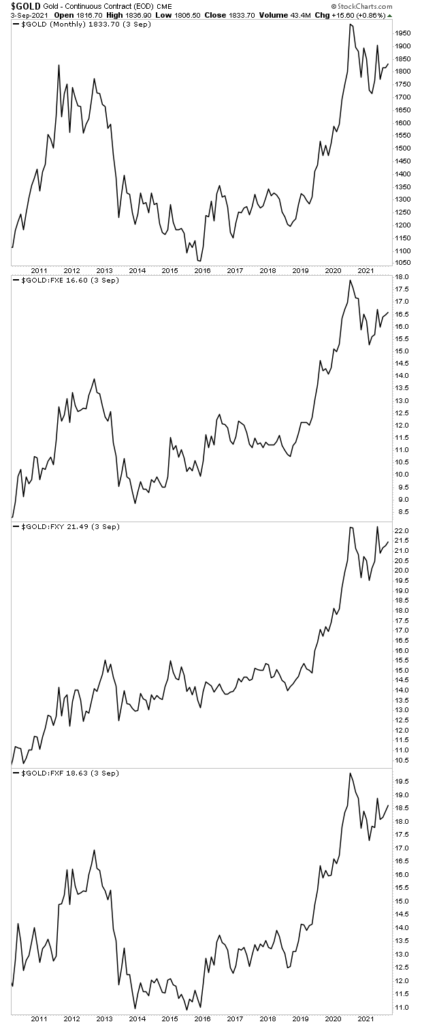

And then there’s gold, which recently rose to new all-time highs in every major currency.

These charts are SCREAMING inflation. And with the Fed refusing to tighten monetary policy for political reasons, this is likely just the beginning.

Smart investors are taking steps to profit from inflation today. I’ll outline some of my favorite ideas tomorrow.

On that note, we just published a Special Investment Report concerning FIVE secret investments you can use to make inflation pay you as it rips through the financial system in the months ahead.

The report is titled Survive the Inflationary Storm. And it explains in very simply terms how to make inflation PAY YOU.

Over the last two

days, I’ve outlined THE single most important development you need to see, in

order for the market to crash.

Think of them as

BIG warnings, or the FOUR Horsemen that precede a stock market apocalypse.

What are they?

When most heavily

weighted companies began to break down badly.

Technically, the

S&P 500 is made up of 500 companies. However, each of those 500 stocks

don’t receive the same weight from the index. Rather, certain stocks receive a

disproportionate weighting giving them a much larger impact on the market’s

price action.

Because of this,

in order to get a crash, you need the heaviest weighted stocks to break down

badly. Put another way, even if most of the 500 companies in the overall market

are in a downtrend, if the heaviest weighted stocks DON’T break down, it’s

pretty much impossible for the overall market to crash.

Yesterday we

reviewed the 1987 crash, noting that the vast majority of the 10 most heavily

weighted stocks had broken down in clear warnings that the market was in

serious trouble.

Let’s apply this

same methodology to today’s market. Today, the top 10 most heavily weighted

stocks in the S&P 500 are:

Company

Symbol

Weight

Apple Inc.

AAPL

6.26

Microsoft

Corporation

MSFT

5.96

Amazon.com Inc.

AMZN

3.82

Facebook Inc.

Class A

FB

2.38

Alphabet Inc.

Class A

GOOGL

2.27

Alphabet Inc.

Class C

GOOG

2.16

NVIDIA

Corporation

NVDA

1.47

Tesla Inc

TSLA

1.47

Berkshire

Hathaway Inc. Class B

BRK.B

1.41

JPMorgan Chase

& Co.

JPM

1.27

Total

28.48

Note that out of

an index of 500 companies, these 10 alone account for nearly 30% of the

market’s weight. So, in order for the market to crash, we need to see them

breakdown badly.

So, let’s take a

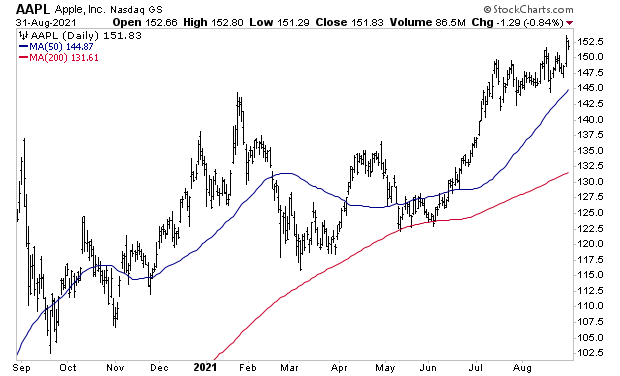

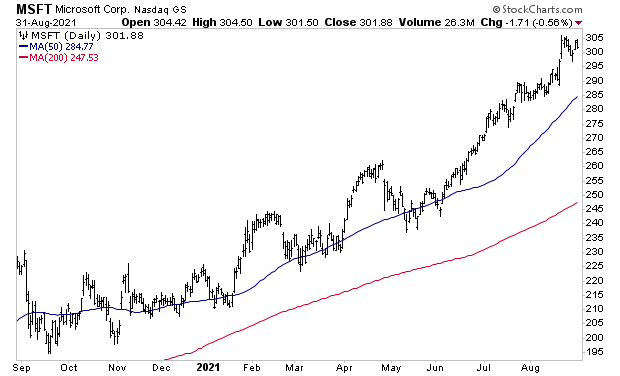

look at the top five today (September 2021).

Apple (AAPL): this

stock is clearly in an uptrend.

Microsoft (MSFT):

STRONG uptrend.

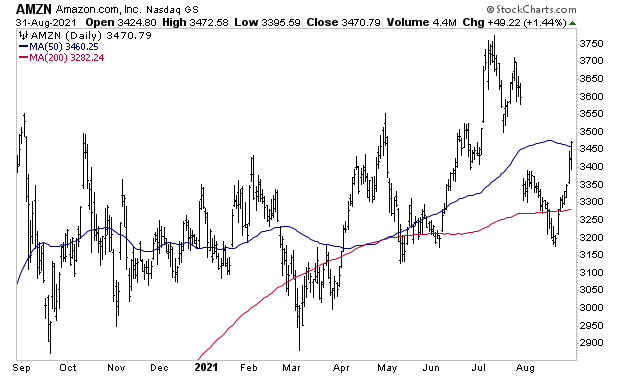

Amazon (AMZN): this is a weak chart. AMZN has been chopping back and forth for a year now. It’s not as bad as if the company had entered a definite downtrend, but it’s still pretty bad.

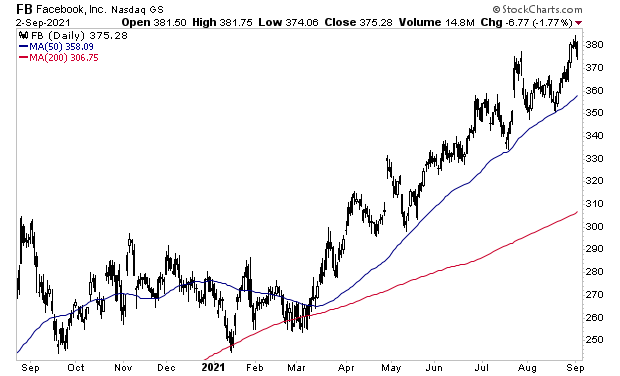

Facebook (FB): strong uptrend.

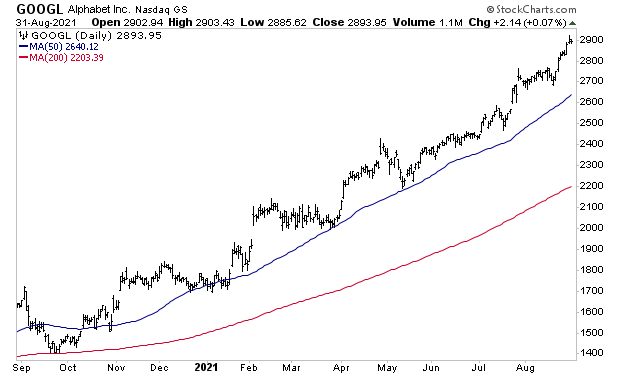

Alphabet (GOOGL):

incredible uptrend.

Put simply, out of

the top FIVE companies in the S&P 500, which account for nearly a quarter

of the market’s weight (22.8% to be exact), FOUR of them are in strong

uptrends.

While the market

is definitely in a bubble, until these companies break down, the odds of a

crash remain small. So, for now, it’s best to let this bubble run. Just keep an

eye on these companies. Once they start to break down, you’ll know it’s time to

start getting defensive.

In the meantime, if you’re looking for a guide on how to means to accurately predict crashes, what investments perform best during them, and how to take out “portfolio insurance” on your portfolio, we offer an Exclusive Investment Report, The Stock Market Crash Survival Guide outlining all those items and more.

Yesterday I outlined THE single most important development

you need to see, in order for the market to crash.

Think of them as BIG warnings, or the FOUR Horsemen that

precede a stock market apocalypse.

What are they?

When most heavily weighted companies began to break down

badly.

Technically, the S&P 500 is made up of 500 companies.

However, each of those 500 stocks don’t receive the same weight from the index.

Rather, certain stocks receive a disproportionate weighting giving them a much

larger impact on the market’s price action.

Because of this, in order to get a crash, you need the

heaviest weighted stocks to break down badly. Put another way, even if most of

the 500 companies in the overall market are in a downtrend, if the heaviest

weighted stocks DON’T break down, it’s pretty much impossible for the overall

market to crash.

So today, let’s review the 1987-Crash: arguably the worst

single-day collapse in stock market history.

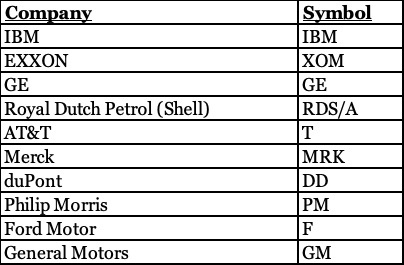

In 1987, the 10 largest companies by market weight were:

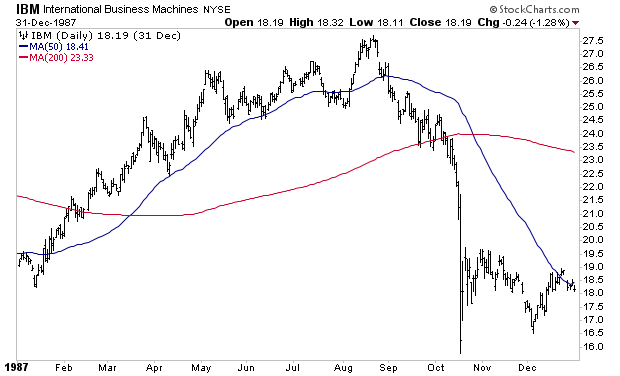

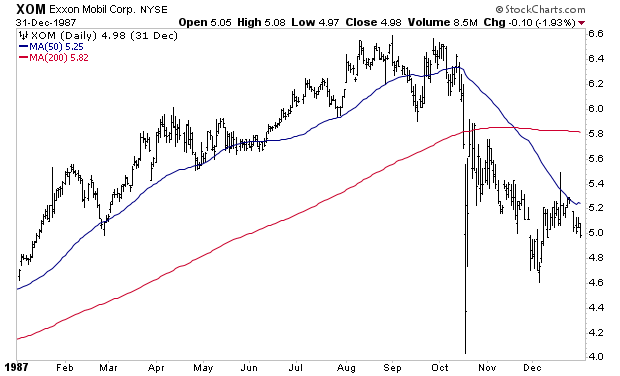

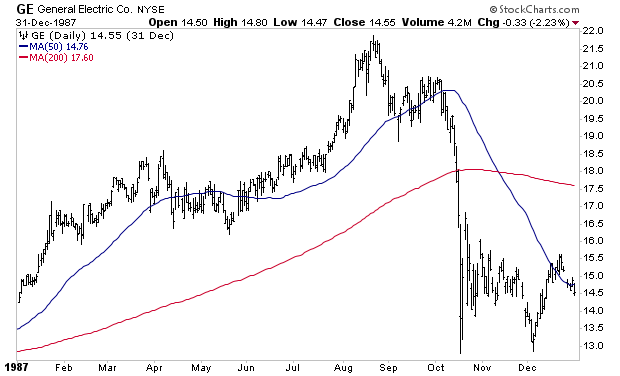

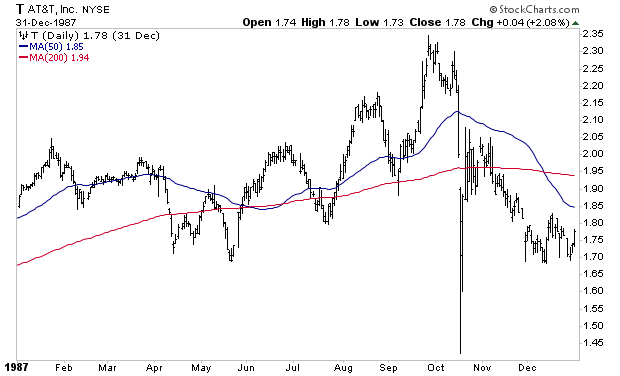

Of these, IBM, XOM, GE and T have charts that are easy to

find. So, let’s review them.

In 1987, IBM had already taken out both its 50-DMA and its 200-DMA before the crash hit. Put another way, the largest company on the index (the equivalent of the tech sector today) had already broken down VERY badly.

Exxon had yet to look as terrible, but it was clearly struggling, having traded sideways for months before finally breaking down.

General Electric looked awful, breaking its uptrend and

falling below its 50-DMA long before the Crash hit.

AT&T (T) was the only one that looked remotely good, as

it was still in something of an uptrend when the crash hit.

For space reasons, we’re only looking at four of the top 10

companies today. But if you were to look at all 10 charts, you’d quickly see

that the majority of them had entered downtrends, and were breaking down badly,

weeks before the Crash hit.

So does this impact the market today? Put another way, how

do we know when THIS will happen?

I’ll outline that in

tomorrow’s article. Until then…

In the meantime, if you’re looking for a guide on how to means to accurately predict crashes, what investments perform best during them, and how to take out “portfolio insurance” on your portfolio, we offer an Exclusive Investment Report, The Stock Market Crash Survival Guide outlining all those items and more.

Over the last few weeks, I’ve been outlining the clear evidence that stocks are in a bubble, arguably the largest stock market bubble of all time.

In truth, however, it’s not just a bubble in stocks, it’s a bubble in Treasuries, which the Fed has manipulated to absurd levels via over $2 trillion in Quantitative Easing (QE) during the last 18 months.

These bonds are the senior most asset in the current financial system. Their yields represent the “risk free” rate of return against which all risk assets (including stocks) are valued. So, when the Fed created this bubble in Treasuries, it was creating a bubble in Everything, which is why I call this the Everything Bubble.

Of course, this begs the question… when will it burst?

Put another way, when does THIS happen?

Predicting the actual week, let alone the day, of a market crash is all but impossible. However, there are certain key developments that MUST happen for the market to crash.

Think of them as BIG warnings, or the FOUR Horsemen that precede a stock market apocalypse.

What are they?

The most heavily weighted companies began to break down badly.

Technically, the S&P 500 is made up of 500 companies. However, each of those 500 companies don’t receive the same weight from the index. Rather, certain companies receive a disproportionate weight giving them a much larger impact on the market’s price action.

Because of this, in order to get a crash, you need the heaviest weighted stocks to break down badly. Even if most of the 500 companies in the overall market are in a downtrend, if the heaviest weighted stocks DON’T break down, it’s pretty much impossible for the overall market to crash.

I’ll outline precisely how this played out before the 1987 Crash (arguably the worst single-day collapse in stock market history) in tomorrow’s article.

In the meantime, if you’re looking for a guide on how to means to accurately predict crashes, what investments perform best during them, and how to take out “portfolio insurance” on your portfolio, we offer an Exclusive Investment Report, The Stock Market Crash Survival Guide outlining all those items and more.

Over the last few weeks, I’ve been outlining the clear evidence that stocks are in a bubble, arguably the largest stock market bubble of all time.

In truth, however, it’s not just a bubble in stocks, it’s a bubble in Treasuries, which the Fed has manipulated to absurd levels via over $2 trillion in Quantitative Easing (QE) during the last 18 months.

These bonds are the senior most asset in the current financial system. Their yields represent the “risk free” rate of return against which all risk assets (including stocks) are valued. So, when the Fed created this bubble in Treasuries, it was creating a bubble in Everything, which is why I call this the Everything Bubble.

Of course, this begs the question… when will it burst?

Put another way, when does THIS happen?

Predicting the actual week, let alone the day, of a market crash is all but impossible. However, there are certain key developments that MUST happen for the market to crash.

Think of them as BIG warnings, or the FOUR Horsemen that precede a stock market apocalypse.

What are they?

The most heavily weighted companies began to break down badly.

Technically, the S&P 500 is made up of 500 companies. However, each of those 500 companies don’t receive the same weight from the index. Rather, certain companies receive a disproportionate weight giving them a much larger impact on the market’s price action.

Because of this, in order to get a crash, you need the heaviest weighted stocks to break down badly. Even if most of the 500 companies in the overall market are in a downtrend, if the heaviest weighted stocks DON’T break down, it’s pretty much impossible for the overall market to crash.

I’ll outline precisely how this played out before the 1987 Crash (arguably the worst single-day collapse in stock market history) in tomorrow’s article.

In the meantime, if you’re looking for a guide on how to means to accurately predict crashes, what investments perform best during them, and how to take out “portfolio insurance” on your portfolio, we offer an Exclusive Investment Report, The Stock Market Crash Survival Guide outlining all those items and more.